During the global financial crisis, communication and coordination amongst global central banks was de rigueur. Now that we are six years into the financial market recovery, the focus is more localized and the esprit de corps has faded. National efforts to combat unemployment and deflation have led to negative interest rates and accusations of currency wars. The financial markets, as usual, are discounting future developments – leading to moves such as the more than 20% appreciation in the U.S. dollar since mid-2014. Just as the markets are debating the onset and pace of U.S. Federal Reserve tightening moves for 2015, the Bank of Japan is rapidly expanding its balance sheet and the ECB is preparing to inaugurate quantitative easing. How will the diverging paths of these major central banks, and the impact those diverging paths have on currencies, affect the financial markets? Does the strengthening of the dollar portend trouble to come? From a strategic standpoint, we think that only fixed income investments should be hedged against currency risks. Tactically, we are positioned for the potential of further dollar strength by over-weighting U.S. equities and under-weighting developed market ex-U.S. equities and emerging market equities and debt.

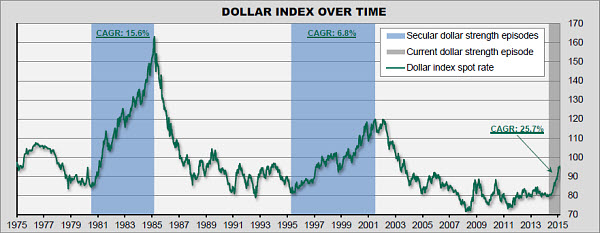

EXHIBIT 1: THE START OF SOMETHING BIG?

Sources: Northern Trust, Bloomberg; data through 2/27/2015. Dollar index is a weighted avg. of major currency FX rates vs. the dollar. CAGR = compound annual growth rate.

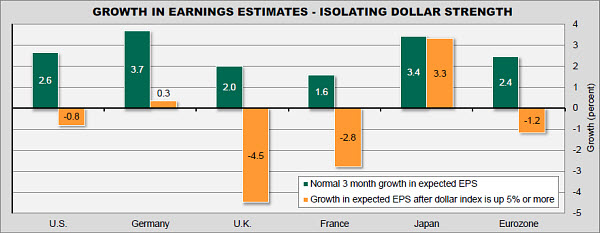

Trying to assess the impact of currency moves on economic growth and corporate earnings is a messy and imprecise affair. The Federal Reserve’s model for the U.S. economy includes estimates of the macroeconomic impact of changes in key variables such as interest rates, stock market wealth and oil prices. The FRB/U.S. model from the late 1990s estimated that a 10% reduction in the value of the dollar would have a 1.6% positive impact on growth after two years, while their updated model (November 2014) cuts the impact to 0.74%. Interestingly, the FRB/U.S. model now estimates a negligible overall impact on growth from a $10/barrel increase in oil prices. Looking at only the impact of the appreciating dollar and falling oil prices, the Fed’s model would estimate a negative impact on growth of 1.0% after two years – based on current price levels. One of the challenges in this forecasting process is that the price changes are not happening in a vacuum, as a rising dollar is most likely the result of the U.S. economy outperforming its peers. To understand the impact of a rising dollar on corporate profits, we studied changes in corporate earnings estimates since 2003 (the earliest point at which the data series in local currencies was available). Over the length of the study, earnings estimates actually fell in all markets after periods in which there was a three-month rise in the dollar of at least 5% (Exhibit 2).

EXHIBIT 2: STRONG DOLLAR HAS LED TO LOWER EPS – EVERYWHERE!

Sources: Northern Trust, MSCI, Bloomberg. Study uses monthly consensus 12-month forward earnings per share (EPS) data in local currency from 6/30/2003 to 2/27/2015. "Normal" measured using median. Dollar growth is over 3 months.

While other factors were undoubtedly at play, the trend of slower growth (Germany and Japan) as well as cuts in earnings estimates (U.S., U.K., France and the broader Eurozone) suggests that the dollar strength frequently was occurring at a time of weakness in their respective economies. The much better relative performance of Japan suggests that the export-related earnings offset the impact of softer domestic economic conditions. After the recent episode of dollar strength, Eurozone next-12-month earnings estimates (in euros) were 1.2% lower than they were three months ago, while Japanese estimates (in yen) were 5.4% higher. This data tells us Japanese companies are benefitting more than European ones from currency depreciation – which is logical given the earlier start of Japanese quantitative easing (QE). However, it also raises the sensitivity of forward European earnings growth to improving economic growth. The benefits from improving exports are clearer than domestic demand growth tied to improved credit creation. As shown in the Appendix, during the two major dollar rallies since 1980, U.S. earnings have actually increased at a 2.9% and 8.0% annual rate – reflecting the relative strength of the U.S. economy during these periods.

