By: Heather Rupp, CFA, Director of Research for Peritus Asset Management, the sub-advisory firm of the AdvisorShares Peritus High Yield ETF (HYLD)

Together the high yield bond and floating rate bank loan market total over $3 trillion.1 This has evolved into a significant, and growing asset class. With high yield bonds and loans now representing about 30% of corporate credit2, this market deserves not only our attention, but we also feel is ripe with opportunity for investors.

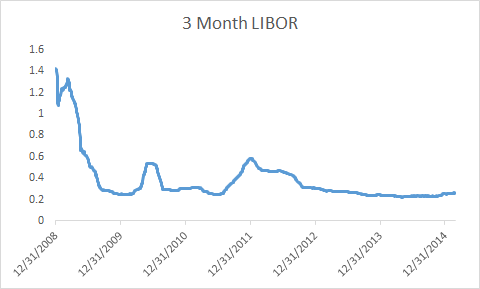

We recently have written on the current opportunity in the high yield bond market (see our commentaries, “The Opportunity in Volatility” and “Alpha Generation for Active Managers”), but now let’s turn our attention to the opportunity set we see in floating rate bank loans. Many often see this market as a duration play—a way to invest if you think rates will rise. Yes, loans benefit from the “floating” rate via the generally quarterly LIBOR-based interest rate reset. However, investors need to keep in mind that a large portion of these loans have LIBOR floors, often ranging from 1-1.5%. This means that we would need to see LIBOR move 0.75-1.25% off of current levels to move the rate realized by the investor. As a frame of reference, we’ve barely seen 3 month LIBOR move over the last few years.3

So not only do you need to see a pretty significant move in interest rates to surpass that floor, and we don’t expect the Fed to take aggressive action by rapidly and sizably raising rates, but you would need to also see interest rate moves here at home impact LIBOR (the London Interbank Offered Rate), despite the quantitative easing we are seeing elsewhere in the world.

While there is certainly a duration benefit to a portfolio by investing in floating rate loans, we believe that investors embracing the loan market as a pure interest rate/duration play may well be disappointed. The more significant value that we see in this market is the expansive number of issuers and issues this market encompasses, allowing investors’ access to companies that may not issue high yield bonds and/or to secured securities in a company’s capital structure, expanding the opportunity set for yield-seeking investors.

As we ended 2013 and entered 2014, the clear consensus was that interest rates were rising and with that, investors poured money into the loan asset class. From mid-2012 to April of 2014 we saw a record 95 total weeks of consecutive mutual and exchange traded fund inflows into the floating rate loan asset class, totaling $81 billion.4 During that period, loan prices ran up and yields became compressed. As that higher rate expectation clearly didn’t play out as 2014 progressed, we saw a sharp reversal in the interest in the loan market. Since the spring of 2014 through mid-February we saw 42 of the last 44 weeks post fund outflows, for a total of $35 billion over this period.5

As we have seen investors leave this asset class, we have seen loan prices fall and yields increase. For instance we began 2014 with 84% of loans trading at a premium to par ($100). Yet we entered 2015 with only 19% of loans at a premium.6 We have seen a clear spread and yield widening in this asset class, which we view as an attractive opportunity for active investors that can look for those loans that offer the best value relative to risk. Keep in mind that loans are secured securities that are at the top of a company’s capital structure, ahead of unsecured bonds and equities, adding another potential layer of risk reduction for investors.

With what we see as attractive yields and discounts creating the potential for capital gains in many cases, today we see compelling value in both the high yield bond and floating rate bank loan markets for investors who have the flexibility to not only invest in both markets but also look for what they see as the best value within each market. Again, the high yield bond and floating rate bank loan markets are large and growing, and that along with the current opportunity we see in them warrants yield-seeking investors’ attention.

1 High yield bonds market size from Acciavatti, Peter D., Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American High Yield and Leveraged Loan Research, January 9, 2015, p. 40. Loan market size from Blau, Jonathan, James Esposito, and Amit Jain, “Leveraged Finance Strategy Monthly,” Fixed Income Research, January 6, 2015.

2 4 Source SIFMA as of 9/30/2014 for total corporate debt.

3 3 month LIBOR, data sourced from Bloomberg.

4 Acciavatti, Peter, Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Leveraged Loan Market Monitor.” J.P. Morgan, North American High Yield and Leveraged Loan Research. January 5, 2015, p. 7.

5 Acciavatti, Peter D., Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American High Yield and Leveraged Loan Research. February 13, 2015, p. 9.

6 Acciavatti, Peter D., Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2014 High-Yield Annual Review.” J.P. Morgan, North American High Yield and Leveraged Loan Research. December 29, 2014, p. 26.

(c) AdvisorShares