As the temperature rises above 50 for the first time in several months, I am reminded of this Newtonian law that a body at rest will stay at rest unless an outside force acts on it. Perhaps the warm-up in weather is the “outside force” we all need to get moving again. I believe that the current market environment is similar to my body coming out of winter.

Outside Force

Global central bankers and their need to take action represent a changing force for asset prices. During the last 18 months or so, the Chairman of the European Central Bank, Mario Draghi, was in a position to describe what his fellow policy makers would do should the trajectory of economic growth in the Euro Zone not improve. What he was doing was buying time while he cajoled the countries of the EU into going along with his stimulus plan. Last month, he indicated that the talking period was over and he was about to do something. He announced a $1.3 trillion dollar (of course that was when the Euro traded above $1.25 now it trades closer to $1.05) bond buying program that actually began last week.

At the same time, our own Federal Reserve has gone from actually doing something, their quantitative easing program ended in the fall of last year, to talking about taking action, namely raising the Fed Funds rate. Markets have been in a tizzy over the timing of this action. But, let’s be clear. No action has been taken.

When Fed policy is operating normally bond investors worry about two things: The pace of economic growth and the level of inflation. Because of the Fed’s unusual action during the last six years, and the fact that they’ve added “full employment” as one of their mandates, investors have become obsessed with measuring unemployment and dissecting the Fed’s words.

If we turn back the clock to a normal period of Fed watching, we would pay attention to the fact that inflation is near 1% and the real gross domestic product for all of 2014 was 2.37%. Neither of these facts suggests a run-away economy that begs for higher interest rates. In fact, if we were to use the long-term average spread between the current rate of inflation and the 10-year Treasury, the 10-year would have a yield of less than 3%. Our own model calculates the fair value on the Treasury near 2.50% and today the yield is 2.09%. It seems that the longer end of the yield curve isn’t that far from reflecting the reality of today’s economic situation. However, there seems to be this groundswell of concern over significantly higher interest rates.

The Fed has a balancing act because as they discuss the need for higher rates, interest rates in Europe and Japan have declined even more. The U.S. 10-year Treasury yield is now 1.92% higher than the German equivalent and 1.69% above the Japanese equivalent. Higher rates in the U.S. will cause capital to flow in our direction further reducing the absolute level of interest rates.

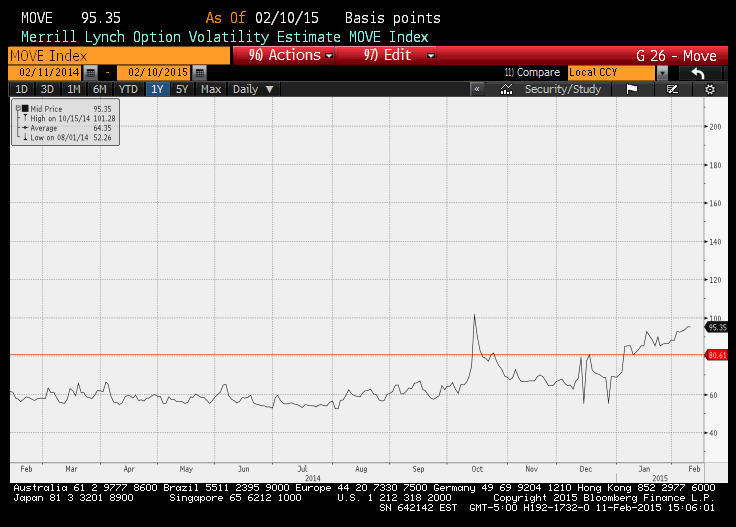

The divergence of central bank policies is the force that will get markets moving and we have seen this already. This chart shows the MOVE index, an index that indicates the level of volatility in the bond market. You can see that volatility has been on the rise as central bank policies diverge.

