Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

A couple of days ago BIS (Bank of International Settlements) released a seminal research piece “Global Asset Allocation Shifts” in which authors explain that weekly institutional and retail portfolio reallocations (not just fund flows) of U.S. investors are 90% driven by two factors easily identified as Yen (Risk On/Off) and Dollar factors hence reaffirming our Global Macro Framework. They also explore systematic predictability of these factors in great details.

We recently shared our Global Macro Framework[1] which basically explains that most of the variance in the major global asset prices (somewhat U.S. centric) and assets prices themselves are explained by Global Carry, Yen and Dollar factors. Two days ago BIS released a seminal research piece[2] in which they effectively identify Yen (Risk On/Off) and Dollar factors as two dominant drivers of US institutional and retail portfolio reallocations. From the abstract:

“We show that global asset reallocations of U.S. fund investors obey a strong factor structure, with two factors accounting for more than 90% of the overall variation. The first factor captures switches between U.S. bonds and equities. The second reflects reallocations from U.S. to international assets.”

From the introduction:

“Our first contribution is to document a striking pattern in international portfolio reallocations of fund investors: Global asset allocation shifts obey a strong factor structure, with two factors accounting for more than 90% of the overall variance of reallocations. The first factor captures around 80% of the overall variance and can be interpreted as a rotation (ROT) factor: It tracks rotation out of U.S. bonds and into U.S. equities. The second factor tracks shifts out of U.S. assets (bonds and equities) and into foreign assets. This factor captures reallocation decisions driven by international diversification motives (DIV) of fund investors.”

This makes it pretty much clear that

ROT = Yen factor (Risk On/Off)

DIV = Dollar factor

Where is the Global Carry factor? As it lifts all assets simultaneously lifting aggregate wealth gradually it is mostly normalized out in BIS procedure:

“Hence, allocation shifts will always be measured relative to aggregate wealth, which we refer to as the wealth-weighted asset reallocation in the remainder of the text.”

