The current bull market, one of the most powerful in the S&P 500’s history, celebrates its sixth birthday today, March 9, 2015. The S&P 500 has more than tripled since the financial crisis closing low on March 9, 2009 (the index is up 206% since then), achieving a cumulative return, including dividends, of 244% (22.8% annualized). Since World War II, just three other bull markets have reached their sixth birthday, and only one (1982 – 1987) produced bigger gains ahead of its sixth birthday, as shown in Figure 1.

IS THIS BULL SET TO END?

We do not think this bull market is about to end just because it’s six years old. Bull markets do not die of old age, they die of excesses, and we do not see evidence today that economic excesses are emerging. There is still slack in labor markets despite healthy job growth in recent months. The credit markets reflect rational behavior. We see few signs of overbuilding in the commercial and residential real estate markets. Inflation (with or without the effects of depressed energy prices) remains low, which has enabled the Federal Reserve (Fed) to remain accommodative. The accommodative Fed provides further evidence of the absence of the types of excesses that have marked prior stock market peaks.

Historically, the timing of Fed rate hikes can provide some insight into when recessions might be coming (though the Fed’s track record is far from perfect). The Fed typically reacts to built-up excesses with multiple rate hikes, contributing to the start of recessions. Bear markets then begin as market participants anticipate those economic downturns. Most of the post-WWII bull markets, including the internet and housing bubbles in 2000 and 2007, came after a period of multiple Fed interest rate hikes. The slow economic recovery has delayed the formation of excesses and the start of the Fed’s rate hike campaign. Rate hikes will come — perhaps as early as this summer — but until we see more evidence that economic growth and monetary stimulus from the Fed are creating worrisome inflation, we expect this bull market will live on.Looking for a Warning Signal

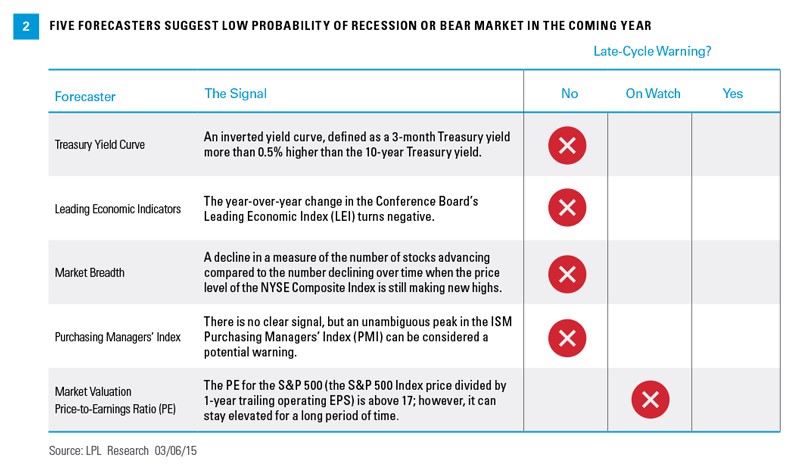

To help us possibly get some warning on when a market downturn may be coming, we have identified several leading indicators (which we have dubbed the “Five Forecasters,” as discussed in our Outlook 2015: In Transit publication) that have been pretty effective predictors of impending market downturns and recessions when combined. These indicators give us more confidence in our positive stock market outlook for 2015 [Figure 2].

WHAT ABOUT VALUATIONS?

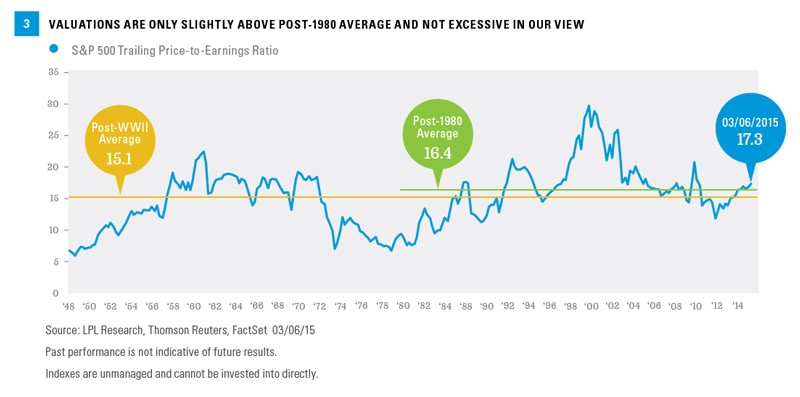

The one “Five Forecaster” that has sent off a potential warning signal is valuations. The trailing price-to-earnings ratio (PE), the series that goes back the furthest, stands at 17.5 (as of March 6, 2015, based on Thomson Reuters earnings data). That is above the long-term average dating back to World War II of 15.1, but not much above the average since 1980 of 16.4 [Figure 3].

