US Equity Market Review For the Week of March 23-27; Hey, We're Still Consolidating, Edition

Writing about market consolidation is very difficult. There are no strong rallies, massive volume spikes or huge losses to get the reader excited. Instead, the entire analysis focuses on prices pin-balling between two trend lines, usually on decreasing volume and weakening technical indicators. So if you’re looking for an article the grabs your attention by telling a story of an incredibly strong surge in bullish price action, move elsewhere. Because this week we again have a market that is consolidating.

Let’s begin by looking at the daily SPY chart:

The two longer term uptrends remain intact. Prices are still above the trend lines that connect the lows of mid-April and mid-December (the red dotted line) or the lows of mid-December and late January). Recent action has occurred between the upper and lower lines that form a triangle consolidation pattern (the dark black lines). Because periods of low volatility are usually followed by higher volatility, the most important indicator is the lower reading of the constricting Bollinger Bands. Although this hints the market is near a breakout, it doesn’t provide any indication as to timing or magnitude. The other indicators are neutral.

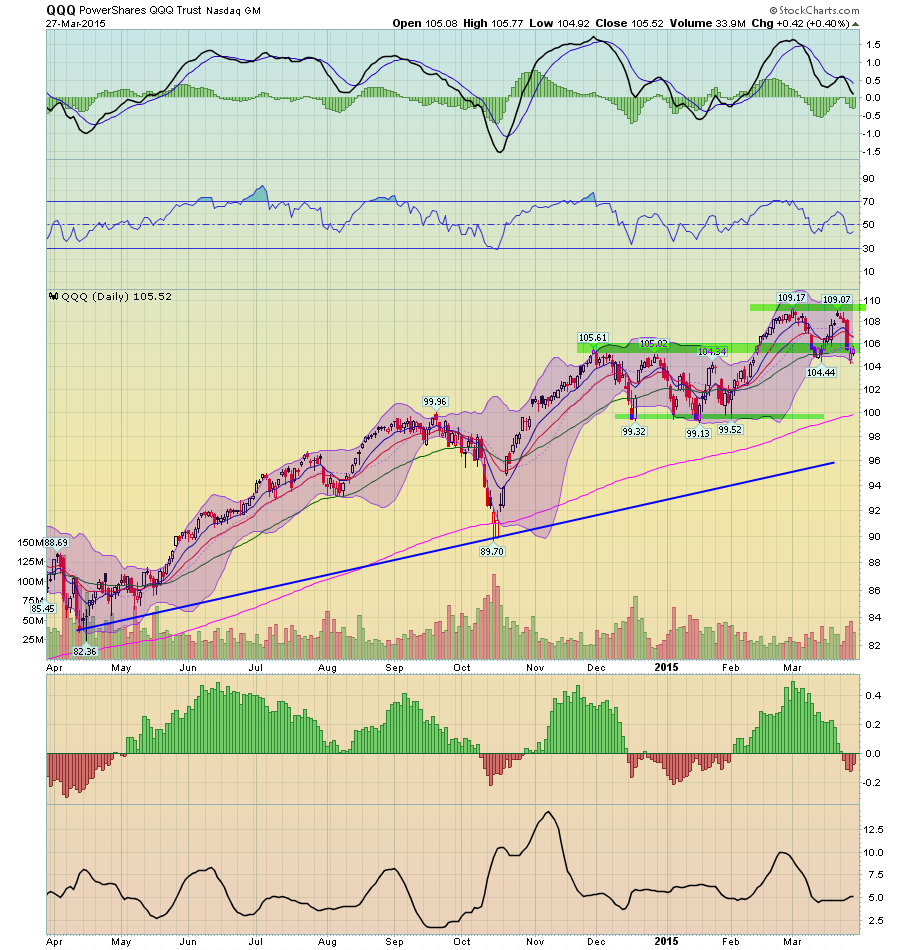

But the SPYs are not the only index consolidating. The NASDAQ is as well:

In fact, the QQQs have two recent rectangle consolidation patterns. The first lasted about three months and occurred between ~99 and ~104-105 price levels. The second, which began last month, is ongoing. But the uptrend that connects the mid-April and mid-October lows is still intact, indicating the overall trend is still up.

