Weighing the Week Ahead: Help for the Economy from Housing?

The economic calendar includes much more housing data than we normally see in a single week. With Fed Chair Yellen’s Congressional testimony and the GDP revisions also on tap, I expect many observers to be linking these topics. They will ask:

Is it finally time for a housing rebound?

Prior Theme Recap

In last week’s WTWA I predicted that the punditry would focus on the new record in stocks, and especially on whether energy stocks would support the breakout. Those were indeed two major themes all week and they were frequently linked, so the question was accurate. Mostly the answer was rather negative. The stock rally continued, but without help from most of the energy sector.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

The quirks of the calendar include some of the major economic reports on housing – new sales, existing sales, and pending sales – along with Case-Shiller and FHFA pricing and the mortgage index. There is a lot of fresh information.

We will see the second estimate of Q4 GDP, with many wondering about the role of a possible housing rebound. Janet Yellen will testify before two Congressional committees, elaborating on current Fed thinking. And finally, the remaining earnings reports feature some of the major companies associated with home construction.

The confluence of these factors will spark the question: Can Housing Finally Contribute to the Economic Rebound?

The Viewpoints

There is a wide range of opinion on housing:

- Fundamental weakness. Some major opinion leaders, including Jeff Gundlach, Laurence Fink, and Sam Zell note the changing demographics and issues in supporting the mortgage market. (This article is from last year, but lays out the reasoning effectively).

- Miscellaneous bearish factors. CNBC’s Diana Olick covers the housing beat and always seems to find a threat to the rebound. A look at her blog’s index page shows stories about the trickle down of high rents to small cities, expected weakness in Houston from falling oil prices, lack of impact from more jobs, higher mortgage rates, negative effects of a strong dollar, and similar stories.

- The long bottom. Calculated Risk has been the leading exponent of this view. The data show that some of the new construction represents owner-built starts and homes intended for rent. Bill recommends consideration of this chart:

- Positive developments. Jonathan Golub of RBC notes that household formation is booming:

As always, I have some additional ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good news last week.

- Progress in Greece. After a slow start to the week, including a German spokesman calling the Greek proposal a “Trojan Horse,” there was finally a firm agreement — to delay for four months. As I noted last week, this type of negotiated solution is actually quite typical. Each side does as little as possible. There is an opportunity for face-saving. The worst crisis outcome is averted. Markets seemed less worried about Greece than three years ago, and celebrated the Friday agreement.

- Weekly jobless claims dipped. Back below 300K. Calculated Risk analyzes and charts the significance.

- Port deal reached. This news broke on Saturday, so it is not reflected in Friday’s closing prices. As I have noted in recent weeks, the Longshoreman slowdown and the accompanying lockout were threatening a major economic disruption. It will still take weeks to resume normal shipping, but this is very good news.

The Bad

There was only a little bad news.

- Ukraine cease fire breaks down. This is a continuing human tragedy and a major drag on the world economy.

- Earnings reports have weakened a bit. There are still 75% of reporting S&P companies beating on earnings and 58% on sales.(FactSet). The blended growth rate is 3.5% as calculated there or about 7% if you take out energy. Brian Gilmartin notes that Apple contributed half of the ex-energy earnings growth and warns against arbitrarily excluding stocks and sectors. You need a good reason!

- Housing starts and building permits disappointed slightly.

The Ugly

The Fed is worried about a rush for the exit in bond funds. Bloomberg’s Matt Boesler tweeted about a passage in the Fed minutes. (Full story from Myles Udland of BI).

…because investors are using mutual funds to invest in bonds, instead of owning the bonds, there could be a problem if investors all want to leave at the same time.

When you own a bond mutual fund, you don’t actually own a bond which will continue to pay a coupon so long as the issuer isn’t in default, you just own a share of the fund, which is comprised of lots of bonds and sometimes other things.

Also, a bond fund is only going to have so much cash on hand, so if the investors in a certain fund all want to redeem their shares of the fund at the same time, it will pose problems for the fund manager trying to meet redemption requests. Most likely, the manager will be forced to sell some bonds, potentially at a discount, as the fund needs to simply raise cash to meet redemptions.

And ace Fed watcher Tim Duy emphasizes the determination to raise rates.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are welcome. I am seeing plenty of bad charts, but little refutation.

On a related theme, could someone explain why PBS continues to feature the guy who called for Dow 5K before 20K, instead ofsomeone who did the opposite? Do they have an interest in the investment success of their viewers? Can anyone find any such items?

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. This week he notes an increase in his combined measure of economic stress, although the levels are still not yet worrisome.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s Big Four summary of key indicators.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. Georg continues to develop new tools for market analysis and timing. Some investors will be interested in his recommendations for dynamic asset allocation of Vanguard funds and TIAA-CREF asset allocation. He has added a method for Vanguard Dividend Growth Funds. I am following his results and methods with great interest. You should, too.