The Warm Up

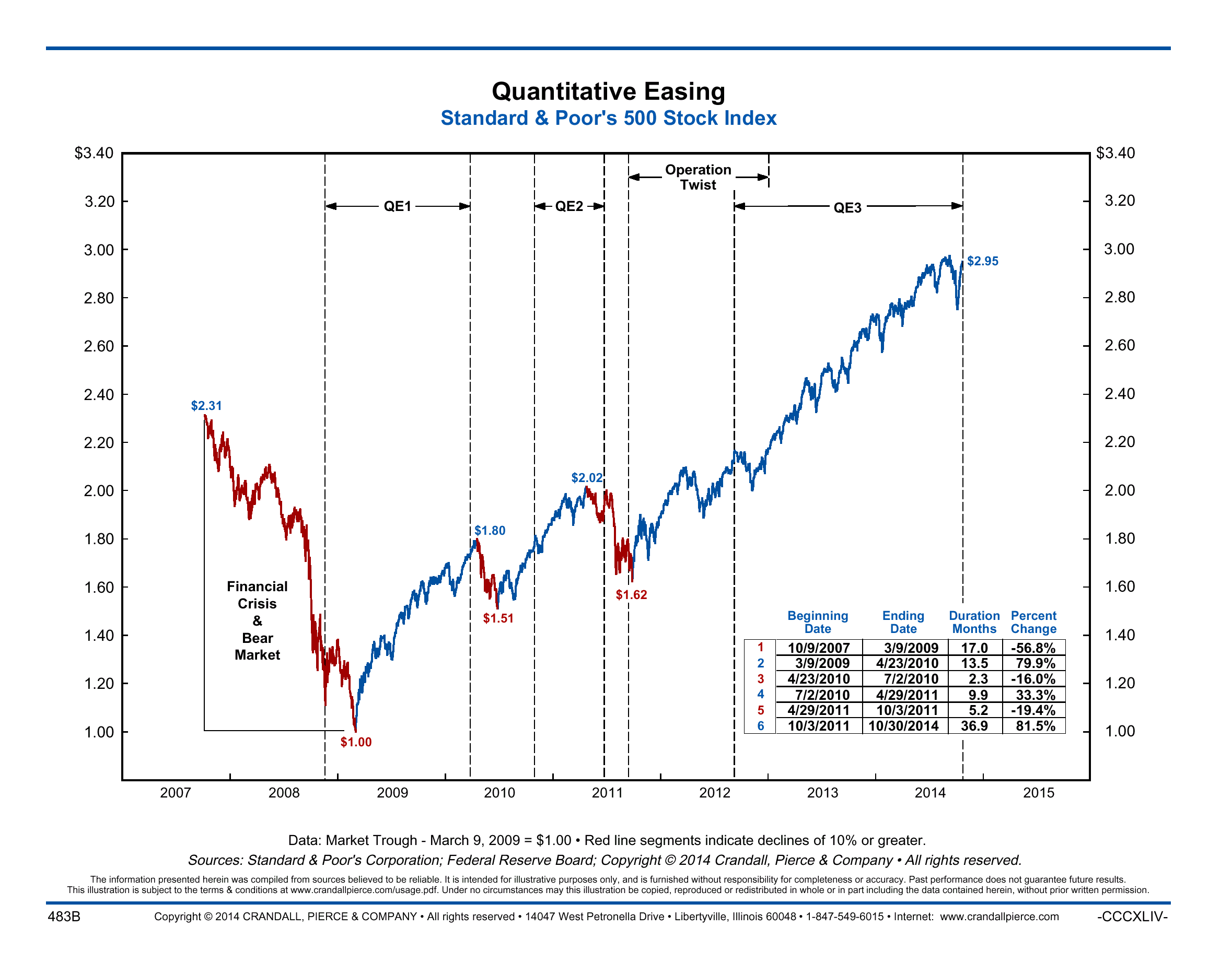

Foreign stock markets, particularly those in Europe and Japan have raised as a result of the newer stimulus policies of the ECB and Bank of Japan. The Euro Stoxx Index has risen over 10% since the beginning of the year while the Japanese Nikkei Index broached the 19,000 level last week for the first time in nearly 15 years. We have only to look at this next chart to determine what will happen to asset prices, stock prices in particular when central bankers use QE to stimulate their economies.

This chart plots the S&P 500 stock index and looks at past QE periods in the U.S. You can see that during each period the market rallied significantly. During the first period the rally was near 80%, 33.3% during the second and again over 80% during the third. If foreign markets follow the same path, then we can anticipate higher stock prices in those areas with the most stimuli.

Because the Fed has left QE behind, we can anticipate that U.S. stocks will begin to focus more on the fundamentals like earnings growth, than the policies of our central bank. To that end, the decline in corporate earnings growth should be a greater concern to U.S. investors than the flat year-to-date return of the S&P 500 Index. We will continue to monitor earnings revisions to see if the fundamentals become a greater force to be reckoned with.

There are many outside forces affecting asset prices, none it seems are as significant as the diverging policies of global central bankers.

(c) Cleary Gull