When looking at the broader investment backdrop and the most recent corporate earnings season, a few key themes emerge. From a macro standpoint, slower growth (particularly in many regions outside the United States), combined with the strength in the US dollar, has weighed on corporate performance. We have heard this from a number of US companies recently reporting quarterly earnings. The US dollar’s strength has clearly served as a headwind for many multinational companies because as the US dollar strengthens, it can adversely impact domestic firms with significant overseas revenue. On an aggregate basis, we have seen fairly modest revenue and earnings growth rates reported thus far, albeit with a fairly wide range of results across sectors. For example, we have seen stronger growth from companies in sectors such as technology, consumer discretionary and health care, especially biotechnology and health care services.

Notably within our growth-oriented strategies, one area where we are constructive is health care, particularly specialty pharmaceuticals and biotechnology. We continue to see very strong innovation, and research and development (R&D) results, which have been driving improvement in drug pipelines, and have been helping support the longer-term outlook for revenues and earnings growth. In addition, the merger and acquisition (M&A) theme is very important in the sector, and for us that goes beyond tax inversions and tax savings. We see the opportunity to improve inefficient businesses through better management execution. Advances in technology are improving the outlook for the health care sector, and that’s an investment theme we believe needs to be a continued focus.

In technology, we believe the proliferation of smartphones globally and the increased use of mobile computing create opportunities for investment across industries and platforms. Examples of such technologies include medical monitoring devices for diabetes, factory automation and consumer applications related to travel, gaming and social media. Valuations within the technology sector broadly remain attractive relative to their long-term growth prospects, in our view. The M&A theme is also prevalent in this segment as well; we believe M&A could serve to consolidate and strengthen the technology sector going forward. We have also observed an increase in technology companies returning cash to shareholders through dividends and share repurchase programs. All of these conditions contribute to our positive multiyear outlook for the IT sector.

US Market Outlook

In the year ahead, we remain fairly constructive on the outlook for the US economy and markets, given two important dynamics: the health of the consumer and the stimulus effect of lower input costs, most notably the rapid and significant decline in energy prices. We believe lower energy prices could have a very broad stimulus effect on a range of sectors and industries.

