Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

The world is changed

I feel it in the water

I feel it in the earth

I smell it in the air

Voice of Galadriel Lord Of The Rings (The Movies)

The world has changed on the 2nd of February after US Personal Income and Outlays report or maybe more importantly ISM Manufacturing Index report got released. The Global Carry trade and Dollar trade got broken and have been broken since. Is it a passing correction or the time is up and the game is over?

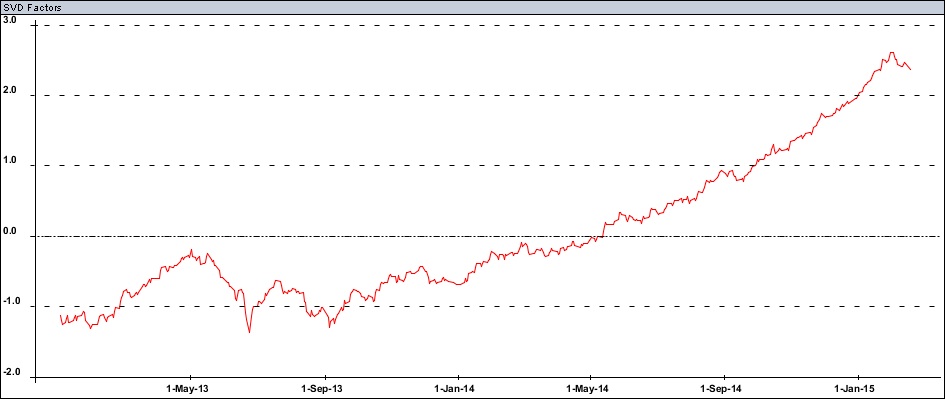

We reviewed Global Carry in details recently[1][2][3][4] so without further ado let us look how “Dollar enhanced Global Carry” factor introduced in “Global Carry gone parabolic?” behaved recently.

What you see on the l.h.s. of the chart above is the Taper Tantrum gyrations, followed by “Global Carry Rock ‘n’ Roll” days with a recent correction which started on the 2nd of February, the day the dollar crashed after US Personal Income and Outlays followed by ISM Manufacturing Index reports came out.

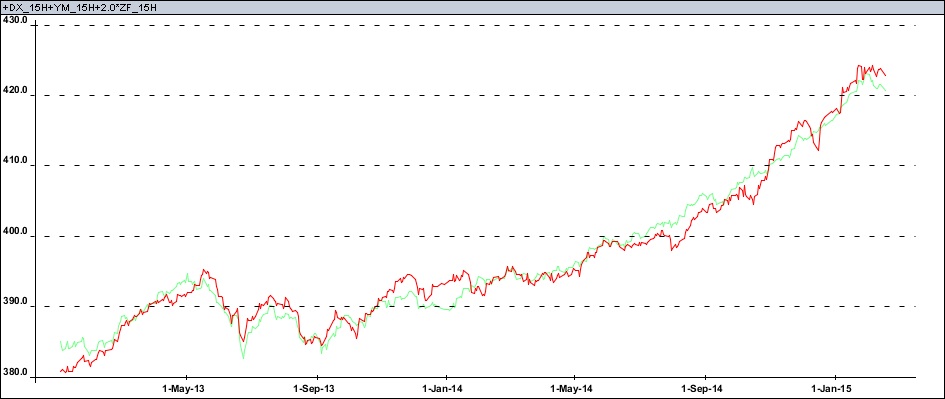

In “Global Carry gone parabolic?” we explain that this recent incarnation of Global Carry can be proxied by a simple futures portfolio of US dollar index, DJ index future and two shorter duration 5y note futures (red – portfolio, green – Global Carry Factor):

You can see the correction seen in this portfolio in December 2014 that has followed our call in “Global Carry gone parabolic?”.

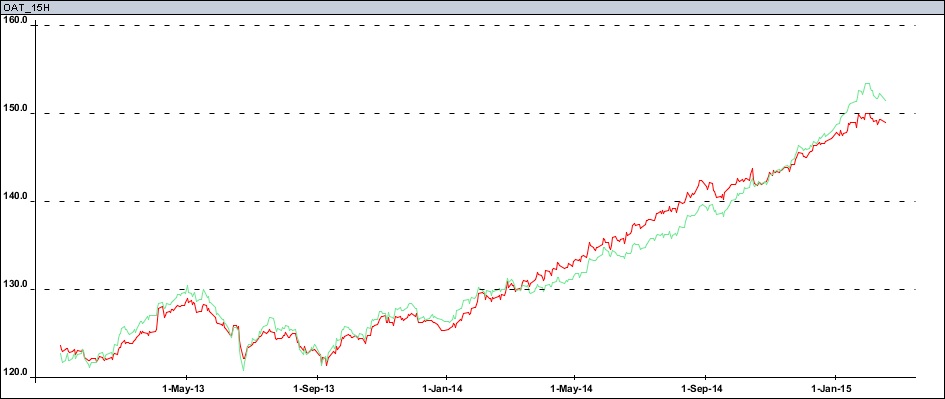

To really grasp why this “Carry” is “Global” let me introduce two other proxies:

