If you were a dog, what kind would you be? I can’t say I’ve thought about it a lot myself, but it is an interesting, possibly introspective question considering the theory that many dog owners pick a breed that looks or perhaps acts like themselves. There’s the Bulldog guy with the similar face, the blonde socialite with a pair of Afghan Hounds trailing alongside, and the paranoid homeowner with a Doberman Pinscher. You get the “picture”. I myself have owned four different dogs during my 70 years, although only one of them came home because of my choosing. Budgie, the German Shepherd, and Daisy, the mutt, were my parents’ choices, and Wiggles, the irrepressible Pomeranian was Sue’s or perhaps 8-year-old Nick’s pick. Nick was so proud of Wiggles that we let him enter her in a dog contest a’ la the movie “Best in Show”. It was immediately apparent however, that Wiggles was no match for the better bred and coiffured competition. Thankfully though, the show was not well attended and there was a category – “home breed” – where no dog was entered. Nick never knew when he was walking Wiggles in front of the judges that he was guaranteed a blue ribbon! Wiggles didn’t seem to care much though, and seemed more interested in sniffing the competition’s crotches than observing their ear placement.

The dog I picked for myself over 35 years ago is at the top of the page – a Golden Retriever, appropriately named, Honey. It would be pretentious to say that I resembled Honey in any way, but nonetheless she was the puppy I chose. Honey turned out to be a little bit of a tramp, so maybe there’s the connection. Back in the freewheeling ‘80s when society had not even contemplated poop scooping and blue pick-up bags, Honey would roam the neighborhood, depositing wherever she pleased, but bringing things back home in return. There was always a fresh assortment of rocks on the front porch, and stale loaves of bread from neighborhood garbage cans. Like the Nathan’s hot dog eating champion, Joey Chestnut, who last July 4th downed 61 hot dogs to win the Coney Island championship, Honey once swallowed four frozen swordfish steaks placed innocently on the kitchen counter. One minute they were there; five minutes later there was nary a trace. Like I say, sort of a tramp. But a loveable one and a loving one, that’s for sure. If you’re into love, and not so much concerned about a fresh fish dinner, I’d recommend a Golden Retriever. If otherwise, I’m sure you’re happy with the mutt in your own “dog” house. Arf, Arf. Sometimes when life seems to be going to the dogs, it’s not necessarily a bad thing.

Like Wiggles, the “home breed” blue ribbon winner, there’s a similar contest going on in global financial markets where the “home country” seeks to outdo the competition in a race to the interest rate bottom. None dare call it a “currency war” because that would be counter to G-10/G-20 policy statements that stress cooperation as opposed to “every country for itself”, but an undeclared currency war is what the world is experiencing. Close to the same thing happened in the 1930’s, a period remarkably similar to what many countries’ policies resemble today. “When the going gets tough” as the saying goes, “the tough get going” and back during the Great Depression, the first countries to abandon the gold standard and get going were the first ones to escape the clutches of the depression.

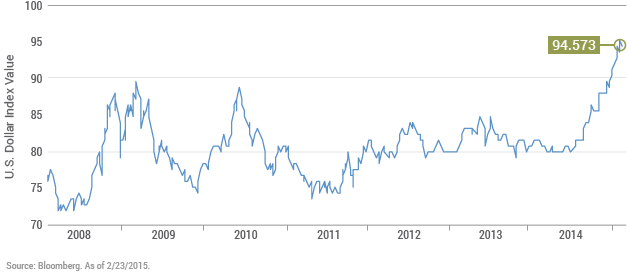

This time, following the Great Recession, it was actually the United States that gained first mover advantage, lowering interest rates to near zero percent by the beginning of 2009, initiating quantitative easing (QE) policies far sooner than competitors, and in effect devaluing the dollar by 15% over the next several years as shown on the following Chart I. Analysts speculate as to why the U.S. has been the blue ribbon growth winner during the global recovery but seldom do they attribute part of the prize to an early devaluation of the dollar and the competitive advantage it earned via global trade. Others caught on with a lag however, and the U.S. tailwind from competitive devaluation has since stalled – in fact the tailwind has now turned into a headwind. While it was once the only breed in the show, it now competes against better coiffured currencies with their own QE’s and promises to hold interest rates for lower and longer than does the U.S. Japan has a quantitative easing program 2 to 3 times greater than our own in comparative GDP terms and the ECB of course is about to embark on its own grand journey into the vast unknown of bond buying, yield lowering, and presumably further Euro currency devaluation.

