Complexity, Critical States and Tributaries of Uncertainty

For long periods of time, the markets can advance relatively smoothly until a sudden onset of chaos occurs, a “tipping point” that quickly changes the picture. Some might say the recent drop in oil would be a case in point. Brooks Ritchey, senior managing director at K2 Advisors, Franklin Templeton Solutions, explores the tipping points that trigger dramatic market turns, and ponders whether he thinks global equities may be teetering on the edge of one today.

J. Brooks Ritchey

Senior Managing Director at K2 Advisors, Franklin Templeton Solutions

In the March 2010 issue of Foreign Affairs Journal, Harvard history professor Niall Ferguson published a terrific article (IMHO) outlining the complexity of systems and the interaction of forces as it relates to the rise and fall of great societies throughout history. In it he described how large empires could be defined as complex systems that are “asymmetrically organized,” meaning their construction more resembles a termite hill than an Egyptian pyramid. As complex systems, these societies tended to share certain observable and ubiquitous features. These included the interaction of many dispersed agents, multiple levels of organization, sometimes a lack of central control, continual adaptation, incessant creation of new niches and the absence of uniformity. The author went on to describe how these systems operated somewhere between order and disorder—on “the edge of chaos” as he suggested—appearing quite stable for long periods and seemingly in a state of equilibrium. Eventually, however, this observable equilibrium would be disrupted. Very often it would be an ostensibly small event or action, a “tipping point,” that would trigger a meaningful disruption.

Scientists define this notion of “edge of chaos” as being in a “critical state” or near “phase transition,” such as the moments prior to water turning to steam or ice, or just before a nuclear reaction. This concept is not exclusive to the academic halls of science, however, nor is it restricted to applications related to states of matter and energy. These “tipping points” leading to “phase transitions”—sometimes insignificant and sometimes world changing—surround us every day in the interactions and activities of our collective experience. They are at work in the earth’s crust when shifting tectonic plates lead to an earthquake in California, in society when the courageous decision of a heroic black woman to no longer sit unjustly at the back of a bus leads to a paradigm shift in civil rights and cultural thinking, and of course in stock markets where home foreclosures in Nevada end with the bankruptcy of one of the most staid and iconic financial institutions on Wall Street.

Tipping points and phase transitions are everywhere and always, and could happen upon us at any moment in any circumstance. In terms of the markets, our world could easily be assessed as one that is perpetually on the brink of phase transition, or as described by economist John Mauldin in a “state of stable disequilibrium.” That is to say that participants from all over the world are connected inextricably together in a complex and layered loom of investments, debt, trade, globalization, international business, finance, currency and banks. All operate in a critical yet stable state, in between periods of market rest (low volatility and bull runs) and reaction (high volatility and bears).

So this then begs the question, what are the sorts of tipping points that may trigger a market phase transition? Are they observable? Can they be monitored and anticipated?

Sand Piles

In the book Ubiquity: Why Catastrophes Happen (Crown Publishing, 2002) social scientist Mark Buchanan explores the concepts of complexity theory, chaos theory and critical states. While not directly addressing investments, the book does provide some insight and understanding as to why financial markets can seemingly advance for long periods relatively smoothly, sometimes years, until a sudden onset of chaos or Nassim Taleb’s “Black Swan”-type of events emerge, triggering market corrections or crashes.

The book describes the work of three physicists studying in 1987 at the Brookhaven National Laboratory on Long Island. The physicists, Per Bak, Chao Tang, and Kurt Wiesenfeld, used a computer program to create a virtual sand pile. The program was designed to stack one virtual grain of sand at a time and monitor the results, with an eye toward studying “non-equilibrium systems,” i.e., the crazy world that surrounds all of us every day—Wall Street notwithstanding. Over the course of their experiment the physicists learned some really interesting things. One might assume that they would have been able to observe some sort of pattern-like behavior in the sand pile, such as a typical size or number of grains required before a collapse, but this was not the case. On the contrary, each time the experiment was run the results were completely chaotic in their unpredictability. After a large number of tests with millions of grains of sand, they observed no patterns, no typical number required to trigger a system collapse. Sometimes it was a single grain, others 10, 100 or 5,000. Still others involved massive mountains of sand incorporating millions of grains that would collapse in a single and seemingly random onset of failure. In other words literally anything, at any time, might be just about to occur. Perpetually on the brink of phase transition.

This kind of stuff sticks with me when I think of the markets … and positioning portfolios.

In an attempt to gain some insight into the cause of such unpredictability in their sand pile game—or in an effort to assign some order to the disorder they observed—the scientists pushed their experiment further. Now they looked at the virtual sand pile from above, and they color coded its regions according to steepness, with relatively flat areas green and steeper sections red.

In the beginning the pile was mostly green of course (though it still would collapse periodically) but as the game progressed more red areas began to infiltrate, until eventually a dense skeleton of random red danger spots coursed through the sand like tributaries in the Mekong Delta. This offered some insight into the peculiar behavior (though no real predictability), as a grain of sand falling on a red spot could, by domino-like action, cause a sliding at other nearby red spots.