- - 10y German Government Bond (Euro Bund, red) vs Global Carry Factor (green)

- - 10y French Government Bond (red) vs Global Carry Factor (green)

So global indeed, and let me assure you it goes far beyond and is deeply entrenched in global financial markets across all asset classes (currencies, equities and bonds).

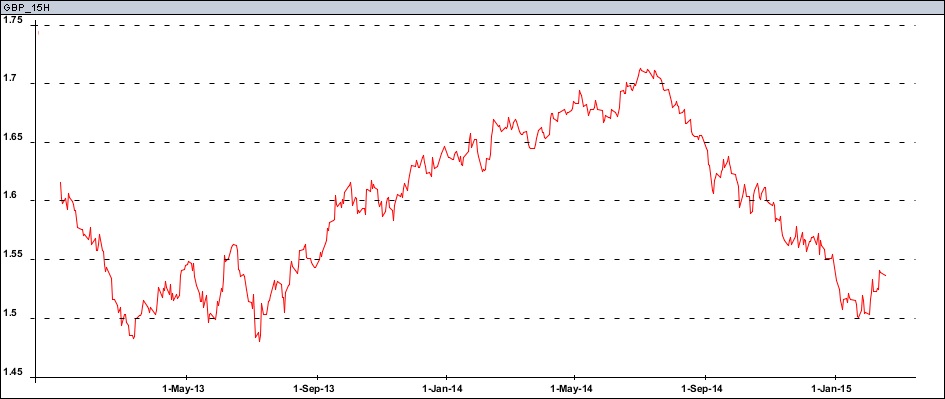

On the same day (2nd of February 2015) the dollar itself got broken. You can see it in the Dollar Index only slightly because it is essentially driven by Euro and recent Euro turmoil kept it under pressure. Also commodity currencies got their sources of headwind as well. Still dollar weakness is clearly seen in GBP for example (and likewise Gilts):

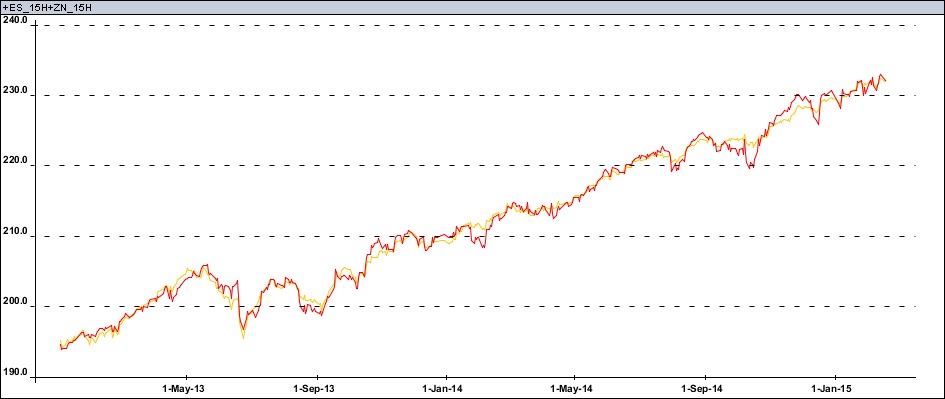

Finally what about our conventional Global Carry (SPX + 10y US note) performance?

It is not damaged yet as broken Dollar enhanced Global Carry and dollar offset each other for now. Only time will tell, but one thing is clear: this will be the year to remember.

[1] “Global Carry a.k.a. Risk Parity”, Dynamika Commentary, 16-Oct-2014

[2] “Global Carry gone parabolic?”, Dynamika Commentary, 29-Nov-2014

[3] “Global Carry is correcting”, Dynamika Commentary, 10-Dec-2014

[4] “Global Carry Rock ‘n’ Roll”, Dynamika Commentary, 3-Feb-2015