When Hollywood tells a story, the expectation is that viewers are willing to suspend disbelief to fully immerse themselves in the plot. But when the market tells a story, suspending disbelief may result in overly complacent investors who blithely ignore the potential downside risk of a profit cycle in its later stages, which we see today through the lens of our full-cycle perspective.

Where do we go from here?

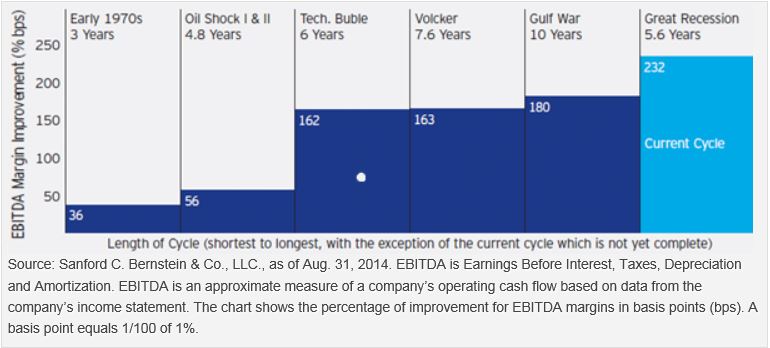

This cycle has seen substantial improvements in operating leverage, which has generated among the largest profit margin improvements in recent history — a robust 244% return on the S&P 500 Index since the bull market began in 2009.1 With incremental margins near historical highs, future returns become more reliant on multiple expansion and prudent capital allocation, particularly as management teams seek to extend the profit cycle.

Largest Profit Margin Expansion and Second Longest in 50 Years

When operating leverage naturally declines in later parts of the cycle, management teams look for other ways to generate returns, including:

- Merger and acquisition (M&A) activity, which has increased of late, with the number of deals surpassing prior peak levels. This is not surprising because low borrowing costs, improving management confidence and strong cash flows set the stage for M&A activity.

- Share buybacks, which have reached levels consistent with previous highs. Though we generally applaud the return of capital to shareholders via buybacks, we don’t believe this is always the best use of capital, particularly when companies are trading at heightened valuations. In this instance, we prefer the more conservative route of holding that cash for potentially tougher times. If given an option, we generally prefer to see returns of capital via steady dividend growth over time.

As value investors who manage portfolios today for success tomorrow, we can’t be complacent about the vast number of influences beyond corporate fundamentals impact stocks — sentiment, currency movements, financial leverage, credit spreads and external shocks, to name a few. In the second part of this series, I’ll look at areas where we see complacency in the marketplace.

For a more comprehensive analysis, please see the Insights titled Dividend Value Investing: No Time for Suspension of Disbelief. You may also be interested in information about Invesco Diversified Dividend Fund and Invesco Dividend Income Fund.

1 Source: Lipper, Inc. The return is calculated based on data from 3/9/2009 – 12/31/2014.

This is the first blog post of a three-part series. Part 2 looks at where we see vulnerabilities in the marketplace, and Part 3 will explore support factors for the market over the next several years.

Important information

Common stocks do not assure dividend payments. Dividends are paid only when declared by an issuer’s board of directors, and the amount of any dividend may vary over time.

Credit spreads are option positions in which the price of the option sold is greater than the price of the option bought.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

The S&P 500 Index is an unmanaged index considered representative of the US stock market.

Past performance cannot guarantee comparable future results. An investment cannot be made in an index.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.