Investing is a funny business. It is usually wise to invest the opposite of how the market feels to you. Six years ago stocks had fallen by 50%, the financial institutions that underlie our global economy were buckling, and the economy was in shambles. Investors were running from the stock market in droves. But because prices and expectations were low and because all the major central banks flooded the world with liquidity it was actually a great time to invest. As we linger today near all-time highs on virtually every global stock market it certainly feels like a good time to invest. Perhaps that feeling is a danger sign.

Nearly half of the rise in the S&P 500 since 2012 has been explained by an expansion in the Price to Earnings multiple which has resulted in high valuations for US stocks. In the second half of 2014 we became more conservative in our portfolios as valuations rose, commodity markets and sovereign bond yield collapsed, and market volatility picked up. These conditions are all signs that after six strong years of returns the stock market has become more fragile. Since our move earnings expectations for the S&P 500 have declined dramatically reinforcing our conviction. According to Zacks, excluding the energy sector, first quarter 2015 earnings growth for the S&P 500 is expected to be 4.3%, down from 12.3% in early October. If you include the energy sector, profits are expected to decline by -3.6%. These are huge downward revisions but yet here we are at all-time highs. Obviously the market is looking over the valley to a recovery later this year. However, the bond market is screaming a serious slowdown is underway globally, so obviously something has to give in the not too distance future.

Although the risk profile is elevated for stocks, investors should not abandon the asset class completely. While more volatile, long-term returns from equities should still be positive and will likely be greater than most alternatives. Many of our holding have rock solid balance sheets and have a dividend yield much higher than the 10-year Treasury. These characteristics should support prices even in the face of a global slowdown.

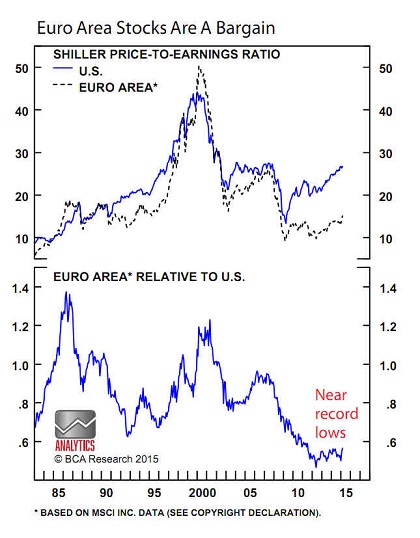

International markets are looking more attractive. Valuations are more favorable, financial conditions are easing and growth expectations have room to surprise on the upside. We particularly like Eurozone and Japanese stocks, both of which have significantly outperformed the S&P 500 so far this year, a surprise to most investors and a big change from 2014. Weak currencies, lower oil prices, accommodating central banks, attractive valuations (see chart), and low expectations suggest the turnaround in performance has far to go.

Please contact us if you have any questions.

Jim Tillar, CFA, Steve Wenstrup

(c) TW Advisors