Chart I: Stronger Dollar = Lower Growth

U.S. Dollar Index 2008 – 2015

What is remarkable about the ECB’s program to come, however, and that of other nations within the European Union which issue their own currency, is the extent to which yields have fallen – or been set – in order to regain a competitive currency edge. First the Swiss, then Sweden, then Denmark. Russia of course, was devaluing daily because of oil and geopolitical tensions. Promoting almost all of these devaluations were policy rates that went negative – that’s right, short term money market rates that would cost banks and ultimately small savers to lend money, as opposed to good old fashioned positive rates that at least offered something in return. The universe of negative yielding notes and bonds in Euroland now total almost $2 trillion. Not even “thin gruel” is being offered to our modern day Oliver Twist investors. You have to pay to come to the dinner table and then sit there staring at an empty plate.

The possibility of negative interest rates was rarely if ever contemplated in academia prior to 2014. No textbook or central bank research paper even mentioned it, although fees for safe haven “storage” have long been in existence at Swiss banks. Ben Bernanke in his famous 2002 paper titled “Deflation: making sure “IT” doesn’t happen here”, mentions helicopters dropping money from the sky, but nowhere was there a hint of negative yields once a central bank reached the zero bound. It was as inconceivable as the “Big Bang” with its black holes that followed billions of years later; the rules of physics or in this case the rules of money didn’t apply; it was impossible to imagine.

But here we are. Negative 25 to 35 basis point money market rates in Germany with minus signs all the way out to six year maturities, reflecting the expectation that negative policy rates are likely in store for at least 3 to 4 years in the future. Sweden has gone the furthest with negative 75 basis points but Switzerland and Denmark are not far behind. Outside the EU, Japan is on a mission of once swift and now gradual devaluation of the Yen via QE – their interest rates having been near zero for years. Even China is lowering its rates seemingly to weaken its Renminbi relative to the dollar and is having some success in doing so.

All of this may seem positive for future global growth and in some cases it may be – lower yields make sovereign and corporate debt burdens more tolerable and their exports more competitive. But common sense would argue that the global economy cannot devalue against itself. Either the strong dollar weakens the world’s current growth locomotive (the U.S.) or else their near in unison devaluation effort fails to lead to the desired results, much like Japan experienced after its 50% devaluation against the Dollar beginning in 2012.

A more serious concern however, might be that low interest rates globally destroy financial business models that are critical to the functioning of modern day economies. Pension funds and insurance companies are perhaps the most important examples of financial sectors that are threatened by low to negative interest rates. Both sectors have always attempted to immunize their long term liabilities (retirement, health, morbidity) by investing at a similar duration with an attractive yield. Now that negative and in almost all cases low short term rates are expected to persist, long term bonds and similar duration assets do not offer the ability to pay claims 5, 10, 30 years into the future. With 10 year German Bonds at 30 basis points and the possibility of them going negative after the beginning of the ECB’s QE in March, what German, Dutch, or French insurance company would attempt to immunize liabilities at the zero bound or lower? Immunization makes no economic or business sense at these levels; similarly for pension funds. In fact even households are handcuffed by low/negative yields, who everyday must now address their inability to save enough money at a high enough rate to pay for education, healthcare, and retirement obligations. Negative/zero bound interest rates may exacerbate, instead of stimulate low growth rates in all of these instances, by raising savings and deferring consumption.

This possibility may be one reason why the Fed appears to be moving to raise interest rates gradually beginning in June this year. In an attempt to elevate returns, investors and savers do all the wrong things required of a stable capitalistic model. Savers save more, not less, and invest at higher risk levels in order to reach their long term liability expectations. Asset prices for stocks, high yield bonds and other supposed 5-10% returning investments, become stretched and bubble sensitive; Debt accumulates instead of being paid off because rates are too low to pass up – corporate bond sales leading to stock buybacks being the best example. The financial system has become increasingly vulnerable only six years after its last collapse in 2009.

Investors and bondholders who have cheered every instance of lower and now sub-zero yields in developed countries because of near-term capital gains that accompany them, must now beware of the potential negative consequences going forward. Central banks have gone and continue to go too far in their misguided efforts to support future economic growth. “Home bred” monetary policies earn “blue ribbon” rewards in the short term, but in the long run may undermine the entire show and send the dogs towards the exits. Stay conservative in your investment portfolio. Own high quality bonds and low P/E, high quality stocks if you want to stay out of the doghouse. Arf, Arf.

-William H. Gross