Why Fed Patience on Rate Hikes Is Likely to Continue

As the first quarter comes to a close, we believe:

- Lackluster economic data, low inflation, and a strong dollar could prompt the Federal Reserve to delay increasing short-term interest rates until late 2015, providing a tailwind for equities over the next few months. Bad economic news (provided it’s not too bad) will continue to be good news for stocks.

- That said, investors should be prepared for increased market volatility in the wake of this Friday’s jobs report and first quarter earnings reports, which kick off next week.

- As the ECB’s quantitative easing takes hold, long-term U.S. yields will follow euro zone rates downward.

- Growth equities and convertibles remain attractive. Growth equities have performed well when long-term rates have been low, and convertible securities can benefit in an environment of slow growth and slowly rising interest rates.

While we don’t believe we are in any danger of a recession, we’ve seen mounting indications that U.S. economic expansion is slowing, including weakness in durable goods orders, personal spending, housing starts, and exports. Although unemployment dropped to 5.5% in February and we’ve seen 12 consecutive months of job growth in excess of 200,000 (a record last achieved in the mid-1990s), these gains have not been accompanied by commensurate improvements in productivity or wage growth. As global energy supply continues to outpace demand, we would not be surprised if oil prices slide further (potentially to $40 a barrel). Although we believe prices can stabilize over the next few months as drilling contracts expire and capital spending cuts are implemented, certain industries and regions tied to the energy sector will still feel near-term economic pain. And more broadly across sectors, we expect corporate earnings growth will slow as a strong dollar makes overseas sales less profitable for U.S. multinationals.

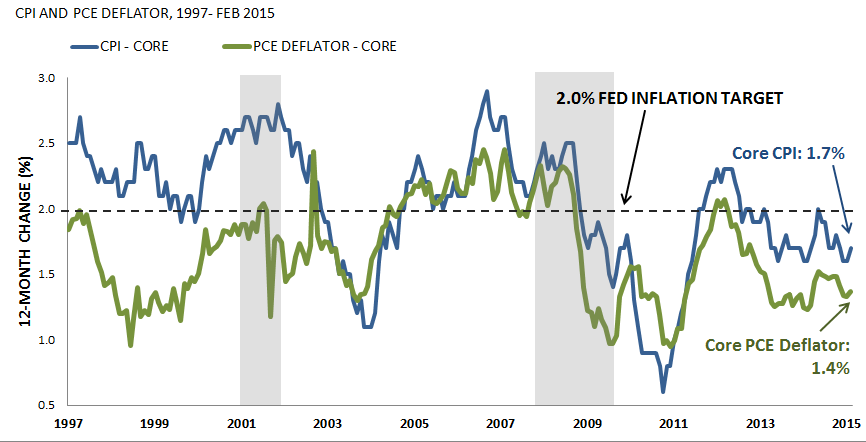

We believe this backdrop will compel the Fed to take a cautious approach. The Fed can also bide its time because inflation is not a problem. At 1.7%, the core Consumer Price Index is below the Fed’s target of 2.0%, while Chair Yellen’s preferred inflation measure, the core Personal Consumption Expenditures Deflator, is even lower at 1.4%.

Low Inflation and Sluggish Economic Growth Suggest Fed Will Remain Patient About Raising Short-Term Rates

Sources: Bureau of Labor Statistics and Federal Reserve Bank of St. Louis. Recessions indicated by shaded areas.

Despite our increased caution about the economy, we see continued opportunities for investors. Although a strong dollar may clip corporate profit growth, we see continued opportunities in equities, where earnings yields remain highly attractive relative to both U.S. Treasury bonds and inflation. Companies are continuing to take advantage of low corporate borrowing costs and high earnings yields, and merger-and-acquisition and share buyback activity remains robust. As we have noted in past posts, this activity can provide a floor to the equity markets during periods of volatility. Growth stocks remain attractively priced relative to value stocks, and we believe that growth stocks should continue to benefit as earnings growth slows but remains solidly positive, corporate earnings continue to expand, and long-term interest rates remain low.

We also maintain a constructive outlook on convertible securities. Because convertibles offer equity participation with potential downside protection, they can be particularly advantageous during volatile but rising stock markets. They can also provide a hedge against an eventual rise in interest rates, due to their equity characteristics.

Conclusion

For years, investors have been preoccupied about when the Fed will end its accommodative policy. While we cannot rule out the possibility of a policy misstep, we believe it is far more likely that when the Fed raises rates, it will be because the U.S. economy no longer needs the highly accommodative policy of the past several years. And that would be good news. In the meantime, we’ll be watching for Friday’s jobs report and the first batch of 1Q corporate earnings announcements, as well as preliminary first quarter GDP data in late April.

(c) Calamos Investments