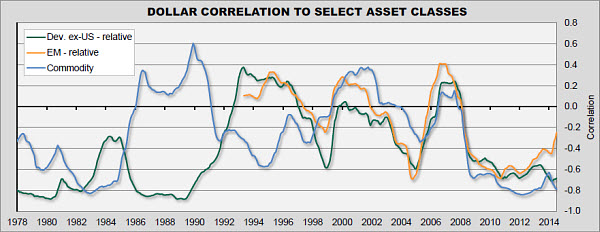

The impact of dollar movements on different asset classes is unstable over time, with correlations that transition from positive to negative. Exhibit 3 shows how non-U.S. equity returns have been both negatively and positively correlated to movements in the dollar. There appears to be a regime shift with respect to the correlation of non-U.S. relative returns to the dollar starting in the 1990s – likely a result of increased globalization, wherein revenues of non-U.S. firms expanded outside the borders of their home countries. Commodity prices have also had a non-constant relationship to the dollar. Commodity prices were positively correlated to the dollar in the late 1980s, and spent most of the 1990s and the 2000s (up to the 2008 financial crisis) with little relationship to the dollar. Post-financial crisis, both non-U.S. equity returns and commodity returns have shown a negative correlation to dollar movements.

EXHIBIT 3: UNSTABLE RELATIONSHIPS

Sources: Northern Trust, Bloomberg. Data in dollars through 2/27/2015. Dev. ex-U.S. and emerging market returns are relative to U.S. equities, using MSCI World ex-U.S. MSCI Emerging Markets and MSCI U.S. Indexes.

Over the near to intermediate-term, we could expect these negative correlations to persist, more so for commodities than for equities. With commodities, the upward move in the value of the dollar puts downward pressure on the commodity values to compensate. With equities, the downward move in the local currency should have some beneficial impact on growth (through improved exports), improving the corporate profit outlook and offsetting some of the negative currency hit.

There has been significant issuance of dollar-denominated debt by emerging market companies in recent years (a recent estimate from the Bank of International Settlements cite roughly $2 trillion of outstanding debt and up to $3 trillion in bank loans).1 Continued dollar strength represents a considerable risk to these corporate borrowers, where their currencies have correspondingly depreciated as their debt service burden grows commensurately. Chinese issuers are somewhat less at risk due to the effective targeting of the renminbi to the U.S. dollar (the renminbi has depreciated by just 2.3% over the last year, as of 3/5/2015). At the other end of the spectrum would be issuers from countries such as Russia, where the ruble has depreciated by 60% over the same time frame. We expect this increasing debt burden risk to weigh on emerging market company performance over the next year, affecting the performance of both emerging market stocks and bonds.

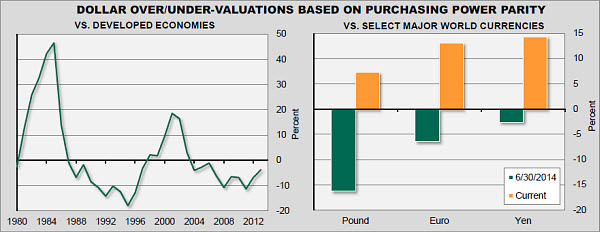

While we have reviewed the impact of dollar moves on earnings and certain asset classes, investors struggle with trying to assess a fundamental outlook for currency values. We can understand the valuation of currencies by comparing what goods and services cost in various currencies (purchasing power parity). Comparing the value of an economy’s output in real terms versus the value of output in U.S. dollars gives us insight into whether the dollar is over- or undervalued. In 2013, using the most recent data from the International Monetary Fund (IMF), the dollar was slightly undervalued when appraised through a purchasing power parity lens. The fact that the same goods/services bought outside the United States cost 3.7% more than when bought inside the United States implied that the dollar was undervalued. Looking at more specific data points, but still using a purchasing power parity construct, the dollar was undervalued versus other major currencies prior to the recent dollar appreciation (June 30, 2014) by 16%, 7% and 3% versus the pound, euro and yen respectively. However, after the recent move upward, the dollar is now overvalued by 7%, 13% and 14% respectively. Purchasing power parity is thought to occur in the long-term, but it can remain in disequilibrium for long periods due to trade restrictions and the immobility of some services (a haircut that is 10% cheaper in London is not going to motivate much travel). As shown in Exhibit 4, the dollar remained significantly overvalued in the 1980s and early 2000s for multi-year periods.