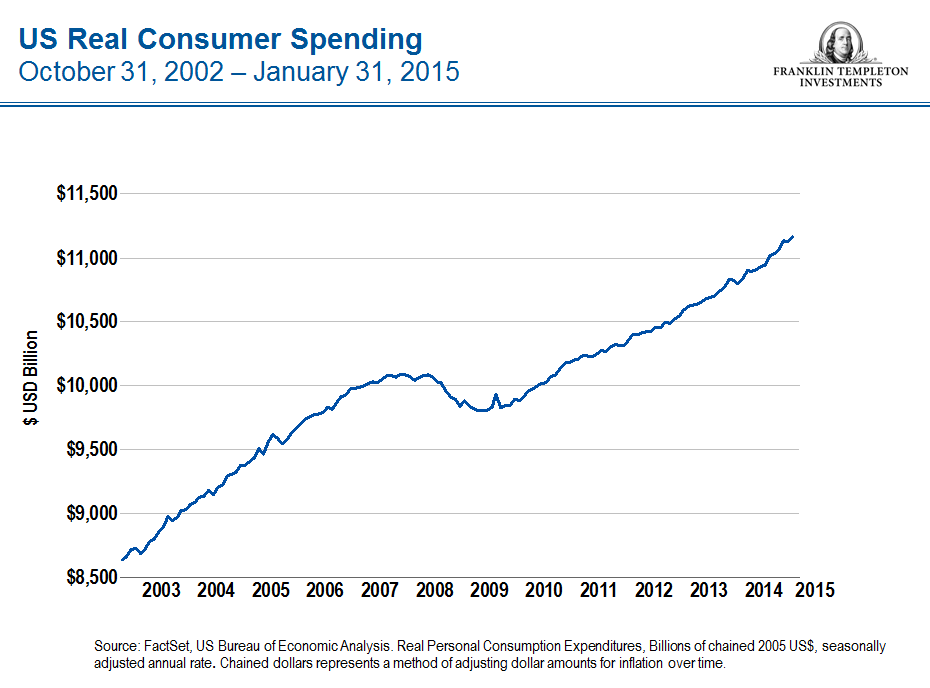

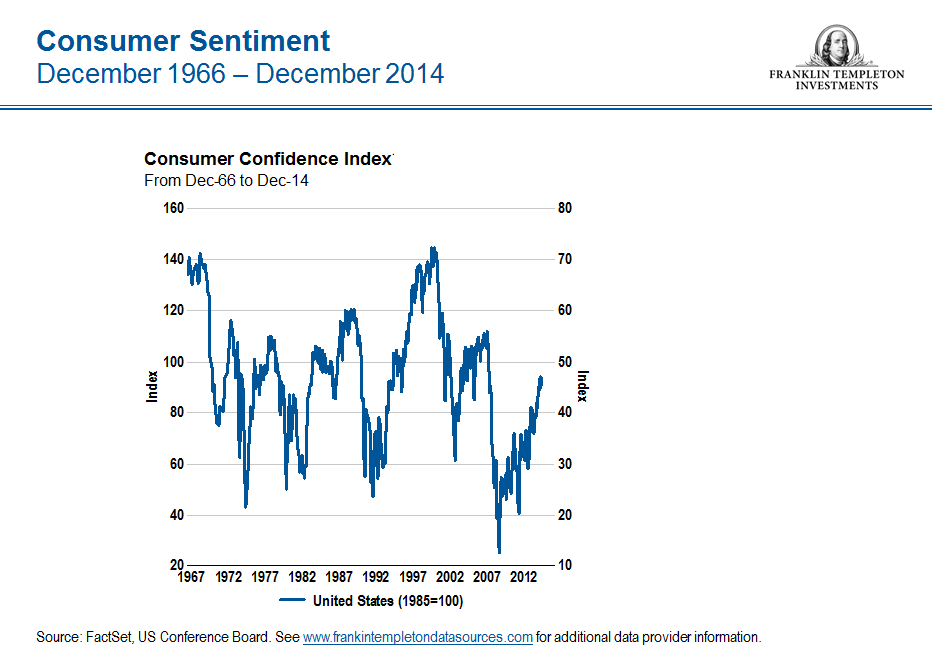

With regard to the US consumer, we see some clearly positive trends that appear to have durable traction, including job growth and rising consumer confidence. We believe the increases in capacity utilization broadly in the economy should continue to provide support for these measures throughout 2015. Though slower growth and other problems in markets outside the United States may make for buzzworthy headlines, it is important to note that the US economy is largely domestically oriented. While foreign markets certainly are important to many US companies, the consumer sector accounts for approximately 68% of the US economy’s gross domestic product, while exports represent roughly 13%. US consumers are in a healthier position than they were just a few years ago; consumer balance sheets have improved in tandem with US corporations, and consumer spending has resumed its upward momentum. Lower energy prices also provide a boost to consumers, as dollars otherwise spent at the pump can be allocated to other areas.

In addition to providing a benefit to consumers, lower energy input costs, in our view, should have a meaningful impact on manufacturing activity and on a range of industries that have historically shown negative correlations to energy prices, from transportation and automotive manufacturing to plastics and machinery. We believe lower commodity prices could benefit some domestically focused businesses and enable them to differentiate versus peers during a time of uncertain global growth.

Energy Sector Volatility: Uncovering Opportunities

Recent turmoil in the energy sector has given us the opportunity to focus on uncovering attractive investments tied to what I would describe as indiscriminant selling that tends to occur when a segment of the market experiences the level of volatility like we’ve seen in energy recently. I would characterize the action in energy stocks over the past few months as herd mentality at its worst. For us, it’s about identifying the good companies that are getting thrown out with the bad, and that’s been a significant focus of ours for the last several months.

