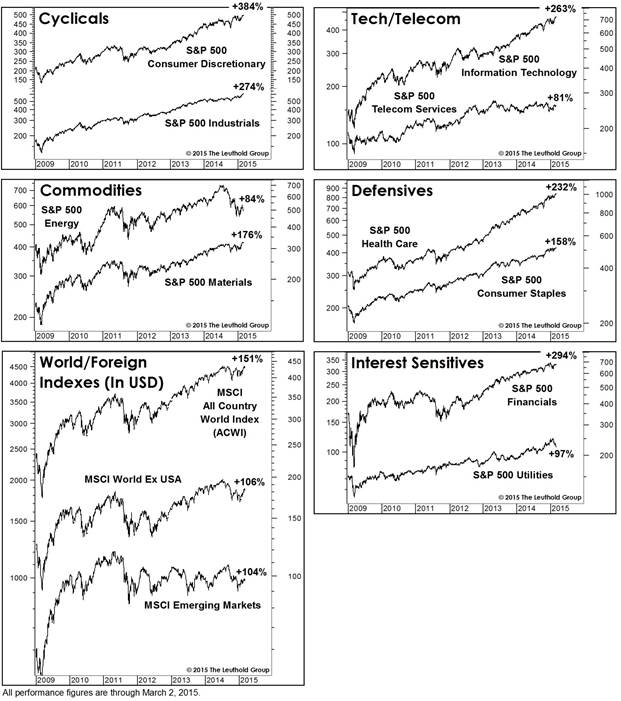

We cautioned investors during the current bull market’s initial blast-off not to expect a repeat of the prior bull market’s leadership—namely, Emerging Market equities and commodity-oriented equity sectors. Excesses built up during a sustained leadership cycle (i.e., equity valuations, production capacity) require a long period to be surged, generally resulting in the former leaders “skipping” a market cycle from a relative performance perspective. That view has been on the mark, with Emerging Markets merely doubling during the past six years (compared with a tripling of the S&P 500) and commodity-based equity sectors badly lagging other cyclical sectors.

Valuations on EM and Energy stocks have certainly become interesting, but we question whether either can mount a sustained leadership run during a cyclical bull that is already so extended. Cheap valuations in a late-cycle bull market are prone to be value traps. To single out an admittedly extreme example, the S&P 500 Financials traded near 12x earnings at the 2007 market high, but proceeded to fall 80% over the next 17 months.

Barring a major upheaval in our group models, we look for “Year Seven” of the bull market to be led by Technology and Health Care—two sectors whose valuations are much cheaper than their good-looking charts might suggest.

© 2015 The Leuthold Group