High Yield in a Rising Rate Environment: Duration and Yield

By: Heather Rupp, CFA, Director of Research for Peritus Asset Management, the sub-advisory firm of the

AdvisorShares Peritus High Yield ETF (HYLD)

We began February with a yield on the 10-year Treasury of 1.68% and today sit at 2.14%.1All the concerns and talk of maybe even no rate rise this year that we saw in January, have turned to frequent mention of a rate rise beginning in June. So what are bond investors to do? Is this finally the year of rising rates and what impact does that have?

Yes, it is well understood that the Federal Reserve will be raising the federal funds rate off of the 0.0-0.25% target that we have seen since the financial crisis. The timing is anyone’s guess, but at the end of the day markets are forward looking mechanisms and have/will price this move in long before it actually happens. Even if the Fed does start to raise rates this year, we don’t expect them to do so rapidly and we don’t expect their actions to have a dramatic impact on the 5- and 10-year Treasuries.

That being said, one thing we know over the last year is that interest rate moves have surprised nearly everyone. But what about investors that are concerned rates will make a sizable move up and with that, how various fixed income asset classes will perform in this environment? Let’s take a look at some data points.

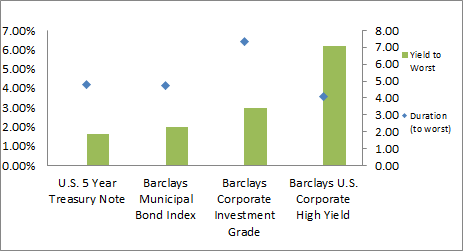

One primary way to evaluate interest rate sensitivity is with duration, a measure of the price change of a fixed-income security in response to a change in interest rates. Per this calculation, rates and prices move in the opposite direction, so an increase in rates would produce a decline in price. Below are the durations and yields for various fixed income asset classes.2

As you can see in the chart above, municipal bonds and the 5-year Treasury carry a duration near 5 years, investment grade bonds have a duration of over 7 years, and high yield bonds offer the lowest duration of just about 4 years, meaning the high yield asset class carries the lowest sensitivity to interest rates. In other words, all else equal, a given increase in interest rates will move the price of investment grade bonds down significantly more than high yield bonds.

The number of years to maturity for the asset is one factor in determining duration, but the starting yield also plays an important role. After a big run in 2014, municipals now offer a yield to worst only slightly over that generated by the 5-year Treasury, both under 2%. The yield to worst on the investment grade index is about 3%, while the broader high yield index offers a yield to worst of twice that, over 6%. So not only do high yield bonds offer the lowest duration, they also offer the highest yield. So how does that play into a rising rate environment? Well, it means that high yield bonds are much less interest rate sensitive than these other fixed income alternatives. And while the traditional adage in fixed income is that as interest rates go up, prices on bonds go down, that doesn’t factor in the yield being received which may outweigh the price decline, all else equal. So investors need to consider both yield and duration.

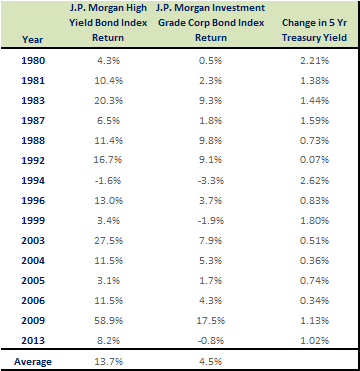

Looking back through history when we have seen rates rise, we have certainly not seen weak returns in the high yield market. For instance, in the 15 years that we have seen Treasury yield increases (rates rise) since 1980, the high yield bond market has posted an average return of 13.7% (or 10.4% if you exclude the massive performance in 2009). This compares to an average return of 4.5% (or 3.6% if you exclude 2009) for investment grade bonds over the same period.3

Intuitively this makes sense because generally rates rise during periods of economic strength, and a strong economy is generally favorable for corporate credit. Historically we have seen the prices of high yield bonds much more linked to credit quality than to interest rates.

For all the chatter that bonds will get hit as rates rise and it is time to move to equities, this historical data would indicate that high yield bonds have certainly not suffered as rates rose in the past. While we currently have our concerns about longer duration asset classes, such as investment grade and municipal bonds, we believe that high yield bonds are positioned well for the rate uncertainty ahead. If rates don’t move much for the year, then you have a much higher starting yield for high yield bonds, and if rates do increase, the high yield asset class has a much lower duration. Furthermore, also including floating rate bank loans in your portfolio can serve to further reduce your duration.

Right now we see many attractive opportunities for investments for active managers in the high yield bond and loan space. There remain over-valued credits and vulnerable credits (such as certain sub-sectors of the energy space) that we would recommend avoiding, but in the mix are also many bonds and loans that offer value for active managers who can select the securities they feel are positioned well for the environment ahead.

1 5-year Treasury rates as of 2/2/15 and 2/17/15.

2 Barclays Capital U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt (source Barclays Capital). U.S. 5 Year Treasury Note is the on-the-run Treasury (source Bloomberg). Barclays Corporate Investment Grade Index consists of publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and the quality requirements (source Barclays Capital). Barclays Municipal Bond Index covers the long-term, tax-exempt bond market (source Barclays Capital). Barclays data as of 2/13/15 and Treasury data as of 2/17/15. Yield to Worst is the lowest, or worst, yield of the yield to various call dates or maturity date. Duration is the change of a fixed income security that will result from a 1% change in interest rate. The duration calculation is based on the yield to worst date, using Macaulay duration for the various Barclays indexes and Bloomberg calculated duration to workout for 5-Year Treasury.

3 Data sourced from: Acciavatti, Peter Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2008 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 2008, p. 113. “High-Yield Market Monitor,” J.P. Morgan, January 5, 2009, January 5, 2010, January 3, 2011, January 3, 2012, January 2, 2013, and January 2, 2014. 2008-2012 Treasury data sourced from Bloomberg (US Generic Govt 5 Yr), 2013 data from the Federal Reserve website. The J.P. Morgan High Yield bond index is designed to mirror the investible universe of US dollar high-yield corporate debt market, including domestic and international issues. The J.P. Morgan Investment Grade Corporate bond index represents the investment grade US dollar denominated corporate bond market, focusing on bullet maturities paying a non-zero coupon.

(c) AdvisorShares