Outlook Review

The United States forecast is for solid average annual economic growth of 3.1% in 2015 -- fastest in the economic recovery to date overall, although areas of the economy with high energy or international exposure will likely encounter headwinds. Strengthening employment conditions, continual improvements in consumer finances and steadily rising housing markets are likely to reestablish the consumer’s lead role in the U.S. economy in 2015. The U.S. unemployment rate is expected to remain on a declining trend from 5.7% in January to nearly 5% by year-end. Overall labor compensation gains will likely increase, and labor force participation is expected to improve, especially for those with skills in high demand. Low energy prices should provide an added boost to inflation-adjusted personal incomes in the coming months. Capital investment in equipment and structures is expected to grow at a solid pace throughout the year as domestic oriented businesses continue to benefit from rising revenue and cash flow growth generated primarily from the domestic economy. . However, slower foreign economic growth and a stronger dollar will likely slow export and profit growth.

The precipitous drop in energy prices resulting from sharp OPEC production increases and slower worldwide demand for energy will likely also put downward pressures on the energy extraction sectors in the U.S. in 2015 and generally slow capital investment in energy this year. U.S. federal spending will likely remain constrained by budget tightening efforts, but state and local spending is expected to accelerate gradually as a result of rising tax revenues. Conditional on solid growth in the U.S. economy and jobs in 2015, the Federal Reserve is forecasted to begin gradually raising its policy interest rates by the second half of the year. Consumer prices as measured by the overall CPI are being pulled down by sharp declines in energy prices, but the upward trend in U.S. inflation is expected to reassert itself by the second half of the year. Long-term interest rates are also expected to rise given firming domestic economic growth, but weakness in the international economy and central bank actions abroad are also putting downward force on long-term interest rates, keeping forecast risks for long-term interest rates elevated.

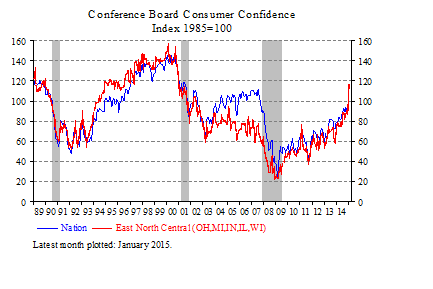

Consumer Confidence rises in the Midwest to its highest level since 2000

Where’s the Inflation?

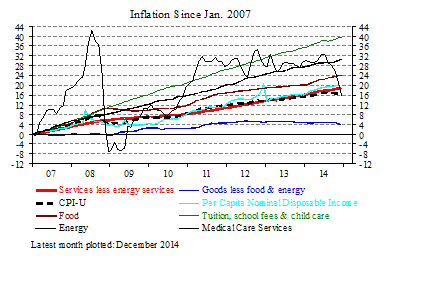

Since January 2007, average per capita nominal disposable personal income in the United States rose 20.4%. As evident in the chart below, most of the increase in incomes went to inflation, which rose 16.1% during the same period. Hence, the recent slide in energy prices is providing a substantial boost to consumer purchasing power.

Since July, the energy portion of the CPI has retraced over half of its 7 year climb in a short period of only 6 months. Further declines are likely in early 2015, providing a substantial total near-term boost to consumer spending power. In addition to declining energy prices, a rising dollar should put additional downward pressure on the price of goods excluding energy and food. However, goods inflation has been practically non-existent over the entire 7 year period since 2007, as the price of goods to consumers has risen only 4.0% during the period, as evident in the chart below.