If the red network was sparse and all trouble spots were well isolated, then a single grain would likely have only limited repercussions if any; again, the triggering was random. But as the red spots began to grow and interconnect the impact of the next grain would become fiendishly unpredictable. Sometimes it fell innocuously and did nothing to the pile, sometimes a few grains tumbled, and every so often it set off a cataclysmic reaction sending walls of sand cascading down the entire pile.

Tributaries of Uncertainty

The author defines these as fingers of instability, but I prefer to consider them tributaries of uncertainty, and not for any copyright infringement risk or pride of authorship, but because “instability” implies, in a way, that an avalanche is imminent, when in fact the experiment showed there is no rhyme or reason. Things can happen just as easily as they cannot. The point being that we are always uncertain, and so we must always be prepared and sheltered appropriately for living in the uncertain world, investment portfolios notwithstanding.

If we did learn anything from the sand pile experiment it is that while we cannot predict what grain of sand may trigger the next phase transition, we can get a sense of the potential size and scope of any imminent disruption to the pile by looking at the steepness and the interconnectedness of the tributaries.

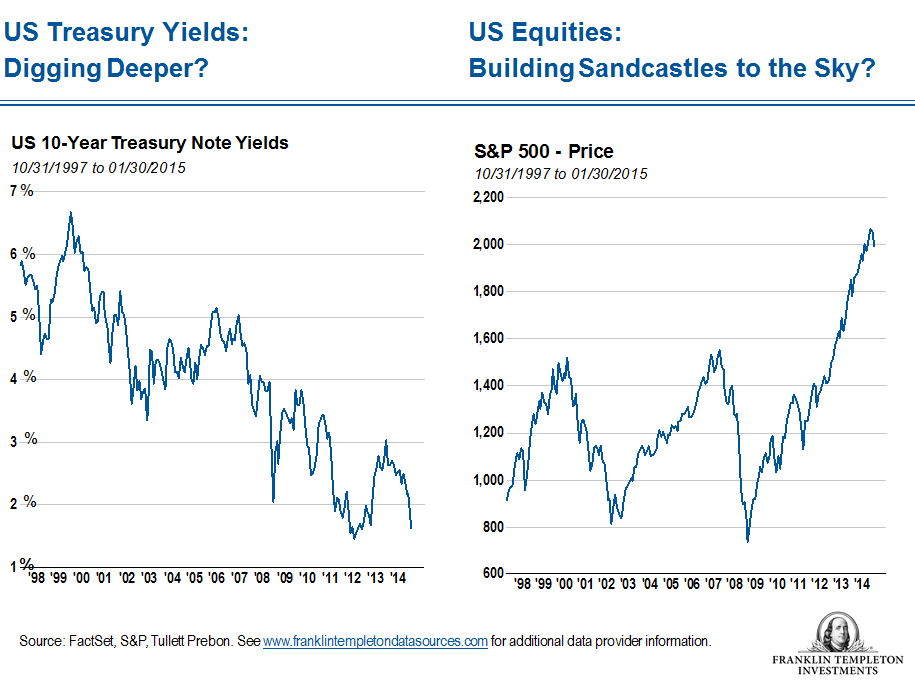

In terms of steepness of the market sand pile, there are ample data that we can observe that illustrates—both literally and figuratively—there is much surrounding us today. That said, we can observe that a significant number of tributaries of uncertainty throughout the pile appear quite extended.

So what about market interconnectedness, the other factor in the sand experiment? Unfortunately quantifying market interconnectedness is a bit more difficult from a data analysis standpoint. If there is a resonant lesson from periods of chaos such as 2008, 1987, etc., however, it is the understanding that things that do not correlate in normal conditions can and often do when sand castles crumble. That much we can be certain of.

The bottom line is that, while I cannot see the future, I do not believe the global marketplace is going to experience a major crash anytime soon (ideally never). Indeed, I am actually optimistic about prospects for equities this year. Nonetheless, I feel markets getting more fragile and volatile as the years move on. On some days it just feels spooky, and certainly not the time to be a full-on bull across the board. The markets today are like nothing they were even 10 years ago. That is not to say they are riskier, because again that is such an abstract and immeasurable quantity to gauge in aggregate that no one could ever know. But it is fair to say they are more complex, even by 2008 standards. The number of participants, assets under management, trading strategies, number of tradable instruments, the light-speed at which information is moved and processed … all of these are grains of sand building the pile. When things go wrong in a complex system, the scale of disruption is nearly impossible to anticipate. There is no such thing as a typical or average forest fire, for example. To use the jargon of modern physics, a forest before a fire is in a state of “self-organized criticality”: it is teetering on the verge of a breakdown pending a spark, but the size of the breakdown is always unknown.

I do not know if the divergence we see among central banks in the world will continue. I have no idea if commodity prices will continue to collapse or if a rapid gain in US dollars versus foreign currencies will spark further deflation and contagion. Are 30-year lows in bond market yields hinting at an economic sinkhole?

The one thing I do know—and firmly believe— is that it is imperative to build a portfolio that is effectively hedged and diversified.

Brooks Ritchey’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal.

Diversification does not guarantee profit or protect against risk of loss.

(c) Franklin Templeton Investments

© Franklin Templeton Investments