Recently the Dow Jones Industrial Average closed above 18,000 and the S&P 500 Index reached a new record high. Geo-political concerns in the Middle East and Ukraine don’t seem to be able to keep the market down, nor do the tepid economic growth numbers coming from Europe and China. Finally, corporate earnings expectations have been moderated significantly for 2015 and that doesn’t seem to matter to stock prices either. Perhaps the explanation is in the sentiment.

Mardi Gras (French for Fat Tuesday) represents the culmination of the festival season, which for Christians extends from the Epiphany in early January to the day before Ash Wednesday. This celebration provides people an opportunity to imbibe in the things they will most likely go without during the Lenten season.

Stock prices are supposed to be based on fundamentals. The price of a company’s stock should represent its future earnings power, the growth of those earnings and the company’s revenue. It also should represent the value of future cash flows to the extent that the company pays a dividend and has the ability to growth that dividend payout over time. Discounting these future cash flows and earnings back to the present provides insight into a company’s stock price.

However, often the actual value of a company’s stock, based on these fundamental factors and the current stock price, look nothing like one another. Research analysts who look at companies’ future earnings potential are asked by their clients to provide an estimate on what those companies will earn. Experience tells us that the further out into the future you ask an analyst to predict earnings the more likely their estimates are to be off. However, the direction of analysts’ earnings estimates does provide some useful information regarding the level of earnings growth an investor can expect in the near-term.

When taken in the aggregate, these estimates may provide some useful information regarding how different the current market valuation is from future earnings growth expectations. As an example, when combining the earnings estimates for the stocks in the S&P 500 Index, the Index is expected to earn $118.79 in 2015 as of last Tuesday. At the beginning of the year, the expectation was for companies to earn $131.01. This 9.4% decline in earnings expectations has had virtually no effect on the direction of stock price movement as the S&P 500 Index has rallied from 2058.90 to 2096.99 or 1.85% since the end of 2014. To what can we attribute this divergence in opinions between analysts and the market?

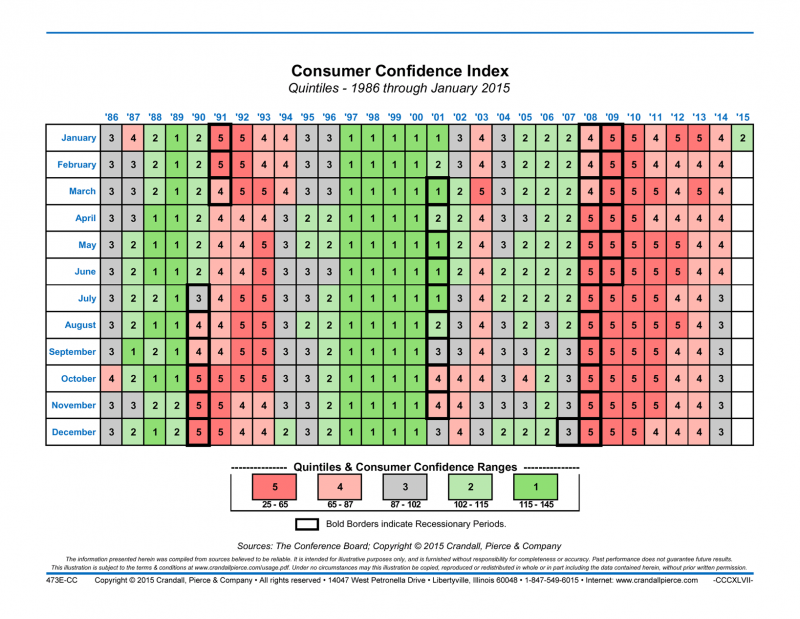

There are several explanations. The first of these really has to do with consumer confidence. The recession that began in 2008 took its toll on consumers. The chart below provides an indication as to just how bad confidence has been and for how long. The chart looks at confidence each month going back to 1986. Green and light green represent periods where confidence is near the top of its measured range while pink and red represent the bottom of the range. As you can see the bold periods represent recessions. Since the recession of ’08 and ’09, consumer confidence has been pegged near the bottom of the range until the middle of last year. As employment and wage increases begin to improve, and frankly gas prices declined, confidence has been improving. So much so that for the first time since August of 2007 we have made it back to green!

Consumer Confidence

The next most plausible reason for stock prices to continue their climb higher in the face of declining earnings expectations is the recent announcement by the European Central Bank (ECB) that they are going to engage in a lengthy period of quantitative easing (QE). They have indicated that they will purchase over $1.2 trillion of bonds to provide economic stimulus to the European economy. We know from our recent history lesson in the U.S. that when our own Federal Reserve engaged in similar activity it lifted asset prices. There were four versions of QE in the United States taking place over the last seven years (QE 1 started in November of 2008, you can find the history of U.S. QE here). During that period stock prices rose with the Fed’s balance sheet.

There is no reason to believe that asset prices won’t also be lifted by the ECB’s new QE program. The question of course is which asset prices. It may be that the stocks of companies domiciled in the European Union are most affected which means that a healthy allocation to international investments makes sense going forward.

Another reason for the divergence between stock prices and earnings expectations is that investors are presuming that analysts are too aggressively lowering their estimates. Investors know that analyst estimates are suspect over time. The decline in earnings estimates is a function of the decline in oil prices and the impact that has on energy prices as well as the impact the stronger dollar has on earnings.

Perhaps investors are looking past the energy sector’s earnings difficulty and the strength in the dollar and focusing more on domestic and foreign economic growth. While modest today, investors seem to hope for a better tomorrow. If that stronger growth comes to fruition, then these stock prices will be supported in the second half of the year by upside earnings surprises. If not, then like many Milwaukee residents the day after Fat Tuesday, investors will be feeling like those who ate too many paczki’s.

(c) Cleary Gull