Hence, where is inflation? Since Jan. 2007 it is in services. The total of services excluding energy services has been rising at a steady rate throughout the volatile ups and downs of the economy in the last 7 years, for a total 18.9% increase during the period, just shy of the 20.4% rise in average per capita disposable incomes. Services inflation was led by sustained strong price increases in the costs of tuition & child care (up 40%) and medical care services (up 31%), also shown in the chart below. In contrast to energy, services inflation has shown modest signs of accelerating in the last year, rising 2.45% in the 12 months through December 2014, up from 2.33% in the previous year. In addition to services, Food prices (up 24% since 2007) have shown steady annual increases more akin to the behavior of services than the typical volatile “commodity type” behavior of energy. In the first quarter of 2015, the overall consumer price index is expected to register another overall decline due to the recent large declines in energy prices and goods. However, with a strengthening economy fostering rising incomes, liquidity and pricing power, the core services inflation component is expected to continue in the 2.5% range this year, and accelerate further next year. Hence, inflation is forecasted to remain a risk in the long-term even as it may practically disappear from the radar screen of financial markets in 2015. Even with the benefit of recent sharp declines in energy prices, inflation will almost certainly continue to impact those with especially large budgets dedicated to medical care, tuition, food and other areas of services exhibiting sustained high inflation in recent years.

Monetary Policy

Substantial strengthening of labor markets in the last 4 months keeps the Federal Reserve on track for policy interest rate increases to begin in mid-2015. The Federal Reserve is forecasted to raise the Federal Funds rate target range from its long-held current target range of [0% to 0.25%] to [0.25% to 0.50%] after its 2 day FOMC meeting ending June 17. Subsequently, the Federal Reserve is forecasted to lift the Fed Funds rate target by about ¼ percent during each quarter, closing 2016 at 2.0%. A strengthening U.S. economy, a relatively low unemployment rate moving towards 5% and the likely continuation of solid money supply growth should set the stage for gradual monetary policy firming to begin. If labor market performance disappoints as a result of weakness in the international economy, then the first Fed funds rate target increase would likely be delayed until the September FOMC meeting. However, international headwinds are not expected to forestall modest firming of monetary policy this year, as long-term considerations of inflation and appropriate interest rates relative to economic growth will likely require the beginnings of policy interest rate increases.

Maintained somewhat higher than the Fed Funds rate target, the interest rate paid on excess reserves (IOER) will likely rise along with the Fed Funds rate target, and is expected to support the Federal Reserve’s monetary policy in a normalizing rate environment. The new Overnight Reverse Repurchase agreement (ON RRP) is potentially another policy interest rate tool in a rising rate environment, as it could be set precisely by the Federal Reserve, and it could put a firm floor under money market interest rates. Given the extraordinary levels of liquidity in financial markets, the actual Fed Funds rate will likely deviate more from the Federal Reserve’s target during the early stages of policy rate increases than it has done during past periods when the Fed Funds rate target was raised. The new monetary policy tools IOER and ON RRP should aid the Federal Reserve in reducing this potential volatility.

The Federal Reserve ended its outright purchases of securities after its October 28-29 FOMC meeting, although it plans to continue its reinvestment of principal payments on its portfolio into agency mortgage backed securities (MBS) and to roll over maturing Treasury bonds upon their maturity. According to Chairwoman Yellen in the September FOMC news conference, the Federal Reserve’s intention is to gradually reduce the size of its assets to a level consistent with no more than it needs to effectively perform monetary policy. This downsizing will likely take a significant period of time. Chairwoman Yellen estimates that the desired size of the Federal Reserve’s balance sheet won’t be achieved until the end of this decade. Hence, the Federal Reserve plans to maintain its large balance sheet and the monetary stimulus it provides for the next several years, even as it raises its policy interest rates. However, the Federal Reserve’s guidance on future monetary policy is based on their forecasts of economic developments, and their actual policy action(s) could change if developments in the economy or inflation differ from their expectations.

Recent FOMC statements emphasize the “data dependent” nature of future monetary policy. Hence, the guidance is for interest rates to be low for a “considerable” and therefore lengthy period of time, but actual policy will ultimately respond to events as they occur. This is probably the most significant monetary policy clarification from the October 28-29 FOMC meeting, and it is probably designed to anchor confidence that the Federal Reserve will do whatever is required to meet its dual objectives of low cyclical unemployment and inflation close to 2%.