The Week Ahead

It is a normal week for economic data.

The “A List” includes the following:

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- New home sales (W). Time for a rebound?

- Consumer confidence (T). Conference Board version correlates with economic spending and employment.

- Michigan sentiment (F). Same concepts as Conference Board, but using a panel design.

The “B List” includes the following:

- Existing home sales (M). Less important for the economy than new construction, but still significant.

- Durable goods (Th). Continuing weakness in volatile series?

- CPI (Th). Inflation is still not important in these ranges, but always watched closely.

- GDP (F). The second estimate. Backward looking but still noteworthy.

- Chicago PMI (F). Gets extra attention when occurring right before a weekend. Best regional report for predicting the ISM index.

- Crude oil inventories (W). Maintains recent interest and importance.

There is plenty of FedSpeak, featuring Chair Yellen’s “Humphrey Hawkins” testimony before a Senate Committee on Tuesday. The House gets a chance to question her on Wednesday. There are at least four other appearances by Fed Presidents on Thursday and Friday.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

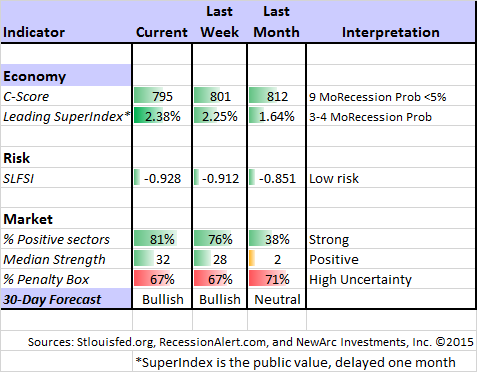

Felix has continued a “bullish” posture for the three-week market forecast. The data have improved a bit, but are only slight better than the recent neutral readings. There is still plenty of uncertainty reflected by the high percentage of sectors in the penalty box. Our current position is still fully invested in three leading sectors, and we have gotten more aggressive. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com.

As I have noted for six weeks, Felix continues to feature selected energy holdings. Felix is not just a momentum trader!

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a new page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

My bold and contrarian prediction for 2015 – that the leading sectors would lose and the laggards would win – looked a lot better over the last two weeks. If I am correct, there is a very, very long way to run for the cheapest market sectors – energy, technology, cyclicals, and financials.

Other Advice

Here is our collection of great investor advice for this week:

Personal Finance

Abnormal Returns continues to focus on personal finance in the Wednesday links. Read them all, but I especially like Morgan Housel on risk and David Merkel on why investors underperform stock averages.

Stock and Sector Ideas

Warren Buffett cuts back on big oil. Others debate his wisdom. (Barrons)

Five reasons not to expect a big rebound in oil prices. (Tim Mullaney at MarketWatch).

The place for bonds, even when rates are rising. Mark Hulbert shows how intermediate bonds can show gains even when rates are rising sharply. The basic idea is to keep the maturity short and reinvest as rates move higher. (This is the concept we follow in our bond ladder). Bonds are also essential for those who need to reduce the volatility of a pure stock portfolio.

Cam Hui suggests that it might be time to buy Greece. His article was published the day before the announcement, but is well worth reading, especially for those who like some technical support for fundamental ideas.

A longer term chart of the Athens General Index and the US Greek ETF GREK also tells a similar story. Greek stocks look washed out, especially when they don’t react negatively to bad news.

Health insurance companies that support Medicare Advantage are benefiting from the influx of “younger seniors.” (Wedbush via Barrons). I enjoyed some of these names last year, but sold on a valuation basis as new highs were reached. Time to revisit the price targets?

Market Outlook

Robert Shiller may be reducing his holdings of US stocks. Media questioners always try to get him to predict an imminent crash. Market bears use his CAPE ratio as the foundation for demonstrating an over-valued market. Most people would be surprised to learn that he continues to hold over 50% stocks, an aggressive allocation given his age. He has also recently been noting risks in bonds.

Morgan Stanley sees another 1000 points in the S&P 500 as foreign investors join the party.

Final Thought

Most economic recoveries have help from the housing sector. Part of the reason for below-trend growth has been the continuing missing elements. We have had drags from government spending (especially local), business investment, weather, and housing. Gene Epsteintakes note of this as follows:

The U.S. economy is in the benign grip of a virtuous circle, with key positive factors reinforcing one another, all of them lubricated by low energy prices. Employment gains are driving up wages and salaries, which are driving consumer spending, which is encouraging capital investment, which is in turn motivating business to hire.

So far, however, the housing market has been barely participating in that virtuous circle. Monthly housing starts have been running at an annual rate of only a little over a million, nothing like the 1.5 million that could be seen if household formation begins catching up with the increase in the population.

Household formation could heat up by 2016 as labor markets become tighter. Then growth of 4% could finally become a reality.

He has a good point. I expect a final surge in economic growth during this business cycle, and it might take two or more years to play out.