“It [investing] is the one sphere of life and activity where victory, security and success is always to the minority and never to the majority.” –John Maynard Keynes

Dear Fellow Investor,

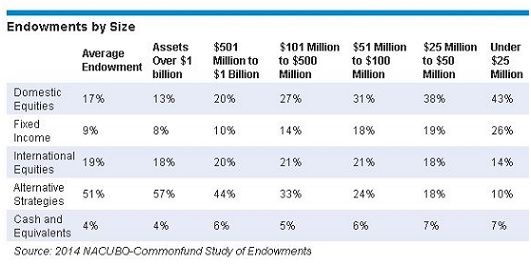

To get a good feel for where the largest pools of money are invested around the world and to identify the minority, we draw from the NACUBO-Commonfund Study of Endowments in North America. This year’s survey included $516 billion in investable assets. The results for the fiscal year ended June 30th of 2014 are listed below. Pay particular attention to the largest endowments, because we believe they represent the asset allocation of the largest worldwide institutions.

Dogs No Longer Chase Cars

Back in the 1980s, we used to say that “dogs chase cars and people chase stocks.” Domestic equities have compounded money in the S&P 500 Index at 16.56% over the last five years. Apparently, the majority of investors have not chased stocks. The average ownership of U.S. equities has dropped from 18% in 2009 to 17%, but the largest institutions have only 13% U.S. equity ownership.

Since the largest endowments had 11% ownership of U.S. equities in the 2010 survey and the S&P 500 has caused each $1 million investment to grow to $2.1472 million in that time period, we will assume that the largest institutions have been massive net liquidators of U.S. common stocks for the last five years. Therefore, maybe dogs don’t chase cars anymore. Can this bull market end without finally drawing in the largest pools of investable dollars around the world? History argues no.

What is the Alternative?

The largest endowments are heavily committed to the alternative investment space (57%). They argue that they get equity-like returns with less volatility from alternative investments, provided they do it in a diversified manner. Most of the money in alternatives sits in four areas. Those investment arenas are hedge funds, private equity (LBOs), venture capital, real estate and commodities.

What do these alternatives have in common? They benefit immensely from the historically-low interest rates precipitated by the post-financial meltdown accommodative monetary policy of the Federal Reserve Board. Three of these categories (hedge funds, private equity and real estate) borrow money directly and have seen returns enhanced constantly for thirty-four years by the bull market in bonds. A wise man once said, “Do not confuse brains with a bull market.”

Venture capital has also been indirectly and positively impacted by lower interest rates. Venture capital returns have tracked over the years with strong performance by small-cap stocks relative to large-caps. From the end of 1999 to the end of 2013, small caps (as represented by the Russell 2000 Index) stomped their larger S&P 500 brethren while interest rates fell. It makes total sense that smaller-cap companies with lower credit quality would benefit from amazingly low interest rates from banks and the junk bond market (high yield). Venture capital and private equity firms harvest their gains via the stock market and do it when riskier/newer companies have done the best.

Expense is the Enemy of Your Portfolio

We think it is interesting that the average institution and most of the large ones are the most heavily invested in the asset classes (alternatives) which are the most expensive to own. Most hedge funds, private equity firms and venture capital firms charge some type of premium fee structure compared to an active U.S. equity separate account manager, which is even greater when compared to a passive U.S. equity vehicle. It is a big price to pay to get your results out of the newspaper. God only knows how some of these things have done along the way, let alone anyone who would like to track risk-adjusted returns. CALPERS, the huge state-employee pension institution in California, recently removed the hedge fund investments from its portfolio and cited the expense as the primary reason.

Which Asset Class Puts you in the Keynesian Minority?

Experience and observation have taught us that what the largest pools of money don’t want to do has a tendency to outperform the other asset classes. We believe Keynes would agree. In the 2002 NACUBO survey, U.S. equity was 37% of the average portfolio. Since large-cap stocks had been the darling of the prior decade of the 1990s, we think it was probably more than 70% of the U.S. equity total to make it around a 26% portfolio allocation then. Since small and mid-cap U.S. equity have dramatically outperformed over the last ten years, we believe that the 17% average is no more than 60% or around 10% of large institutional portfolios and could be even lower.

Lastly, large-cap companies haven’t been the epicenter of excitement for leveraged buyout firms since the takeover of RJR Nabisco in 1988. Today’s focus has been on small and mid-cap companies. As interest rates rise, the strong balance sheets and self-financing ability of large-caps could make them be the place to be. Isn’t it ironic that these heavy-weight investors own so little of the easiest to own, most liquid and the least expensive productive asset class available?

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.