Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

Never let an airplane take you somewhere

your brain didn't get to five minutes earlier

Old Pilot Sayings

Global Carry, Yen and Dollar are irrefragable drivers of Global Macro. As we explain equities and bonds are just derivatives of these factors. We expose how the big picture asset dynamics worked since the GFC, brief on what happened over the last year and conclude with comments on dollar blowout over the past week.

Over the last week you should have figured out whether you have long (made money) or short (lost money) dollar exposure in your portfolio as dollar blowout was pretty much the major and the only driver of assets over the last week aside from modest Yen weakening.

We bragged about Global Carry extensively recently[1][2][3][4][5] but let us revisit the framework from scratch:

- Let us take a basket of the major macro assets (US Equities (SPX, NQ, DJ), US Bonds (2,5,10,20), Dollar Index, Euro, Japanese Yen, Nikkei)

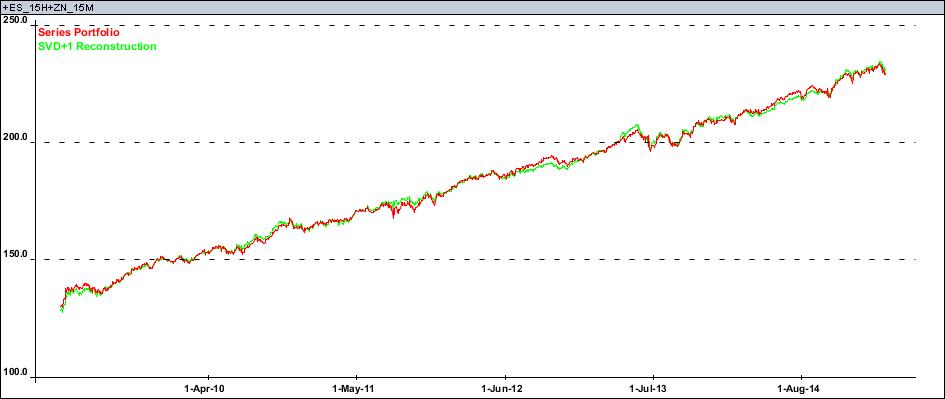

- Turns out since the end of the Global Financial Crisis (Mar-2009, six years ago) almost all movements in these assets are explained by three statistical factors which can be thought of as:

- – Global Carry (a.k.a. Risk Parity)

- – Yen Factor

- – Dollar Factor

- It implies for example that there is no need in “specific factors” explaining for instance US Equities or US Bonds (including term structure)

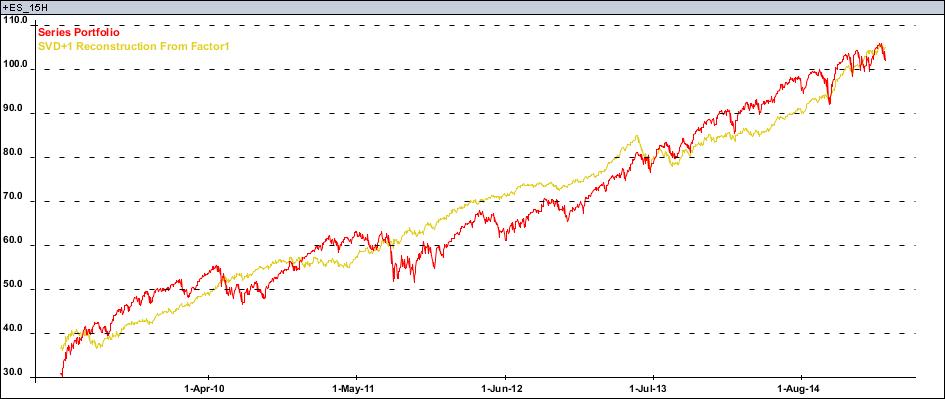

- SPX = long global carry + short yen + short dollar

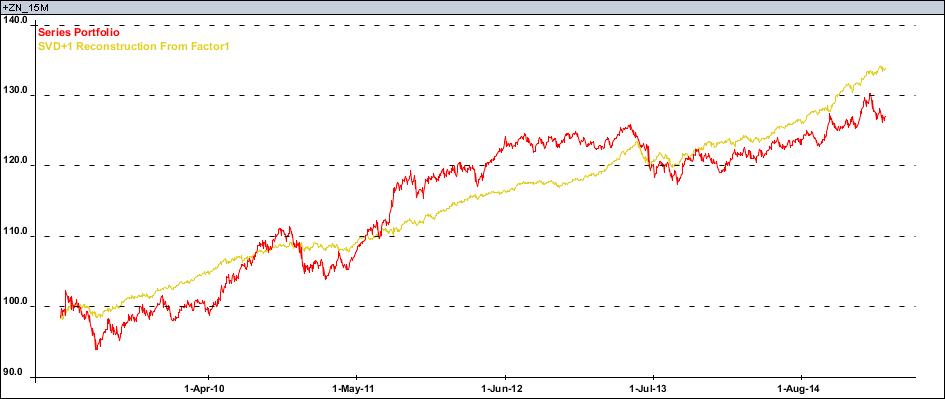

- US 10y Note = long global carry + long yen

- The SPX and US 10y Note are anti-correlated because of the opposite Yen Factor exposure which is effectively the one producing Risk On/Risk Off behavior. But this anti-correlation is only at play when the Yen Factor is dominating on the day.