The European Central Bank (ECB) will commence its much anticipated quantitative easing program comprising asset purchases of 60 billion euros per month commencing in March and ending in September 2016. The ECB will buy government bonds proportional to the size of the respective member economies, securities issued by European institutions and private sector bonds. The purchases will massively expand high-powered reserves in the Eurozone banks by over 1 trillion euros when completed. As has been the case with the activist monetary policies in the U.S. and Japan, the purchases will probably exert downward pressures on long-term interest rates worldwide. However, the Europeans have added a caveat to their monetary policy that has not occurred in the other major central banks – it charges the banks in its system 0.2% to hold the reserves that the banks receive as a result of the asset purchases. (Source: WSJ) Hence, European banks have an added incentive to lend out their reserves. The historically stimulative monetary policy of the ECB virtually assures inflation will reaccelerate in the eurozone. Low interest rates and a cheaper euro also add economic stimulus to Europe overall, but the success of implementing structural reforms in the stressed European economies will ultimately determine the success of the euro experiment in the long-term, in all likelihood.

The Bank of Japan (BOJ) has committed to continue its extraordinary monetary policy into 2015, which is the highest relative to GDP in the world. In contrast to the ECB and BOJ, the Bank of England is beginning to signal a potential tightening of monetary policy and lifting of policy interest rates to counter rising inflationary pressures in the United Kingdom. However, the overall trend for policy interest rates in 2015 may be downwards. Countries with large resource exposure such as Canada may continue to reduce their policy interest rates to offset pressures on economic growth created by lower commodity prices. Other countries may find reducing policy rates keep their respective currencies from appreciating to the point where exports slow overall economic growth. This will likely be the case for many of the major trading partners with the Eurozone in 2015. Hence, the European actions, like those of other major economies in the world, will likely set the monetary policy tone for the other economies worldwide in 2015. Pro-growth policies imply massive injections of liquidity worldwide and potentially in any country challenged by economic growth.

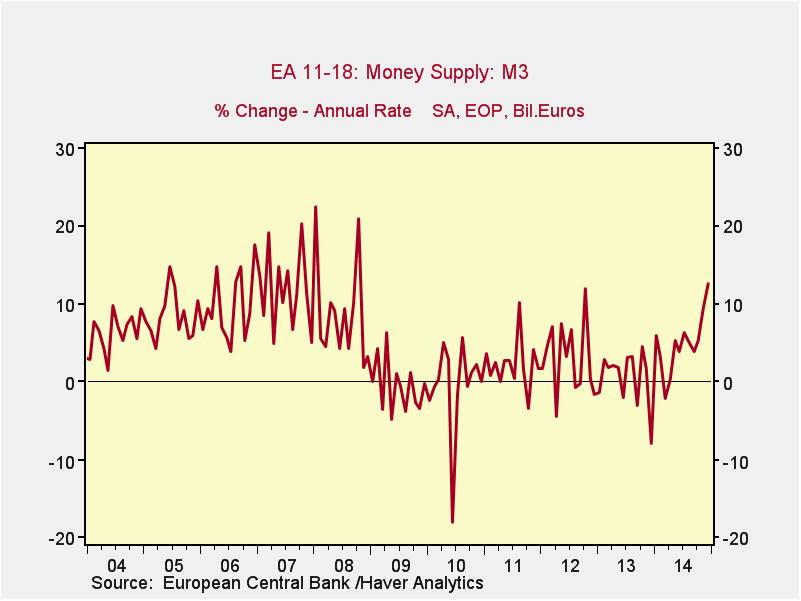

The Money Supply in Europe has begun to accelerate in response to aggressive ECB monetary policy designed to combat deflation and stimulate a moribund economy with unemployment over 11%

Dollar

The dollar exchange against major currencies is expected to continue gaining support from stronger U.S. economic growth and gradually firming domestic monetary policy. Much of the recent dollar gains have been due to the combined weakening of the euro and yen against most major currencies – a trend that could continue for the remainder of the year, albeit at a slower pace than the recent sharp cross-currency movements. The currencies of emerging market countries that have minimal domestic inflation risks and have continued to exhibit solid economic growth in the last year should continue to perform well in the next year overall.

