Running in Place

- Volatility returning

- No change in our “lower for longer” interest rate forecast

- ECB preparing to go on bond buying spree

- 2016 state budgets getting special attention

A much colder than normal winter throughout the United States has impacted daily activities. Folks are remaining indoors and waiting for the March thaw. Not only are there fewer pedestrians, but runners are a rare sight. The logical inference is that many dedicated exercisers have retreated to the warmth of their basements or local health clubs for exercise, and are instead logging miles on stationary treadmills.

“Running in place” is a metaphor that encapsulates what has transpired in the financial markets thus far in 2015. Just two months old, the year is unfolding as we expected. Price volatility has accelerated in equity, bond and commodity markets – a stark contrast to 2014. In January, stocks started off the year on the wrong foot, but sharply rebounded in February. Many global equity indices even reached record highs in February. Bond markets have been the mirror image of stocks: yields dropped in January and reversed course last month. Commodities have garnered more attention, and price instability, due primarily to the plunging cost of oil and its derivative products.

Two-thirds of the way through the first quarter, bond yields have displayed little net change despite a frenetic two-month ride. In the municipal marketplace yields have run a significant distance in both directions, but presently rest pretty much where they started and perhaps leave the mistaken impression that prices have not shifted much in eight weeks. The Barclays Municipal Bond Index has moved 0.72% higher year-to-date (+1.77% gain in January followed by February’s -1.03% decline).

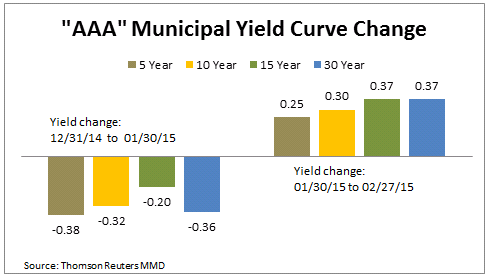

Tax-exempt inter-month trading volatility is shown in the graph below. Selected points along the “AAA” municipal yield curve highlight the monthly yield moves. First, note the 13 basis point net decline in the short maturity (5-year) segment of the curve. This is due in part to the annual calendar “roll-down” effect as well as to global bond markets’ reactions to perceived dovishness by the Fed and the anticipation of large scale bond purchases by the European Central bank (ECB) beginning this month. The intermediate (10-year) and long-term (30-year) maturities have not registered a meaningful yield shift in 2015 despite dramatic monthly fluctuations. SMC’s preferred maturity segment (15-year) has cheapened by 17 basis points.

The “will they or won’t they” debate endures. In her semi-annual testimony before Congress last week, Fed Chairwoman Janet Yellen reminded Congressional leaders that the FOMC will maintain its slow-motion retreat from over eight years of monetary stimulus. The markets interpreted her remarks to mean short-term rates will continue to remain near zero for a considerably longer period of time than many were anticipating. We maintain the opinion that the Fed will err on the side of being too cautious, and rates will remain low, probably through year-end. The still deteriorating global economic picture will preclude any near-term move. The U.S. economy is not immune from global influences. A strong dollar means we are importing deflation from the rest of the world: imports are cheaper and exports more expensive. We anticipate seeing the effect in first quarter corporate earnings of multinational companies that are heavily reliant on overseas sales.

The ECB embarks on its much-anticipated bond purchasing program this month to help revive the Eurozone economy. The ECB’s version of quantitative easing will entail the buying of Euro 60 billion ($68 billion) per month of sovereign government debt securities through September 2016. However, there is a problem, as government bonds are in short supply and the shortage is expected to get worse as demand from the Central Bank accelerates. Purchases will be based on each member country’s share of the EU population. Germany, the largest member, is already posting negative bond yields due to the supply imbalance. The ECB is planning on purchasing 26 times more German debt than the amount by which the sovereign Bund market is expected to grow between March 2015 and September 2016. Likely, U.S. Treasury bonds will continue to benefit, supported by their relative yield attractiveness and currency strength.

As spring approaches the “state of the states” gets more attention. Most governors have recently presented their proposed 2016 budgets for the fiscal year beginning July 1. According to the National Association of State Budget Officers, ten states will be proposing tax increases, including some by Republican-led governors. Mounting payments for underfunded public pension and healthcare programs is the most serious issue due to both underpayments in past years and required more conservative future funding assumptions. Illinois, the lowest rated state (“A-” by S&P), is confronted by $6.4 billion of unpaid bills, the worst funded state pension system, and union unrest. Fortunately, Illinois Governor Bruce Rauner is not considering a run for the GOP 2016 Presidential nomination.

However, there are three prominent Republican governors who have both an eye on the presidency and considerable budget challenges at home. Analysts are questioning whether the soundness of their respective state fiscal plans is being influenced by their political ambitions or what they truly believe is in the best interest of their constituencies. Louisiana’s Bobby Jindal has to respond to falling tax revenues due to plunging oil profits. New Jersey has suffered eight credit downgrades since Chris Christie took office five years ago. His proposed $34 billion budget contains virtually nothing for needed infrastructure spending or refilling the nearly-depleted transportation trust fund. His proposed aggressive restructuring plan of the state’s underfunded pension healthcare and pension system, including a constitutional amendment, will be difficult to enact. Wisconsin’s Scott Walker, already facing a $233 million revenue shortfall in the current year, is proposing an equivalent cut (13%) from the state’s university budget. While the municipal market appears to be running in place, these chieftains are likely maneuvering to get a good start out of the blocks.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary is neither an offer to sell nor a solicitation of an offer to purchase securities, any other investments or any other product sponsored or advised by SMC FIM, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. Such an offer or solicitation may be made only by the relevant documents for the relevant investment vehicle and/or investment program. This commentary is not, and may not be used as, a recommendation of any security, investment program or vehicle. There is no assurance that any securities discussed herein will remain in a client’s account at the time you receive this commentary or that securities sold have not been repurchased. The securities discussed do not represent the client’s entire portfolio and in the aggregate may represent only a small percentage of the client’s portfolio holdings. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2015 Spring Mountain Capital, LP. All rights reserved.