EXHIBIT 4: AMERICANS IN PARIS … AND TOKYO AND LONDON

Sources: Northern Trust, IMF, OECD, Bloomberg. Left panel: Data through 2013. Right panel: Current as of 2/27/2015.

A parity construct that tends to sit closer to equilibrium in the near-term is interest rate parity. Interest rate parity theorizes that, if the risk-free rate of interest differs within two currencies, the exchange rate between those two currencies should adjust to make up the difference. For instance, the U.S. three-month Treasury currently provides a 0.05% rate of interest. While extremely low (almost zero), it looks great compared with the -0.27% offered by three-month German bunds. Assuming that both vehicles are indeed risk-free, interest rate parity would predict that the U.S. dollar should depreciate by 0.32% versus the euro over the next three months. Otherwise, an investor could make money by borrowing in euro and putting that money in U.S. dollars. However, this theory does not work well in practice. Financial market frictions take away some of the arbitrage opportunities. Also, there are multiple examples of the carry trade phenomenon, wherein currencies with higher interest rates actually continue to show appreciation as investors pile in. The concluding point is fairly simple: because of real world frictions and investor sentiment, theory does not translate well into practice and currency moves can be quite volatile and unpredictable. What does all this mean for portfolio construction? On a tactical basis (12-month time horizon), we do recommend U.S.-dollar investors reduce risks associated with the rising dollar. We have primarily expressed this through recommended underweights to non-dollar equity assets such as developed ex-U.S. and emerging market equities. Additionally, increased currency risk and rising carrying costs leads us to underweight emerging market bonds. Finally, we have been skeptical over a bounce back in natural resources from the recent weakness – based on the potential for further U.S. dollar strength as well as an expectation of moderate global economic growth.

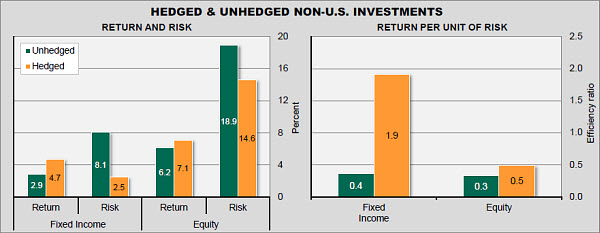

EXHIBIT 5: LOTS OF REASON TO HEDGE YOUR BONDS

Sources: Northern Trust, Bloomberg; last 10 yrs. of monthly returns through 2/27/2015. Fixed income: Barclays Aggregate Global ex USD Index (hedged & unhedged); Equities: MSCI ACWI ex-U.S. gross total return Index (USD & local).

On a strategic basis, we think fixed income portfolios benefit from currency hedging. The increased volatility of the Barclays Aggregate Global ex-USD Index on an unhedged basis, at 8.1% risk compared with 2.5% on a hedged basis, is unacceptably high for the risk control part of a portfolio. This can be demonstrated by looking at the return per unit of risk, shown on the right side of Exhibit 5, which shows significant deterioration in the unhedged fixed income portfolio. With respect to equity exposures, we believe the long-dated nature of these investments diminishes the necessity of currency hedging. While there was some improvement in efficiency over the study period, its benefit is vastly overshadowed by the benefits of hedging the fixed income portfolio.

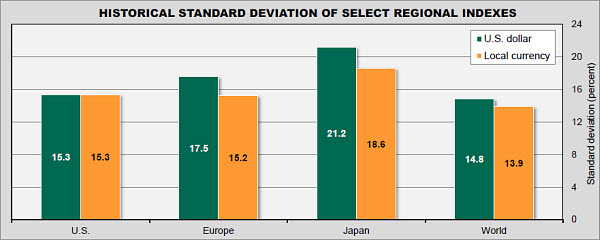

Finally, we would like to address a topic that is front-and-center in many year-end portfolio reviews (especially for U.S.-based investors). The significant recent outperformance of U.S. equities (including the 13.7% return in 2014 – using the S&P 500 as proxy – compared with U.S. dollar returns of -4.5% for EAFE and -1.8% for Emerging Markets, using MSCI indexes as proxy) has raised questions about the value of global diversification. From a diversification standpoint, the overall risk of an equity portfolio is reduced through globalization. In local currency terms, both a U.S. and European concentrated portfolio have risk just north of 15%, while a Japanese-only portfolio has risk of 18.6%. All of these investors would benefit from reduced risk by moving to a world equity portfolio, where risk is reduced to 13.9%.