Profits

Aggregate profits, excluding energy, should continue to grow in line with a stronger U.S. economy in 2015. However a strengthened dollar will likely benefit companies that do most of their business within the U.S. relative to those that maintain significant operations overseas. The energy sector overall will likely encounter a sharp decline in profitability in the near-term that should gradually reverse with an expected normalization of energy prices over the next 2 years.

Treasury Yield Curve

The short end of the Treasury yield curve will likely remain low and in line with the Fed Funds rate target and gradually lead the Fed Funds rate target in 2015. Long-term Treasury interest rates have been suppressed by weak economic growth, the Federal Reserve’s bond purchases, geo-political stresses, central bank interest rate policies globally including the recent ECB actions, weakening economies in Europe, Japan and China, and a general flight to quality created by uncertainties in the financial landscape. Despite the end of additional Federal Reserve bond purchases, high demand for Treasury bonds for liquidity, regulatory, or asset diversification purposes has probably put further downward pressure on long-term interest rates. These combined downward forces, including the recent sharp declines in government bond interest rates in Europe, have resulted in the 10-year Treasury interest rate declining below 2.0% in early 2015. However, the onslaught of downward forces has now largely been priced into bonds and is not likely to intensify further. Continued solidifying of the U.S. economy and labor markets are expected to reassert upward pressure on long-term interest rates in 2015, with 10-year yields advancing gradually upwards through 2016. This interest rate forecast hinges on containment of recent geopolitical crises and a gradual expected improvement in the world economy overall in the next 2 years.

Long-term risks: The Congressional Budget Office (CBO) projects federal debt held by the public to increase from 74.1% of GDP in 2014 to 78.7% in 2025. Federal Debt-to-GDP would likely be even higher should a recession occur in the next decade. A recession is not forecastable at this time, but history foretells it is likely to occur sometime within that time period. Furthermore, based on current CBO projections, federal debt relative to GDP begins to escalate substantially after 2025 based on demographic and government policy projections. Hence, long-term interest rate risks and the risks they might pose to the economy are probably high.

Key Economic Developments

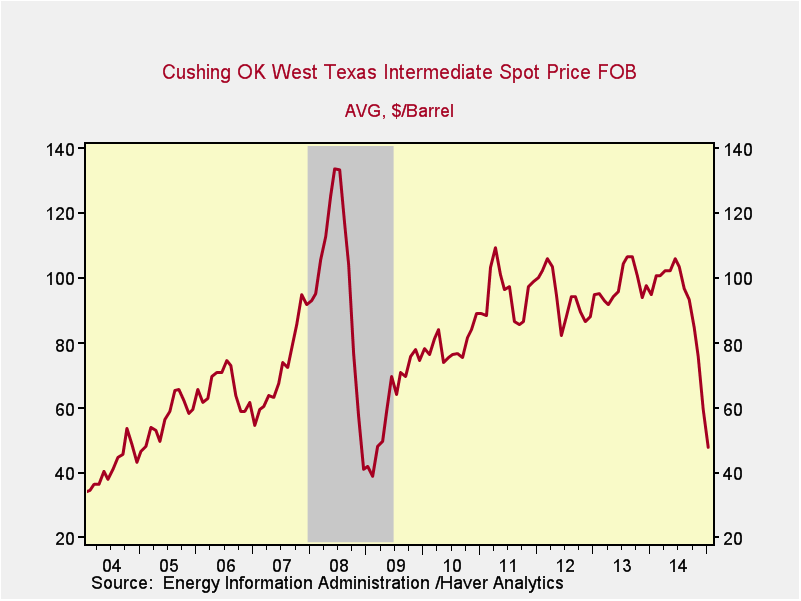

The price of West Texas Intermediate Crude Oil Drops to its lowest level since the Recession on both OPEC supply increases and demand decreases emanating primarily from a slower world economy

