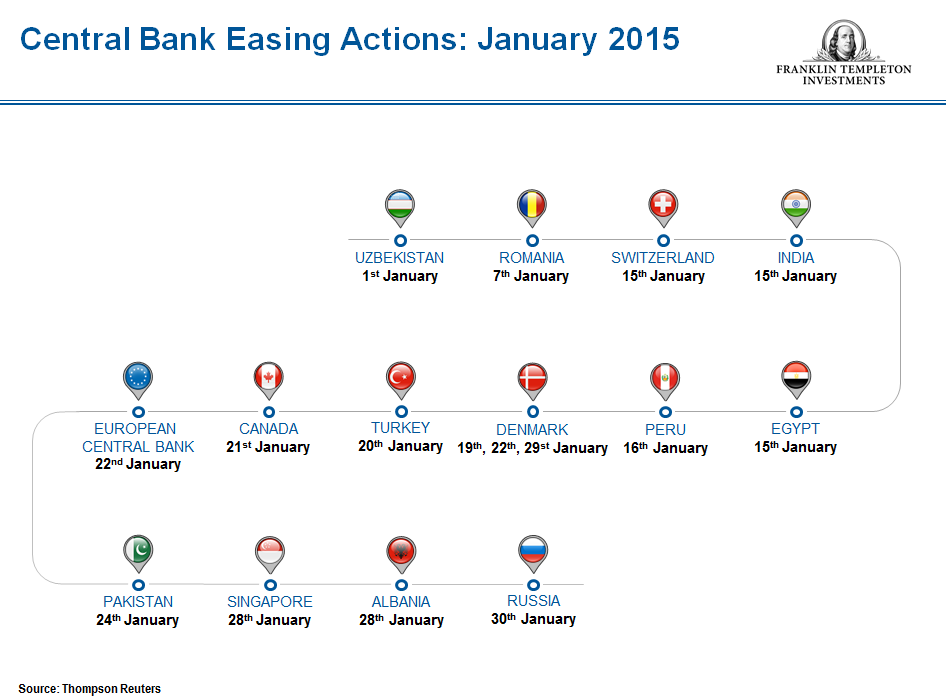

This year we expect the divergence in monetary policy among the world’s central banks to be a key theme and a likely driver of asset flows. For now, the scorecard seems to be tilted toward monetary easing since in the first month of 2015 alone, 14 central banks engaged in some form of monetary policy loosening, generally in the form of interest rate cuts or asset purchases.1 Denmark’s central bank has been particularly aggressive in regard to the former, slashing interest rates four times in a three-week period already this year, while the European Central Bank (ECB) announced plans to step up its quantitative easing (QE) game plan, taking a page from the playbook of the US Federal Reserve (Fed) and Bank of Japan.

When it comes to QE, “easing” really isn’t an accurate description—in actuality, it is about expanding rather than easing. The first phase of the Fed’s money-creation program (QE1) started in late 2008 in response to the US sub-prime financial crisis, in the form of a program to purchase government debt, mortgage-based securities and other assets primarily from banks who were suffering from the declining value of those assets. The original program was set at US$600 billion, but the expected economic recovery and ending of tight credit did not materialize as expected. Hence, QE2 was launched in 2010, and then two years later, QE3, as policy makers became more and more desperate to create the required economic stimulus. In total, more than US$4 trillion (close to the size of China’s foreign exchange reserves) was spent, about six times the original plan. The result was a three-fold expansion of the Fed’s balance sheet.

In my view, what’s most important to note is that during those years the United States was not the only country to launch such a program. In the United Kingdom, a £75 billion (about US$120 billion) program was launched in 2009, and that program was gradually expanded to £375 billion (about US$600 billion). The Bank of England’s balance sheet expanded four-fold; the government was using new money to buy back its own debt. Improving economic conditions in both the United States and United Kingdom have now turned the discussion in those markets toward the timing of a wind down and potential interest rate increases ahead.

As easing decelerates in the United States and United Kingdom, it marches on in other countries. In October 2014, the Bank of Japan expanded its monetary policy efforts, increasing asset purchases to ¥80 trillion annually (US $674 billion). Dubbed by some as “quantitative and qualitative easing,” or “QQE,” Japan’s central bank has been battling deflation and attempting to jumpstart years of economic stagnation.

The eurozone continues to suffer the fallout from sovereign debt problems and a prolonged period of anemic growth, accompanied by deflationary side effects. So in January, the ECB applied a similar QE solution as in the United States and Japan by announcing plans to purchase at least €1 trillion in bonds starting in March, the central bank emphasized its desire to inject liquidity into the markets.

In emerging markets, we have also seen some policy divergences but the general bias seems toward easing at this stage. Let’s take a look at a few key recent policy actions and some of the rationale behind them.

China (Easing)

Following a surprise interest rate cut in November, on February 4, the People’s Bank of China (PBOC) cut banks’ reserve requirement ratios (RRR) by 50 basis points (0.50%), with the goal of fueling an estimated 600 billion yuan (US$96 billion) into the money supply. The PBOC also announced an additional 50 basis-point cut in RRR cut for smaller financial institutions focused on micro enterprises and agricultural lending, as well as a 400 basis-point RRR cut (4%) for the Agricultural Development Bank of China (ADBC). The government hopes these measures provide an economic boost amid a number of weaker-than-expected statistics, including a key manufacturing barometer, the Purchasing Manager Index (PMI), which dropped below 50 in January 2015. China’s government reported gross domestic product (GDP) growth for 2014 as a whole rose 7.4% on a year-over-year basis, compared with an increase of 7.7% in 2013. We at Templeton Emerging Markets Group are not concerned that China’s growth has been slowing, and believe 7%+ growth for an economy of this size appears quite robust. Nonetheless, the PBOC clearly has its eye on ensuring China remains a global growth engine, and it would not be surprising to us to see further easing measures this year.