EXHIBIT 6: LESS RISK IN THE WORLD

Sources: Northern Trust, Bloomberg. Study uses MSCI indexes and gross total return data from 12/31/1969 – 2/28/2015.

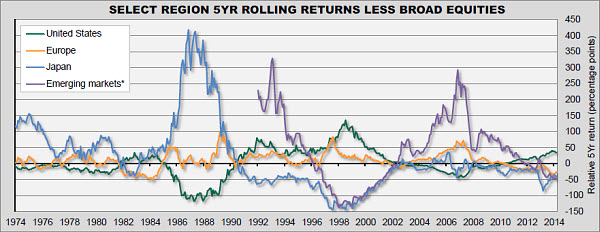

Moving away from diversification to look directly at relative performance, Exhibit 7 shows the performance of the major developed regions versus the MSCI World Index since 1974 and emerging markets since 1992. To smooth out performance, we show the trailing five-year relative performance of each region. There are periods of relatively long-outperformance at the regional level: with Japan and Europe outperforming the United States during the 1970s and 1980s; U.S. and European equities trouncing Japanese shares in the 1990s; and emerging markets outperforming in the early 1990s and mid-2000s. However, if you bought the best-performing region at the end of any of the eight five-year periods studied, that region repeated as the best-performer only three times. Further, while many are worried about Europe, history shows that Europe outperforms 88% of the time over the next five years after underperforming over the previous five years.

EXHIBIT 7: IN AND OUT OF FAVOR

Sources: Northern Trust, Bloomberg. Data through 2/27/2015. Broad equities = MSCI World Index (*ACWI for EM, available since 1992). Regional equities are proxied by MSCI United States, Japan and Europe Indexes. Returns are in USD.

CONCLUSION

The divergence in global monetary policy that has led to sharp currency swings over the last eight months looks set to continue as both Japan and Europe are committed to improving economic growth and avoiding deflation. The task for the monetary authorities is hardened by the fact that monetary policy is, by itself, insufficient to improve their economic dynamics. This only increases the likely duration of the easy money policies, leading to further currency risks. While making bold currency forecasts is not for the faint of heart, we do believe that continued dollar strength over the next year is the most likely outcome – and that portfolios should be tilted toward U.S.-dollar assets. We have felt that the divergent growth between the United States and other developed markets was unlikely to persist throughout 2015 – and that economies such as Europe would see some pickup in growth and converge toward the United States. This positive convergence remains our most likely outcome, which could limit the eventual magnitude of the currency moves. While European growth data has improved of late, the U.S. data has been more mixed – with the strong February jobs report being a recent positive outlier. The only real certainty seems to be increased volatility in 2015 as the market weighs the incoming economic data and wrestles with the implications for monetary policy.

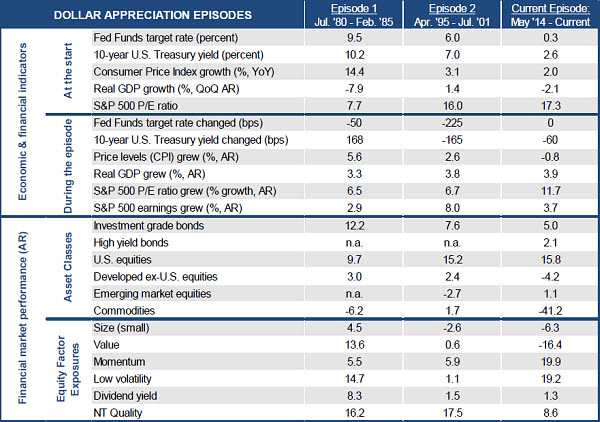

APPEDIX: ECONOMIC & FINANCIAL DETAILS OF THE EPISODES

Sources: Northern Trust, Northern Trust Quantitative Research, Bloomberg. AR = annual rate. Current as of 2/27/2015.

ENDNOTE(S)

1Bank for International Settlements Quarterly Review, 7 December 2014

(c) Northern Trust