- On days when carry is a major driver SPX and US 10y Note will co-move while Dollar Factor movement will affect equities mostly (in negative way, which makes sense from the companies earning perspective)

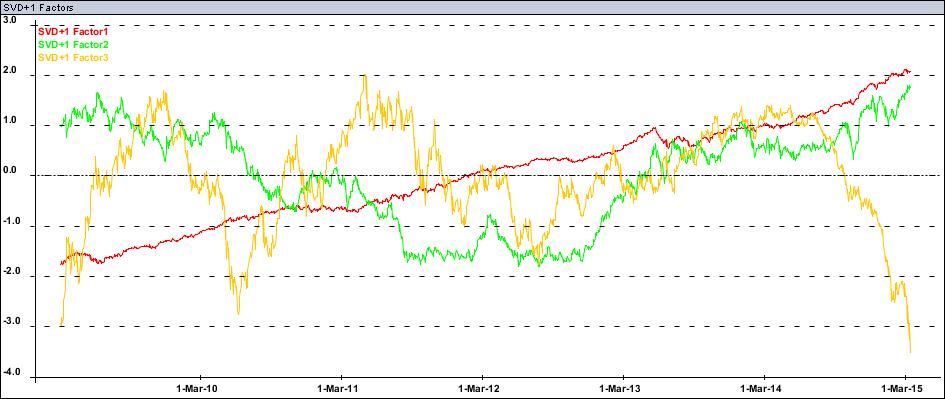

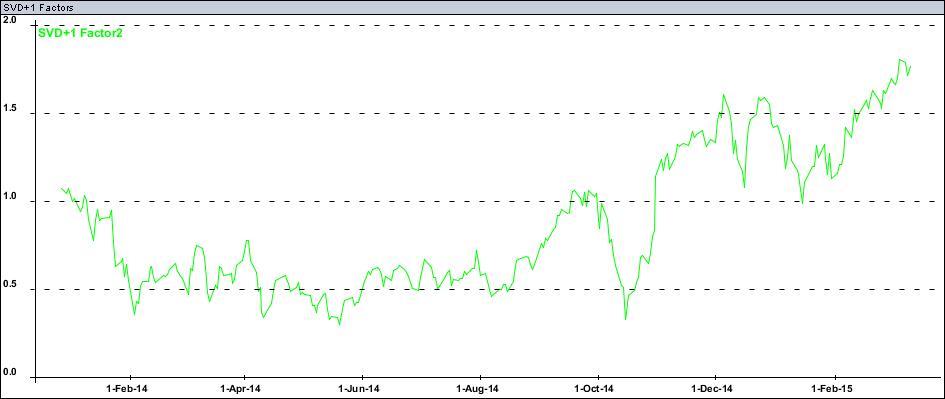

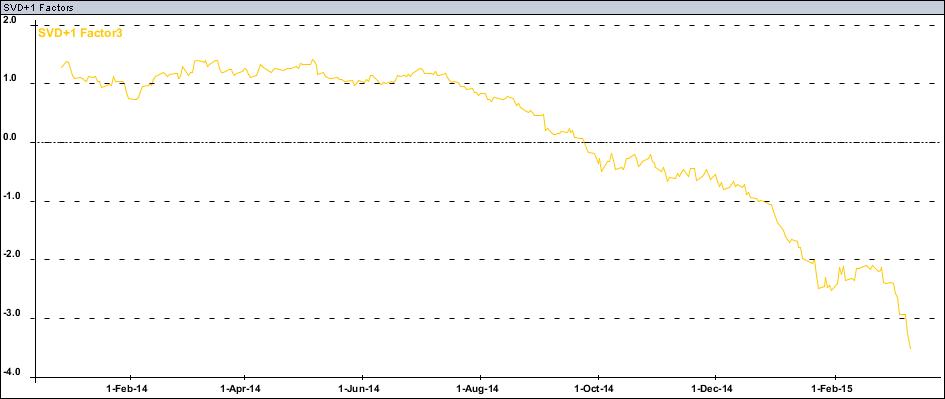

So this is how these three factors performed over the last six years (pay no attention to the scaling of Y-axis):

- Global Carry (Factor1) is basically Equities + Bonds in equal risk i.e. Risk Parity. Noticeable gyrations in spring/summer 2013 are obviously the Taper Tantrum.

- Yen Factor (Factors2 with minus sign) is the Yen adjusted for Global Carry Factor and also is responsible for Risk On/Off i.e. Volatility (VIX). Also not the periods of stability or rather manipulation so to speak in the middle of the period.

- Dollar Factor (Factor3 with minus sign) is pretty much the Dollar index and has been obviously the major global assets driver since July 2014. The recent reversal it appears was just a preparation for further dollar strength. The six year resistance level was broken with a vengeance. Yes, you were right Raoul Pal.

