In the current environment of rising global volatility and potentially weak US corporate earnings growth, Invesco Fixed Income is cautious on US and European credit. While European investment grade credit may be supported by the European Central Bank’s (ECB) program of quantitative easing (QE), we believe US investment grade would likely underperform US Treasuries in the current environment, although we would expect it to perform better than riskier assets.

We are even more cautious on high yield and emerging markets, both sovereign and corporate, and would expect these sectors to be the most affected by the factors outlined below. That said, we believe that careful research and security selection may uncover interesting idiosyncratic ideas within these sectors.

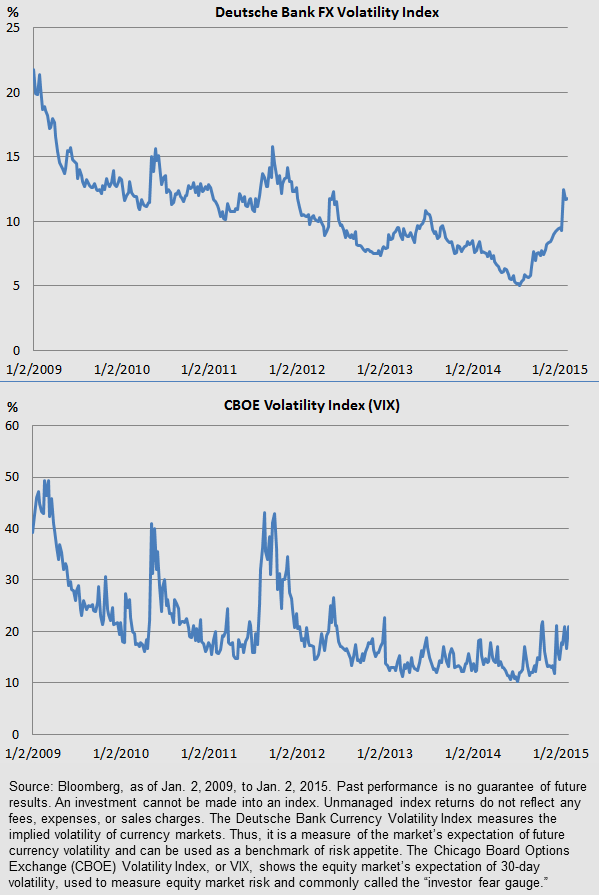

Volatility picking up

Global market volatility — which can often lead to risk aversion — is picking up. Policy surprises from a range of central banks have resulted in a doubling of currency volatility, in particular, over the past six months. But global stock markets, bond markets and commodities have also been impacted.

Heightened volatility across financial markets is not surprising considering the broad divergence in macroeconomic conditions and central bank policies around the globe. Europe and Japan are easing monetary policy aggressively as they struggle to escape stagnation, while the US is posting solid growth and preparing to tighten.

Currency and Stock Market Volatility Picking Up

Such divergence can create stresses. Currency volatility has the potential to hinder global growth by increasing the costs of global financing and trade. A sharply higher dollar, in particular, is associated with deteriorating global funding conditions and tightening liquidity, especially creating pressures among emerging markets. A sustained US dollar rally and elevated volatility further heightens the chances of a significant financial market event, as demonstrated by the recent move by the Swiss National Bank to abandon its currency cap. It is difficult to forecast exactly where the stresses will manifest themselves, but as they build, we believe the probability of an “accident” increases.

Despite greater volatility in global markets, the reaction of US stock and interest rate markets has been relatively muted. This begs the question: Will the increase in global volatility eventually spread to the US? Typically, global financial stress and weak growth have not affected the US, unless a negative financial shock occurs (for example, the failure of Long-Term Capital Management in 1998). If volatility in the US were to follow the rest of the world, our quantitative modeling work suggests that the fair value of US investment grade spreads could widen by 20 to 25 basis points. We would expect US high yield spreads to widen by five times as much, assuming the historical relationship between the two sectors holds. The bottom line: We believe global factors have some potential to hamper the performance of US credit assets.

US corporate earnings depressed

We believe company earnings are likely to disappoint based on global economic weakness, US dollar strength and declining energy earnings. An appreciation in the trade-weighted US dollar and declining commodity prices are generally negative for earnings of large US companies — the strong dollar tends to be more relevant for the investment grade universe, while lower commodity prices are pertinent to both investment grade and high yield. Given these headwinds, the probability of an earnings recession (defined as negative earnings growth), has increased, in our view.

Low oil not priced in

Finally, we believe that current market sentiment and market pricing of credit assets are building in a recovery in oil prices into the next year. Our base case assumes that oil prices will remain depressed. If the price of oil stays at its current level or declines, we will see ongoing stress. In our opinion, it may take some time for funding issues to materialize, but we would expect to see potential fallout among some corporate and sovereign issuers in coming quarters.

Conclusion

The overall environment for risky assets, and particularly for credit, is deteriorating as economic divergence and volatility picks up. We believe investors should be cautious in taking credit exposures, and that simple broad credit allocations are to be avoided in favor of more directed, idiosyncratic credit opportunities. With volatility comes opportunity, but it is more important than ever for investors to do detailed research to avoid credit accidents that are likely to come with increasing frequency in coming quarters.

Important information

Volatility measures the amount of fluctuation in the price of a security or portfolio.

Spread is the difference between investment grade (or high yield) bond yields and yields on similar-maturity US Treasury bonds.

Basis point is a unit that is equal to one one-hundredth of a percent.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

High yield bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of high yield bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

Issuers of sovereign debt or the governmental authorities that control repayment may be unable or unwilling to repay principal or interest when due, and the Fund may have limited recourse in the event of default. Without debt holder approval, some governmental debtors may be able to reschedule or restructure their debt payments or declare moratoria on payments.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.