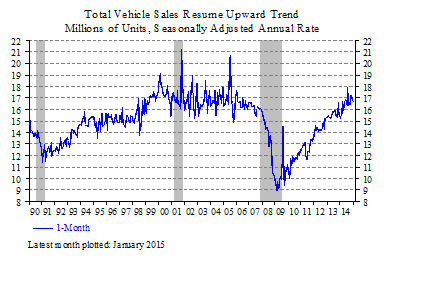

Auto sales remain brisk

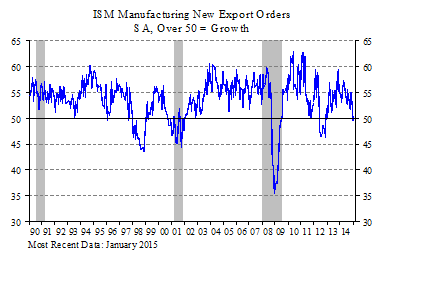

Export slowdown cools manufacturing in early 2015

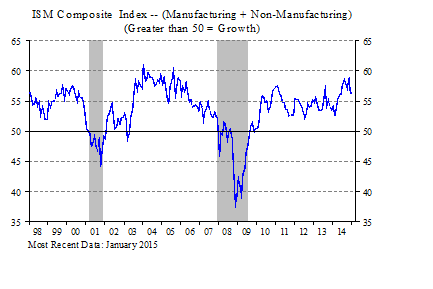

Overall economic activity still high despite international headwinds

Economic Risks

The risk of recession is relatively low in the next year as momentum in labor markets builds and expansionary monetary policy remains supportive of economic growth even if policy rates gradually begin to rise as forecasted. If oil prices remain at extraordinarily low levels for an extended period of time, then increased stresses could result in the energy sector. However, OPEC may damage to its own member states as well as the competition by continuing to produce at maximum levels. Hence, OPEC’s production levels will likely slow at some point for the political and economic interests of its members. Furthermore, world demand for oil has been restrained by unusually weak economic growth in the world overall and especially in Europe, Japan and China. With monetary stimulus rising abroad in 2015, economic growth and the concurrent demand for energy that it creates will likely begin to rise as the year progresses, pushing up the price of petroleum. Although forecast risks are high, a gradually rising price of crude oil is presumed in the forecast. The price of West Texas Intermediate oil has already risen off a possible floor of $47.52 per barrel in January to above $50 per barrel in February.

Policy uncertainty has been reduced at the macroeconomic level with passage of the 2014 federal budget and the lifting of the debt ceiling, but policy and international uncertainties are not likely to disappear in 2015. At the federal level, corporate taxation, regulatory policies and immigration policy will likely attain the highest degree of debate. Global debt in excess of $100 trillion in conjunction with slowing demographic trends in the United States and other developed economies probably poses the greatest known risk to sustained economic growth in the long-term future. High debt can ultimately deplete private sector expansion through its eventual impact on interest rates, taxation and the reduction of essential government spending. High debt also raises long-term inflation risks as high debt relative to GDP may require extraordinarily high levels of monetary stimulus to counter, as recently exemplified in Japan and most recently in the Eurozone. In the worst case scenarios, the Ukraine/Russia conflict and Middle East crises pose risks to the recovery, worldwide stability of energy markets and international commerce, especially to the regional economies directly impacted by the crises. The ongoing crisis in Greece also raises questions concerning the viability of the Eurozone, but Greece represents a small part of the monetary union and its possible exit would likely negatively impact Greece itself more than existing Eurozone members.

Positive Long-term Factors

Improving consumer balance sheets; strong corporate balance sheets; improving housing markets; improving average state and local government finances; strong potential export growth in the long-term; resurging manufacturing sector; natural gas and resource richness. The International Energy Agency projects the U.S. is probably becoming the top oil producer and could become energy independent by 2035 through its success in exploiting shale deposits.