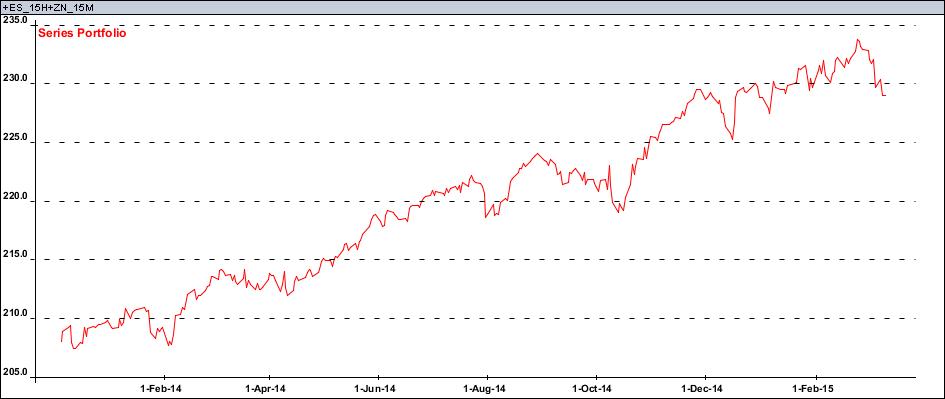

The Global Carry can be proxied by (surprise! surprise!) SPX + US 10y Note portfolio:

I would not get into the details of how one could have made a fortune by getting into this trivial (while still Sharpe 1.5) portfolio six years ago in his IRA and saw this thing securely producing 20 times the money without essential drawdowns as this thing doubled (even without compounding) and the margin on SPX E-mini and 10Y Note futures has never exceeded 5% so leverage 10 would have been acceptable for a high roller.

Just to demonstrate how the Yen Factor cancellation between SPX and US 10y Note worked let me show SPX vs Global Carry

As well as US 10y Note vs Global Carry

Neither of the above two is spectacular but their sum makes magic. Indeed as we explained before Global Carry is nothing else but pretty much proper Risk Parity portfolio and is the only driver behind Risk Parity commercially available portfolios returns.

Of course Global Carry goes well beyond dollars and cents, and one way or another is pretty much the driver behind the majority of international macro assets. As spectacular as it is we would not get into much of it here though.

Recent SPX + 10y Note proxy weakness seen above and illustrated below, which brings it back to the start of the year level, is pretty much explained by the short Dollar exposure coming from the SPX leg.

The commercial Risk Parity providers are bleeding much, I bet.

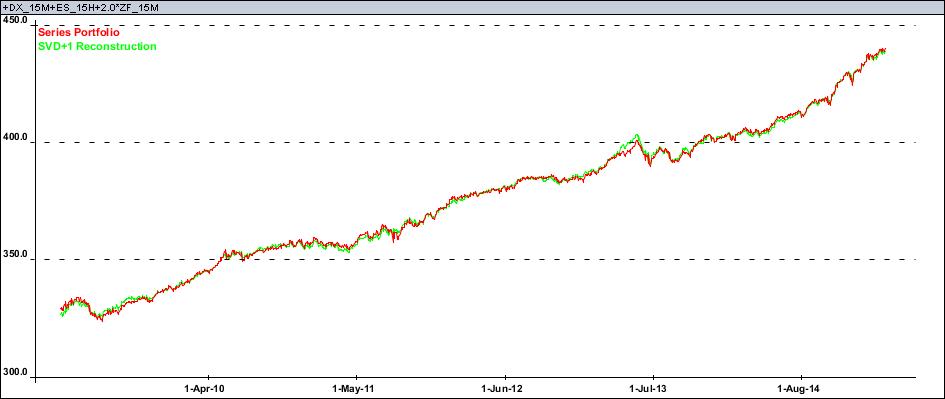

There is a modernized proxy for Global Carry which has very slight positive dollar exposure and uses shorter duration 5y Notes. It is comprised of SPX E-mini, Dollar Index and a couple of 5y note futures.

Rocking and Rolling is its second name:

We are now all clear for the recent performance of Factors charts:

Global Carry:

Yen Factor (opposite sign):

Dollar Factor (opposite sign):

As you can see, the name of the game over the last week (and since July 2014 for that matter) is freaking long the Dollar Factor. A bit short Yen too, while Global Carry has pretty much gone nowhere since the end of January.

We will see what is up next for us on the table, meanwhile please remember this Rule Number One we pilots have:

No matter what else happens, fly the airplane.

[1] “Global Carry a.k.a. Risk Parity”, Dynamika Commentary, 16-Oct-2014

[2] “Global Carry gone parabolic?”, Dynamika Commentary, 29-Nov-2014

[3] “Global Carry is correcting”, Dynamika Commentary, 10-Dec-2014

[4] “Global Carry Rock ‘n’ Roll”, Dynamika Commentary, 3-Feb-2015

[5] “Global Carry Game Over?”, Dynamika Commentary, 17-Feb-2015