Municipal bond market volatility in early 2015 may have investors wondering if they should sell today and lock in their gains from 2014. After 13 consecutive months of positive returns, the muni market turned negative in February and the first two weeks of March as interest rates rose. After such a long and strong run, it is not surprising that the muni market has taken a step backward. That said, we do not see reason to panic and continue to believe that the muni market remains on sound footing due to supportive market fundamentals and technicals, as well as our entrenched high tax environment.

State and local financials continue to improve on the back of the gradually improving U.S. economy. While the strength of the global economy is in doubt, the U.S. economy continues to benefit from lower energy costs and interest rates, as well as from an improving labor market. As the economy gains steam and the employment picture slowly improves, tax revenues – sales, property and income – continue to increase. At the same time, a byproduct of the Great Recession is ongoing spending restraint. While there are some outliers (Illinois, Chicago, New Jersey, Puerto Rico), the overall muni credit picture is strengthening, and both S&P and Fitch recorded more credit upgrades than downgrades in 2014.

Market technicals are expected to remain favorable. While gross new supply has increased significantly over 2014, the net increase in issuance has been much more manageable. Much of the increase in gross supply is due to refundings (refinancing) of existing bonds. Refundings replace existing debt with new debt, leaving outstanding supply unchanged while lowering interest costs. In addition, the new supply that has come to market has generally been multiple times oversubscribed, indicating strong ongoing investor interest. Demand, which picked up in 2014, remains robust in 2015 as investors have poured over $10 billion into muni mutual funds through mid-March. While seasonal market factors may come into play, we do not expect a material negative impact.

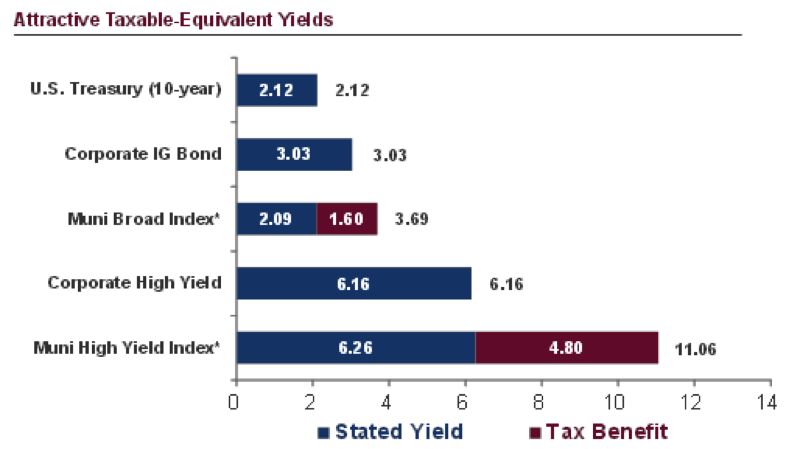

Finally, taxes. The higher the tax rate, the more attractive is tax-exempt income. Recent federal tax increases, as well as implementation of new taxes (such as the 3.4% Obamacare Net Investment Income Tax), means that investors are facing much higher tax bills. Income from municipal bonds, as always, is exempt from federal taxes, including the NIIT, leaving the taxable-equivalent yield of muni bonds higher than on Treasuries and most corporate bonds. We believe the attractiveness of municipal bonds’ after-tax yields will result in continued strong demand notwithstanding recent volatility.

Sources: Bloomberg (U.S. Treasury 10-year) and Barclays, as of March 12, 2015.

* Assumes a 2014 federal income tax rate of 43.4% (39.6% income tax rate + 3.8% Net Investment Income Tax rate). Other taxes are possible. The effect of potential federal income tax phase outs of personal exemptions and itemized deductions is excluded from this schedule. Had they been included, the reported tax rate would have been higher which would then increase the municipal taxable equivalent yield, for any given municipal stated yield. State income taxes may be applicable and can further reduce the after-tax returns of some municipal bond investments (depending on the state of residence). Income from certain tax-exempt securities may be subject to the federal and/or state alternative minimum tax for some investors. In addition, federal and state income tax rules will apply to any capital gain distributions and capital gains or losses on sales. When investing in municipal securities, investors in higher tax brackets can receive a greater tax benefit than those in lower tax brackets. Municipal bonds provide income exempt from federal and, in some cases, state income taxes.

Disclosure

The views expressed are as of 3/16/15, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Income from tax-exempt municipal bonds or municipal bond funds may be subject to state and local taxes, and a portion of income may be subject to the federal and/or state alternative minimum tax for certain investors. Federal income tax rules will apply to any capital gains.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2015 Columbia Management Investment Distributors, Inc. All rights reserved.

1150321