Negative Long-term Factors

High long-term government debt and deficits; rising taxes; sharp near-term government spending cuts; slowing productivity growth; long-term risks to inflation, interest rates and exchange rates; geo-political risks; rising regulatory costs; weak real disposable personal income growth; cyber risks.

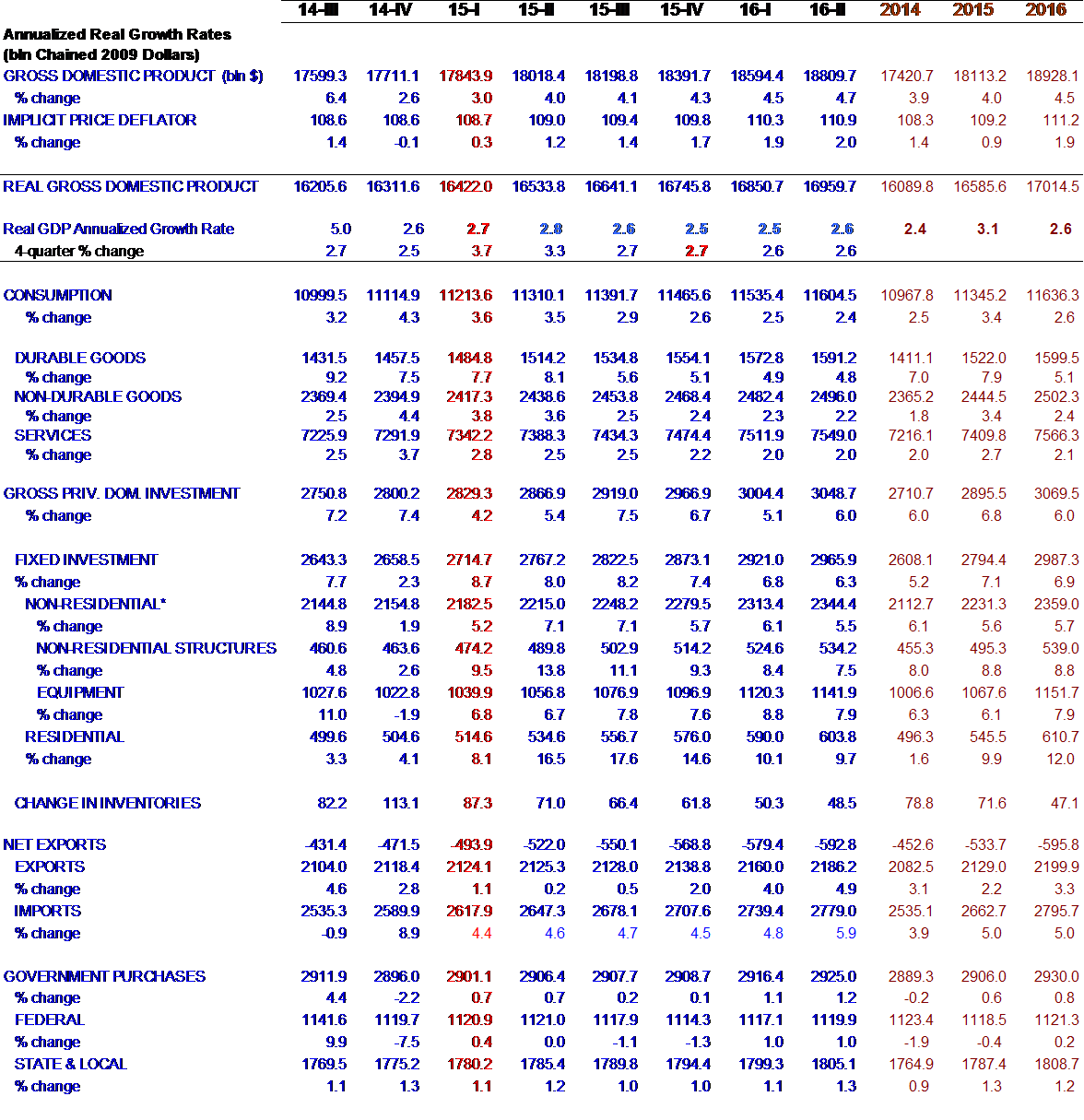

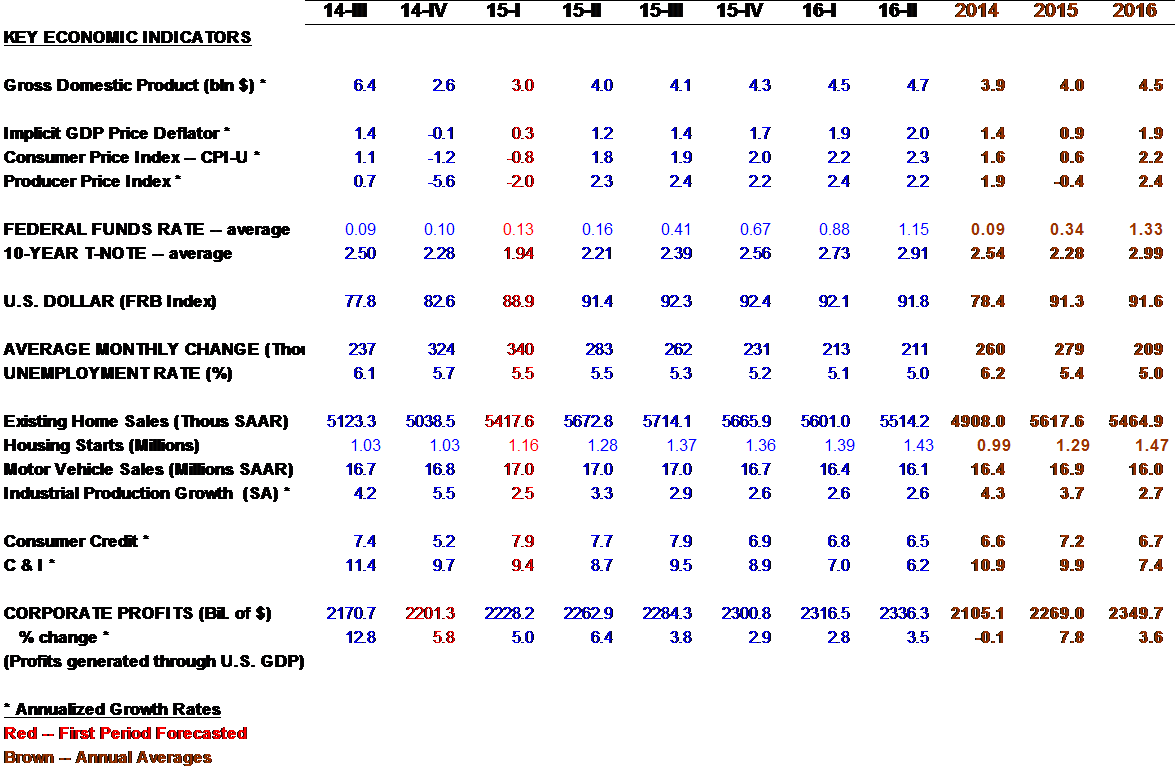

Table 1 (GDP Forecast – February 12, 2015)

Table 2 (Economic Indicators: November 21, 2014)

This publication contains general information: the views and strategies described may not be suitable for all investors, and individuals should consult with their investment advisor regarding their particular circumstances. Any forecasts presented are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Content herein has been compiled or derived in part from sources believed reliable and contain information and opinions that are accurate and complete. However, Huntington is not responsible for those sources and makes no representation or warranty, express or implied, in respect thereof, and takes no responsibility for any errors and omissions. The opinions, estimates and projections contained herein are as of the date of this publication and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Investing in securities involves risk, including possible loss of principal amount invested. Past performance is no guarantee of future results.

Huntington® is federally registered service marks of Huntington Bancshares Incorporated.

© 2014 Huntington Bancshares Incorporated.