While valuations may be higher, we do not think it means an impending end to this bull market for several reasons:

- Valuations are not a reliable short-term predictor. Although above-average valuations may signal muted longer term returns, valuations have proven to be a poor predictor of shorter-term stock market performance. Prior bull markets have shown that earnings gains can lift stocks for quite a while even after valuations exceed long-term averages and PE expansion is halted.

- Stocks may be preferable to bonds. Low interest rates have made bonds a less attractive alternative to stocks, making stock valuations more attractive. Stocks may be slightly overvalued, but bonds are much more stretched, in our view.

- Earnings gains are possibly set to continue. We see continued, though modest, earnings gains in 2015, as the benefits of lower energy prices for consumers and businesses help offset the sharp downturn in energy sector profits. Despite sharp downward revisions to energy estimates, consensus still reflects S&P 500 earnings gains in 2015. The Institute for Supply Management (ISM) Manufacturing Index, our favorite leading earnings indicator, is still signaling positive earnings growth despite dipping in recent months. Corporate earnings are benefiting from share buybacks (which lower share counts, the denominator in the earnings per share calculation), as well as low borrowing costs and limited wage pressures, which are all helping to support profit margins and continued earnings growth.

- Low inflation increases the value of future corporate earnings, supporting stock valuations. Though certainly tied to interest rates and the Fed, and a driver of bond performance, inflation by itself is a drag on the value of cash flows and dividends that corporations generate; therefore, it is a key driver of stock market valuations.

ARE WE DUE FOR A CORRECTION?

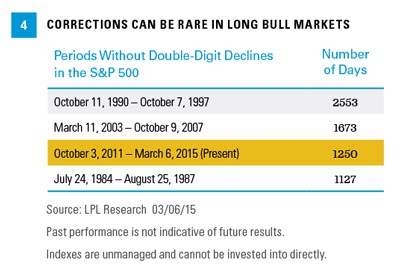

After “Are stocks too expensive?” perhaps the second most common question we have been getting during the latest leg up of this bull market is, “Are we due for a correction?” We define a correction as a drop in the S&P 500 of 10 – 20% (a 20% or more decline is a bear market). It has been a long time since the S&P 500 dropped 10% or more — 1,250 days to be exact — but we only have to go back to the past two decades to find longer periods. During the 1990s bull market, the S&P 500 went 2,553 days, or just shy of seven years, without a correction, and during the 2000s bull market, the S&P 500 went 1,673 days, or about 4.5 years, without dropping more than 10% at any point[Figure 4]. The age of this bull market could mean volatility may increase in the coming year, and 10% corrections are fairly common, even in bull markets; but the length of this period of relative calm is not without precedent, so we would caution against moving to a defensive stance in anticipation of a correction.

CONCLUSION

Bull markets die of excesses, not old age. We do not see the types of excesses in the U.S. economy today that suggest a bear market decline is forthcoming. The Fed, which has historically raised interest rates multiple times before bull markets end, has not yet begun to hike interest rates during this cycle. And some of our favorite leading indicators suggest the economic expansion and bull market may continue through 2015. Although valuations are above average and a correction may come should the aging bull market become more volatile, we think the chances are good that at this time next year, we will be wishing this bull market a happy seventh birthday.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

All indexes are unmanaged and cannot be invested into directly.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The Leading Economic Index is a monthly publication from the Conference Board that attempts to predict future movements in the economy based on a composite of 10 economic indicators whose changes tend to precede changes in the overall economy.

The Purchasing Managers’ Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI is based on five major indicators: new orders, inventory levels, production, supplier deliveries, and the employment environment.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

The trailing PE is the sum of a company’s price-to-earnings, calculated by taking the current stock price and dividing it by the trailing earnings per share for the past 12 months. This measure differs from forward PE, which uses earnings estimates for the next four quarters.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. EPS is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5009 0315 | Tracking #1-361611 (Exp. 03/16)

(c) LPL Financial