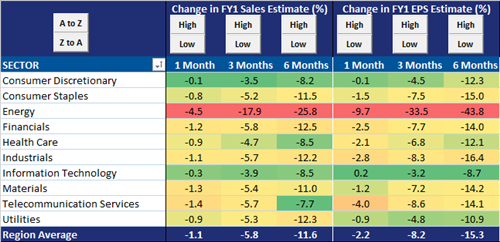

We have commented quite a bit on the dismal revisions to sales and earnings estimates (see here, here, and here for just a few examples). As we have noted, European stocks have excelled in the downgrade department, led by the Energy sector:

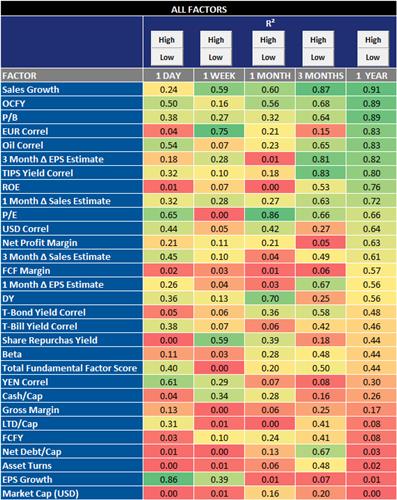

Keeping in mind that changes in estimates have remained in the top 10 important factors driving performance for MSCI Europe over the past year...

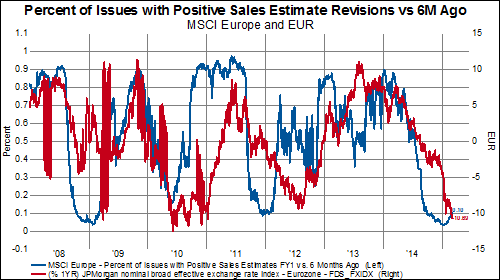

...as well as the close relationship between those estimates and movements in the EUR...

...it is a bit disconcerting to watch as the EURUSD exchange rate flirts with a decisive breakdown below long-term support:

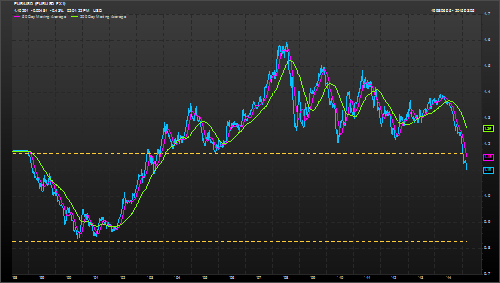

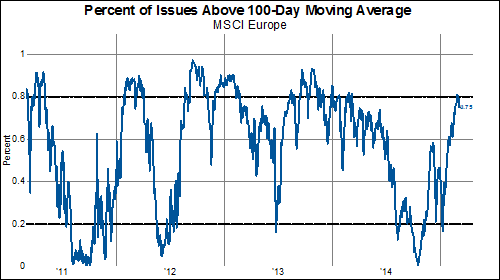

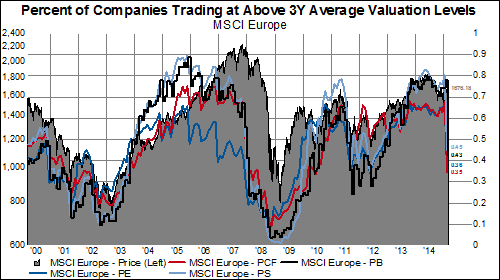

Furthermore, investors seem to have taken notice of the fairly extended nature of the market, as evidenced by a sharp drop (to ~40% from ~70% a month prior) in the percentage of companies trading at a premium to longer-term valuation metrics.

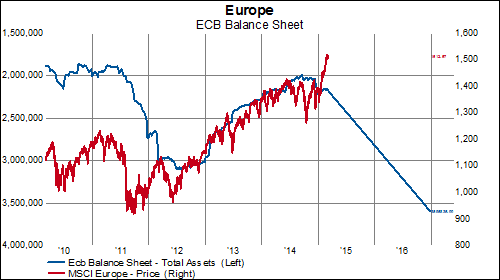

All of this would seem to lend support to the relationship we showed between ECB asset purchases and stock performance a while back-- namely that MSCI Europe looks vulnerable to a 35% decline from current levels:

(c) GaveKal Capital