Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

The Credit Managers Index deteriorated significantly over the last two months and current readings stand at the recessionary levels not seen since 2008. There is a very serious financial stress in the amount of credit extended to the businesses and the amount of credit applications rejected. The speed of deterioration is shocking.

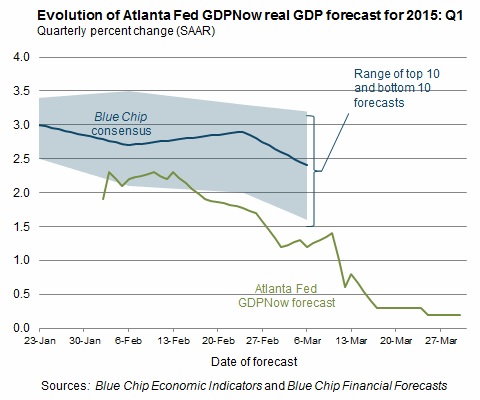

Our recent summaries of the leading indicators posed uneasy questions on the economic condition in the USA[1][2][3]. Since then the rosy projections of 3% GDP for the first quarter of this year turned into 0.8% estimate from Goldman Sachs and 0.2% estimate of GDPNow[4] now-casting model from Federal Reserve Bank Of Atlanta:

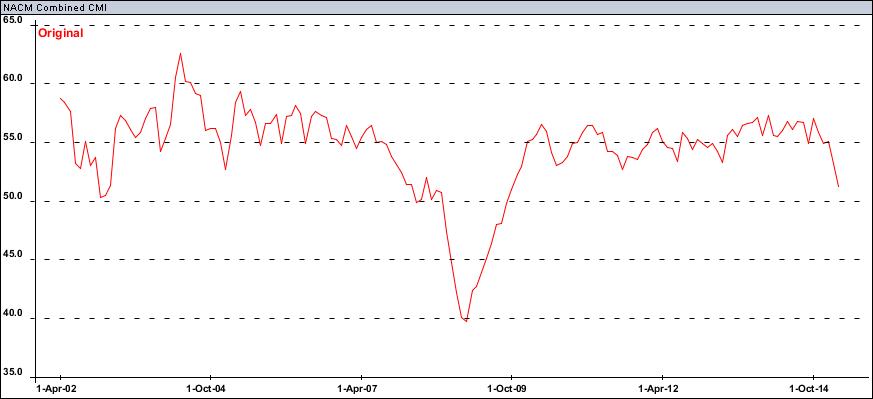

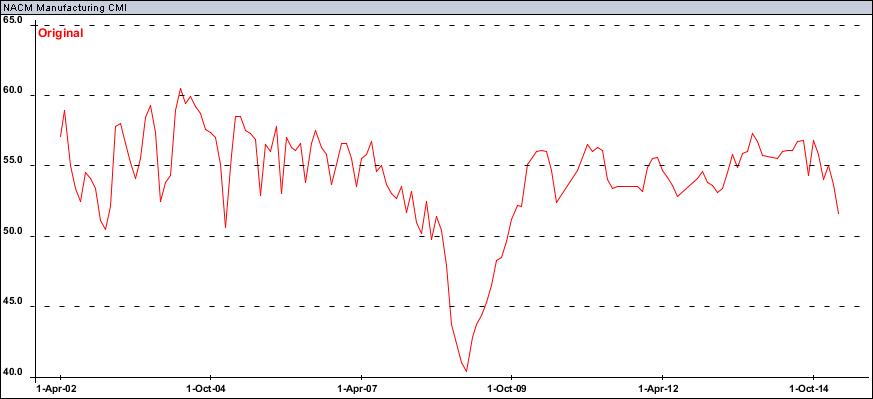

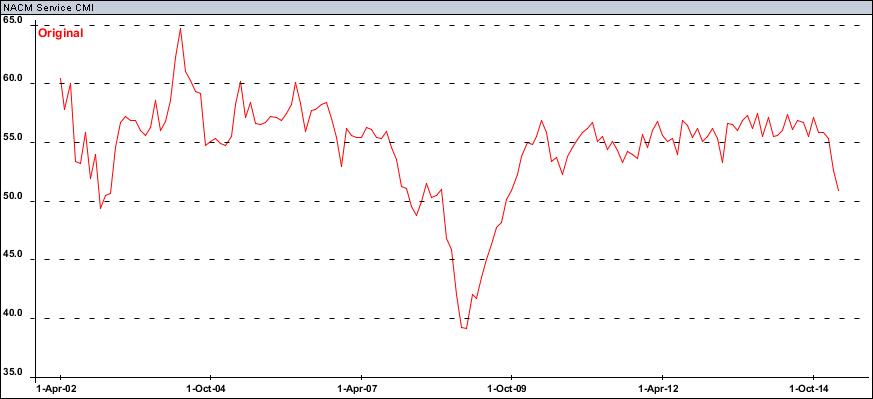

National Association of Credit Managers produces an excellent index of credit conditions - Credit Managers Index (CMI)[5]. It is published since February 2002 on last day of the month for the previous month:

“The CMI is created from a monthly survey of U.S. credit and collections professionals. The survey asks participants to rate whether factors in their monthly business cycle — such as sales, new credit applications, accounts placed for collections, dollar amount beyond terms — are higher than, lower than, or same as the previous month. The results reflect the entire cycle of commercial business transactions, providing an accurate, predictive benchmarking tool.”