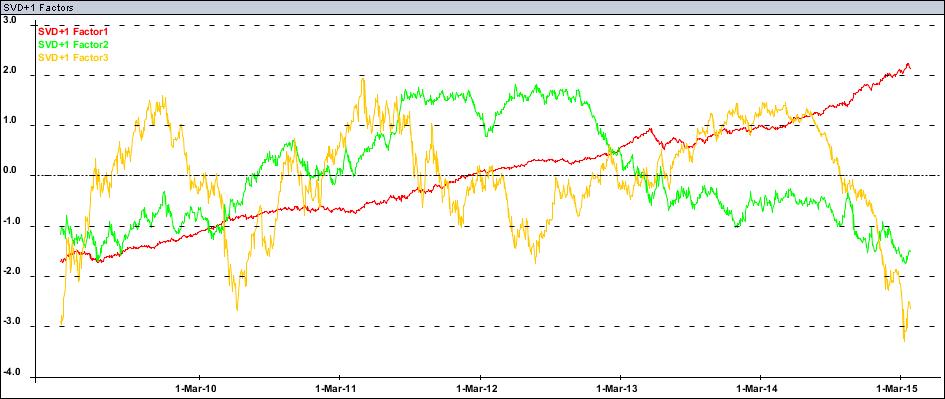

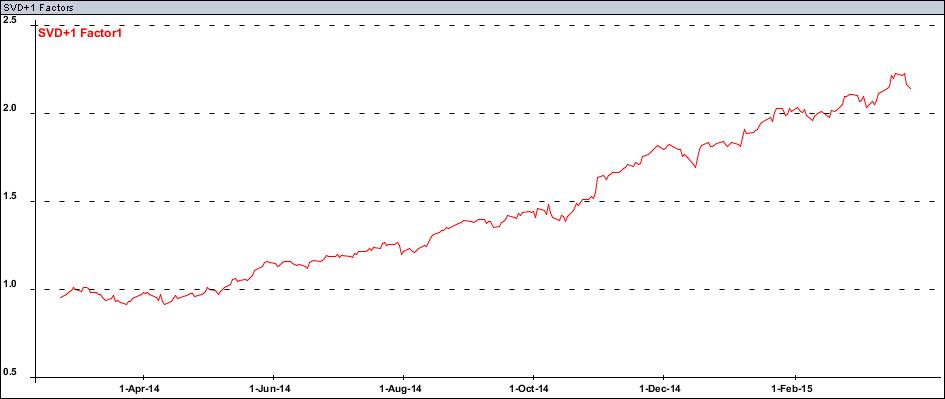

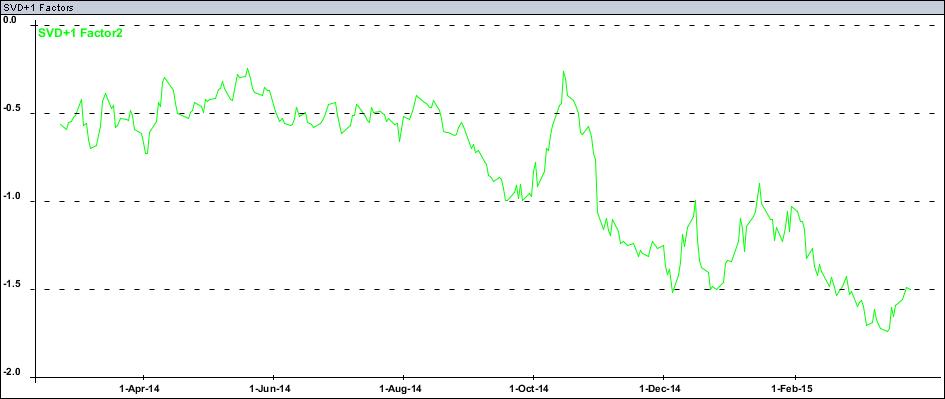

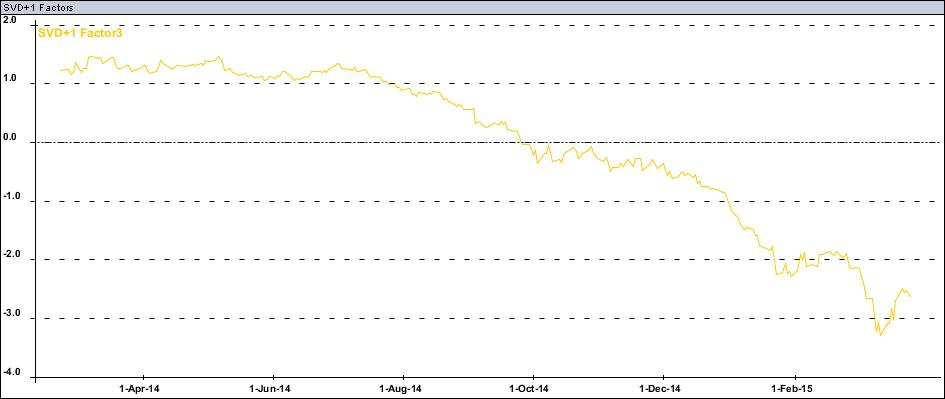

I think that settles it. Let us quickly review where we stand in terms of Global Carry (red, inverse sign), Yen (green) and Dollar (yellowish, inverse sign) factors:

Or zooming in on the past year

As you can see above contrary to the first three weeks of March when major player was the Dollar factor crashing and subsequently lifting US equities this week is different. The dollar factor is on sidelines while Yen factor reversion brought Risk Off volatility and Global Carry Factor in experiencing a correction.

Let me conclude with the second part of the BIS paper abstract:

“Portfolio allocations respond to U.S. monetary policy, most prominently around FOMC events when institutional investors reallocate from basically all other asset classes to U.S. equities. Reallocations of both retail and institutional investors show return-chasing behavior. Institutional investors tend to reallocate toward riskier, high-yield fixed income segments, consistent with a search for yield.”

There is great wealth of information and insight on how Yen and Dollar factors work and how they relate to FOMC announcement (which makes them predictable) and other phenomena such as search for yield and yield curve shape. I encourage you to delve deep into that seminal piece of research.

[1] “Global Macro Framework”, Dynamika Commentary, 11-Mar-2015

[2] “Global Asset Allocation Shifts”, BIS Working Paper No 497, 24-Mar-2015