India (Easing)

India has been in the easing camp as well, despite robust GDP growth. A revision in the methodology used for calculating national accounts data, which brings India’s GDP statistics closer to global standards, led to a significant upward adjustment to the country’s most recent GDP data. Newly released data from the Indian government indicated that GDP growth increased to 6.9% year-over-year for the fiscal year ended March 2014, from 4.7% previously. Similarly, growth for the fiscal year 2012-13 was adjusted to 5.1% on a year-over-year basis from 4.5%.

In January, the Reserve Bank of India surprised markets with a 25 basis points (0.25%) cut in the key interest rate to 7.75%. Easing inflationary pressures led the Bank to reduce interest rates as part of efforts to further boost economic growth. Then, on February 3, the statuary liquidity ratio (which measures the share of demand deposits and liabilities that banks must hold as reserves) was lowered to 21.5% to help encourage banks to lend. While India’s consumer price index increased to 5.0% in December 2014 on a year-over-year basis from a record low of 4.4% in November, the rate remained significantly lower than the 8.8% recorded in January 2014, adding some measure of comfort to loosening policy. Reserve Bank of India Governor Raghuram Rajan has stated lower oil prices have dampened the threat of inflation in the country, and indicated that further interest rate cuts could be forthcoming.

Russia (Easing)

Russia’s Central Bank unexpectedly reduced its benchmark interest rate by 200 basis points (2.0%) to 15% in January to support the domestic economy. The central bank had previously raised interest rates to 17% from 10.5% in December as part of efforts to stabilize the Russian ruble and curb inflationary pressures. Inflation rose to its highest level in more than five years in December largely due to higher food costs, as the consumer price index jumped to 11.4% on a year-over-year basis from 9.1% in November. In the past couple months, the government announced a series of measures worth at least US$35 billion to tackle the economic crisis in the country. Measures included a US$15.7 billion recapitalization of the banking system and US$4.7 billion capital injection into the state development bank to allow it to increase lending to support the domestic economy. Clearly, Russia still has a number of challenges ahead that monetary policy alone cannot solve. In January, international ratings agency Standard & Poor’s downgraded the country’s sovereign credit rating to BB+ from BBB-, below investment grade status, citing deteriorating asset quality in the financial system as a result of the weaker ruble, restricted access to international capital markets due to sanctions and likely economic recession in 2015.

Turkey (Easing)

The central bank in Turkey reduced its key benchmark interest rate by 50 basis points (0.5%) to 7.75% in January as inflationary pressures eased following a decline in oil prices. The consumer price index eased to 8.2% on a year-over-year basis in December, from 9.2% in November. Turkey is facing a number of crosswinds. The central government budget deficit widened more than 20% year-over-year to US$9.9 billion in 2014, and according to the Turkish Ministry of Economy, the current account deficit for 2014 was US$45.8 billion, narrowing from $64.7 billion in 2013.

Brazil (Tightening)

Brazil would probably like to see some of the deflationary pressures Japan and the ECB have experienced, as Brazil’s consumer price index rose 6.4% in 2014, the fastest pace since 2011 and above the central bank’s target. A significant cause was the depreciation of the Brazilian real which declined 11% against the US dollar in 2014.2 Despite sluggish economic growth in Brazil, inflation worries prompted its central bank to raise the benchmark interest rate by 50 basis points (0.5%) to 12.25% on January 21 (the third straight rate hike) to its highest level since August 2011. Consumer confidence recently reached its lowest level since 2005 in Brazil as people grew increasingly concerned about the worrisome combination of rising prices and weakness in the job market. Brazil’s public sector primary fiscal account posted its first deficit in more than a decade in 2014. Lower tax revenues and higher government expenditure ahead of the presidential elections in October resulted in a deficit of US$13.8 billion, or 0.6% of GDP. In order to support the government’s fiscal crisis Finance Minister Joaquim Levy announced a number of measures, including increases in taxes on fuels, credit and imports as well as the end of tax breaks on automobiles.

Putting It All Together: Investment Implications

In my view, the easing programs put in place by the world’s major central banks may have helped spur economic growth, but also have, in many respects, allowed banks to avoid making tough decisions regarding their bad investments. Meanwhile, much of the money that was intended to flow out to the marketplace has remained on the banks’ balance sheets, much to chagrin of the central bankers who wanted the banks to initiate lending so their economies would revive.

The low interest rates we see globally in many markets are now a disadvantage to regular bank deposit savers and pensioners, while the equity investors have generally benefitted. Many savers who have suffered with low interest rates could be hit with another problem down the road resulting from all this easing—high inflation and asset bubbles. The recent decline in the price of oil has helped provide a cushion, but we don’t envision oil will remain this low long term. Additionally, there are concerns about “currency wars” breaking out amidst all the easing maneuvers, as countries battle to weaken their currencies to seek to boost export growth.

For now, we believe the most recent easing efforts of Japan, the ECB, China, India and other central banks should offset concerns about potential interest rate increases coming this year from the Fed and possibly others. We think central bank easing efforts will continue to provide liquidity to the markets, and expect that could help drive flows into equities globally as investors search for yield. But, we’ll also be watching for any potential aftershocks.

Mark Mobius’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

© Franklin Templeton Investments