It is indeed an excellent leading indicator which is not revised and which predicted both the start of the GFC at the end of 2007 and subsequently early recovery exactly at the end of February 2009. Below is the combined (Manufacturing + Service) index:

As you see, the recent deterioration in February and surprisingly March is pretty significant and unlikely can be explained by weather (there is definitely nothing like this last year and we are looking at March data already).

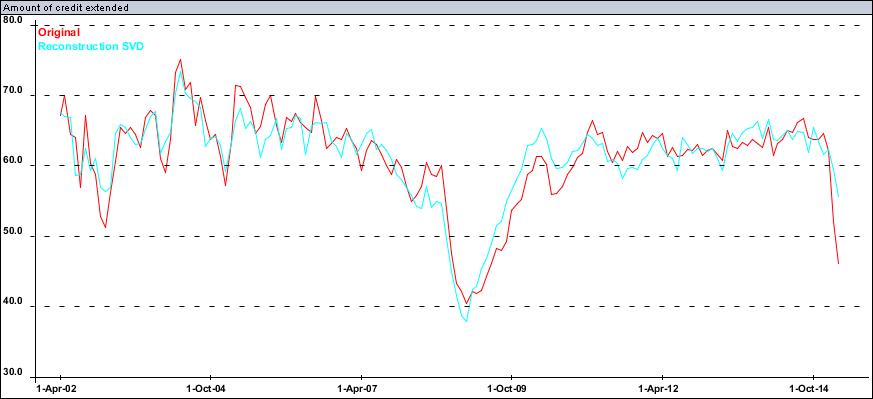

The most shocking deterioration is in the “Amount of credit extended” subcomponent (red). It is compared to the index (aquamarine) on the chart below:

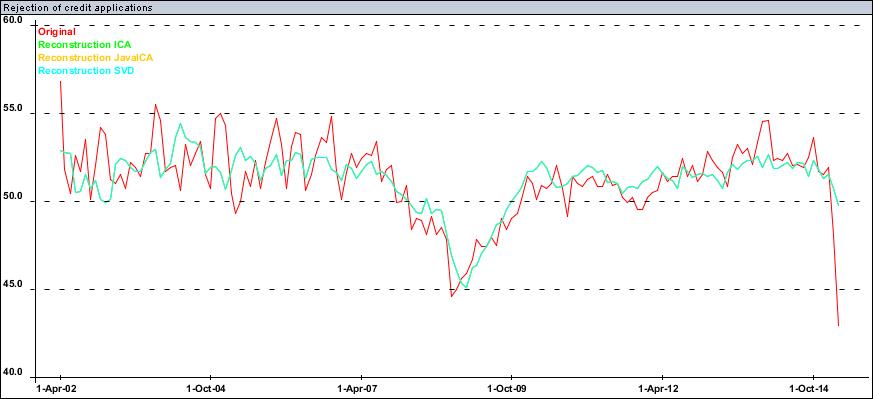

Similarly for the “Rejection of credit applications” subcomponent (red)

“Boy that escalated quickly...” From the above it appears we are experiencing some kind of mini credit crunch for the very least. Supposedly expectation of rate hike produced serious tightening in business lending conditions.

Similar picture is observed in both Manufacturing and Service indices:

So it is not just manufacturing or commodities/oil related!

Let me wrap with a few insightful quotes from Credit Managers Index March report released today[6]:

“We now know that the readings of last month were not a fluke or some temporary aberration that could be marked off as something related to the weather. There is quite obviously some serious financial stress manifesting in the data and this does not bode well for the growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound.”

“The most drastic fall took place with the unfavorable factors that indicate the real distress in the credit market. It has tumbled from 50.5 to 48.5 and that is firmly in the contraction zone — a place this index has not been since the days right after the recession formally ended. The signal this sends is that many companies are not nearly as healthy as it has been assumed and that there is considerably less resilience in the business sector than assumed.”

“As stated earlier, the real concerns start to manifest with the unfavorable categories. The rejections of credit applications fell out of the 50s with a resounding thud — going from 50.3 to 43.8. There is most definitely a credit crunch underway and it is now easy to determine what the prime factor is. There are many companies seeking credit that are too weak and there is obviously an abundance of caution showing up in those that issue that credit.”

“The big news is access to credit. It is suddenly very hard to get and this looks like the situation that existed at the start of the recession in 2008. The overall economy didn’t look all that bad in late 2008, except that there was a dearth of credit and that soon led to business failures and struggles.”

“The pattern is the same whether one is discussing the manufacturing or service side — too many seeking credit that are not going to get what they are seeking — either because there are doubts as to their credit status or because those issuing credit are in a very cautious mood.”

So, it does not look pretty. Reading the whole 7-pages of the report is pretty insightful. It only provides data in tabular format for the past year hence above I looked at the data visually since 2002 when the index was established.

www.dynamikacapital.com/subscribe

© Dynamika Capital L.L.C.

[1] Dynamika Commentary, “Is US sliding into recession?”, 28 January 2015

[2] Dynamika Commentary, “US vs G7: Decoupling? Recoupling!”, 4 February 2015

[3] Dynamika Commentary, “Unsettling interplay of leading indicators”, 24 December 2014

[4] https://www.frbatlanta.org/cqer/researchcq/gdpnow.cfm

[5] http://web.nacm.org/cmi/cmi.asp

[6] “Report for March 2015”, National Association of Credit Management, 31-March-2015