Dear Fellow Investors,

March 10th is one of my favorite days of the year. The tech bubble of the late 1990's burst on March 10th of 2000 and the biggest bear market of my career (2007 peak to 2009 low) bottomed on March 10th of 2009. There is a great deal to learn from those two dates in history as it pertains to the way secular bear markets work and how long it takes to move from the most popular investment in the world to being completely out of favor.

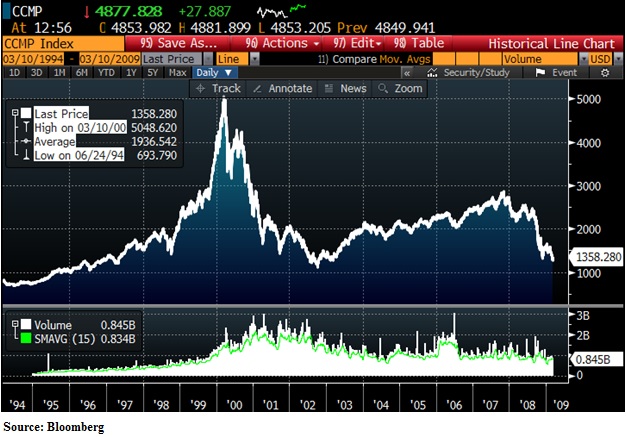

Let’s start with the historical chart of the tech-heavy Nasdaq Index:

We believe the first and most important part of a secular bear market is the enormous price increase prior to the top in March of 2000. Tech stocks had earned amazing adoration and belief with spectacular stock market returns.

During the first three years of the secular bear market in tech stocks, investors bought heavily all the way down. Notice the very sharp bear-market rallies in 2001 through the bottom in 2003. Dramatically lower prices and an expected recovery in earnings growth were the lure, but heartache was the end result. Now observe how little absolute and relative reward occurred through nine years of a secular bear market and then think about the opportunity cost to investors. With the Nasdaq chart in mind, take a look at the long-term oil chart below:

What did this mean for investors in the oil patch in the U.S. on March the 10th of 2015? A move in oil prices from $11 per barrel to a peak around $145 was a great start to a secular bear market. See the similarity of the parabolic move in prices to the tech stock bubble. Even worse to us is the ability to stay above $100 per barrel long after the supply and demand dynamics had changed by June 20th of 2014.

Now consider what the first leg of the bear market has accomplished in oil; just like in tech stocks, there has been an enormous decline in crude oil prices. This is in the early stages of what looks like another secular bear market to us. Are investors buying into the oil patch on the way down in a similar pattern to tech stocks in 2001-2003?

Thanks to terrific writing in the Wall Street Journal we have part of the answer from a piece called, “Investors Are Buying Stocks and Bonds From Energy Producers Amid Oil Price Drop.” Here is its thesis:

Investors are snapping up new stock and bonds from energy producers as they search for bargains amid the tumult caused by the plunge in oil prices.

The buyers are betting these companies can ride out the slump in crude and natural gas. Meanwhile, by selling stock now, companies are signaling they don’t see a quick rebound in commodity prices that would ease their funding woes and lift their shares.

The run up in tech stocks in the 1990's was built on the back of what we call a "well-known fact.” The fact was that the Internet was going to change our lives. This fact was used to justify irrational, and in some cases, infinite price-to-earnings ratios for tech stocks.

The "well known fact” in oil stems from the love affair investors came to have with what portfolio manager Bill Miller coined, "the globally-synchronized recovery." This was the idea that the uninterrupted growth in China and other emerging markets would create more than 400-500 million new middle class citizens of the world. The media dwelled on this fact and early investors in it were trotted out constantly to reinforce the message.

While many tech stock investors in 2001-03 felt that they could "ride out the slump" in tech stocks to get at longer-term rewards, other individual and professional investors felt like pioneers who were part of an intellectual property land grab. These new middle class folks, who are the centerpiece of the "globally-synchronized recovery," are believed to want everything that developed-country middle-class citizens already enjoy. This includes similar types of food, clothing, shelter and automobiles. The demand for commodities like oil was to these investors as endless and wide as the Internet was in changing our lives circa 1999.

The problem for oil worshipers, like tech stock fanatics, is that in economics price regulates price. Every Tom, Dick and Harry with a background in venture capital and computer science made it their life goal to ride the tech wave in the early 2000s. Every Tom, Dick and Harry of 2010-2014 attempted to profit from the oil boom and wanted to be the King of Shale. I can still hear the “oilboomUSA.com” advertisements from satellite radio ringing in my ears.

The problem for fans of the “more people” argument in rising oil prices was that it severely dampened economic growth in the U.S. and all over the developed world. Oil above $100 per barrel broke the back of Peak Oil theory (again), because folks everywhere were highly incentivized to poke holes in the ground and drill for oil expanding supply, thereby ultimately reducing price.

Charlie Munger says, "Competition is the enemy of competence." Nobody in the oil business had any competence in June of 2014. Based on the research from the Wall Street Journal, the competition is not disappearing in a way which could stop the secular bleeding. Just look at the rig count in the U.S. the last fifteen years:

Mark Twain said, "History doesn't repeat itself, but it does rhyme." We agree with the oil producers selling stocks and bonds early in this secular industry decline, who think we are years away from a bottom. Until the rig count drops closer to where it was in 2006-07, we don’t think investor psychology will match up with the long-term investment opportunity. When stocks like Schlumberger (SLB), Chevron (CVX) and others are as hated as today's major bank stocks and are being treated like their owners are miserable fools, we hope to go shopping. Look at this telling statistic from the Wall Street Journal:

U.S. and Canadian publicly traded exploration-and-production companies have sold more than $8.4 billion of new stock since the start of the year, a pace fast approaching the $10.5 billion of stock the group sold during all of 2014.

This has important implications for value investors. Normally a substantial price drop and insider buying would get us interested in a sector of the S&P 500 Index which has been drubbed like the oil sector has. However, we are very conscious that value traps exist based on being years early investing in a sector that may have not yet had its darkest hour in the eyes of investors. In our view, we are still early in the energy sector as it moves from sheer excitement and enthusiasm to contentiousness and utter distaste. We will continue to wait for better prices and the day when most professional investors see no future success in the arena.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.