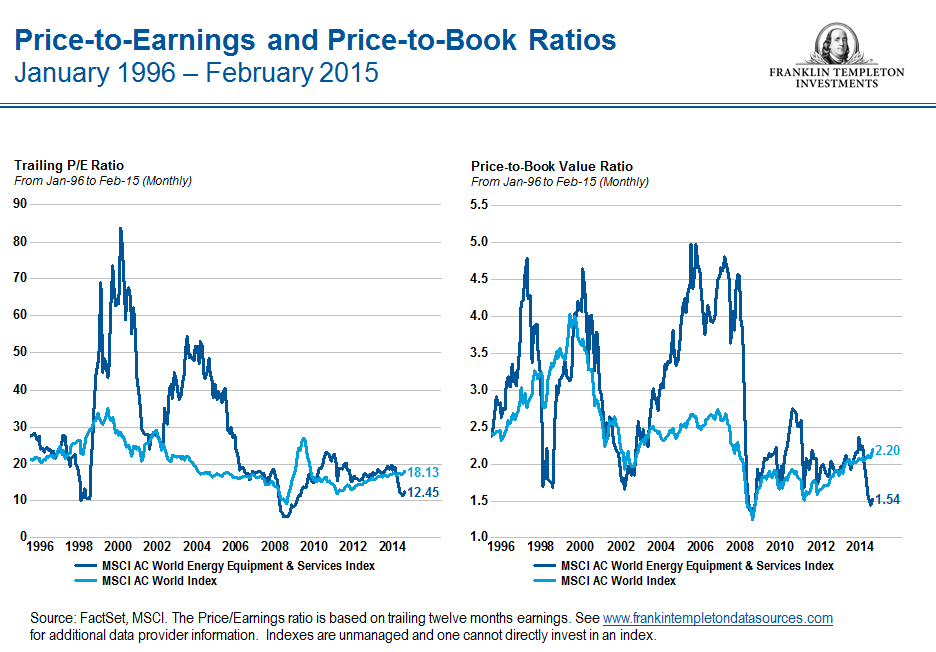

Relative to six months ago, incremental opportunities within the energy sector have surfaced in oil field services and equipment, where we have seen fairly significant declines as a result of meaningful upstream capital expenditure reductions. While the near-term outlook has certainly been hampered, the longer-term outlook for us remains positive for this segment of the energy market, largely due to the increased technical sophistication related to many new areas of production, combined with strong balance sheets and attractive dividends. I think this makes oil field services and equipment an attractive area for long-term investors.

A lot of companies can make money with $100 [per barrel] oil; however, in a world of $55–$65 oil, I think it’s far more important to understand the quality of the assets and the ability of management teams to drive down costs. These factors will be imperative to determining investment success in an environment of lower oil prices, so security selection will be that much more important looking forward. That’s where I believe active management can add value, particularly our bottom-up security selection process, which is the hallmark of our equity and hybrid strategies.

Portfolio Positioning: Views on Corporate Bonds and Convertibles

The strong equity market performance that we have seen generally over the past year has brought some opportunities for profit-taking. While we still believe in the potential for equities this year, in Franklin Income Fund and Franklin Balanced Fund, we have increased our focus a bit more on corporate bonds, largely as a function of what we see as a better opportunity set now, despite continued low long-term interest rates. We have seen increased volatility in credit spreads, which, in our opinion, has been driven somewhat by more technical factors like assets flowing out of the sector at times; that causes spreads to widen and the yield opportunity to improve. In the second half of 2014, for example, we saw yields increase fairly meaningfully across the broader high-yield corporate bond market. We do see a compelling opportunity, but we remain focused on our fundamental credit research effort in order to identify what we believe are the unique opportunities in that market. One additional point is in regard to the opportunity we currently see in convertible securities. Interest in issuing convertible securities to investors seems to have accelerated recently, which is something we are certainly watching and believe could present further opportunities for us in 2015.

(c) Franklin Templeton

http://us.beyondbullsandbears.com

© Franklin Templeton Investments