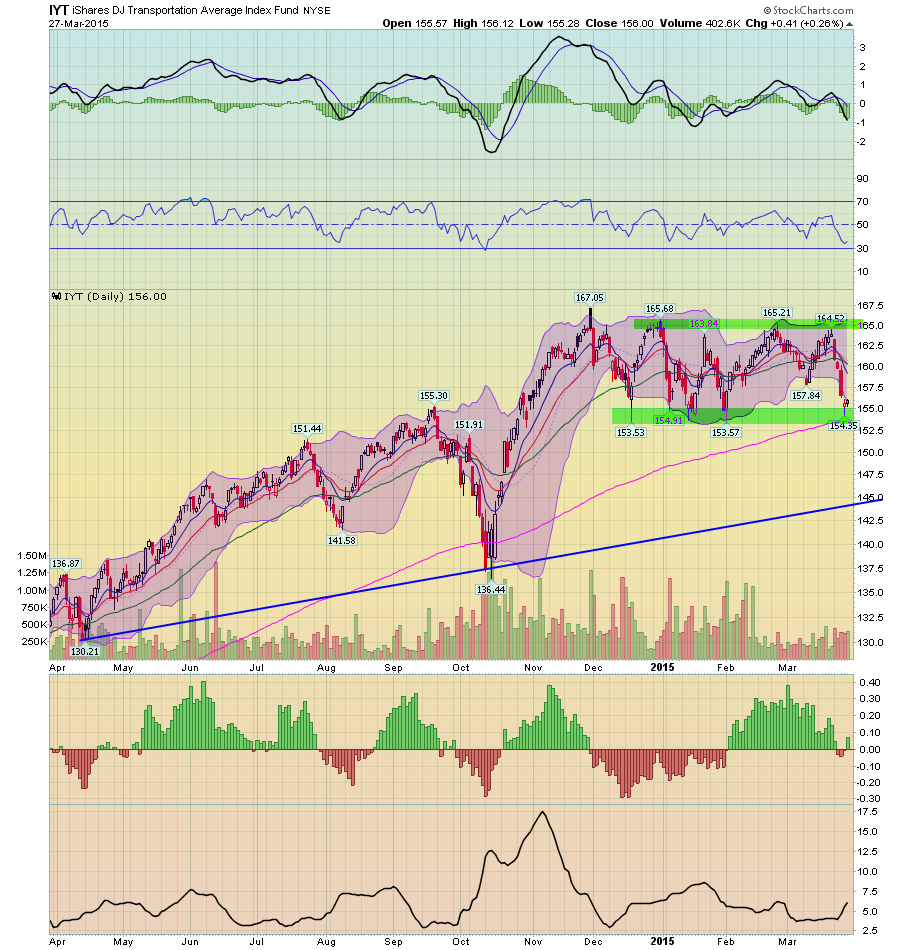

And then there are the transports, which began the consolidating trend.

Prices on this average have stabilized between the ~153 and ~165 price level for the last four months.

The underlying fundamentals provide ample reason for the sideways moves of all three averages. P/Es and P/Bs indicate the market is expensive. The latest GDP report indicated corporate profits decreased in 4Q15:

Profits from current production (corporate profits with inventory valuation adjustment (IVA) and capital consumption adjustment (CCAdj)) decreased $30.4 billion in the fourth quarter, in contrast to an increase of $64.5 billion in the third.

Profits of domestic financial corporations decreased $12.5 billion in the fourth quarter, in contrast to an increase of $16.1 billion in the third. Profits of domestic nonfinancial corporations increased $18.1 billion, compared with an increase of $32.0 billion. The rest-of-the-world component of profits decreased $36.1 billion in the fourth quarter, in contrast to an increase of $16.5 billion in the third. This measure is calculated as the difference between receipts from the rest of the world and payments to the rest of the world. In the fourth quarter, receipts decreased $36.5 billion, and payments decreased $0.4 billion.

The report further indicates that the higher dollar is the main culprit of the revenue slowdown, as seen in the $36.1 billion drop in rest-of-the-world (read international) earnings. And analysts are projecting that 1Q15 won’t be any better:

Analysts predict that profits for the S&P 500 companies will be down 4.6% from the first quarter of 2014, according to data from FactSet Research. This would be the first time profits have fallen since the third quarter of 2012.

Earnings are the mother’s milk of the market. Decreasing earnings points to weaker prices.

Adding to the market pressure caused by weaker earnings are several macro-economic developments. Durable goods orders have been weak for the last 4-5 months and industrial production has recently printed weaker numbers. In the last two months, the six-month rolling average of the leading indicators has decreased from a little over 3% to a little over 2%. Individually, none of these are fatal. When considered together, they at worst point to weaker GDP. But they are also tangible indicators of some weakness, which further drags down prices.

The conclusion to draw from the above charts and indicators is the same as that for the last few months: the market is expensive, making upward moves difficult. And weaker corporate earnings add downward pressure, as does the slight spate of weakness in several manufacturing numbers. But we’re nowhere near a recession, as indicated by the positive yield curve and still rising LEIs.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis