Weighing the Week Ahead: Will Energy Stocks Support the Market Breakout?

Stocks show continuing strength, testing the top of the recent trading range and making new highs. The sector rotation has favored “risk on” despite rather soft economic data. At the heart of this anomaly is the energy trade. In a holiday-shortened week, I expect markets observers to ask:

Is there a bottom in energy stocks? Will this support the overall market breakout?

Prior Theme Recap

In last week’s WTWA I predicted that the punditry (in the absence of much fresh data) would be asking whether it was time for “Risk on.” This was a very accurate call, with plenty of attention throughout the week. The general market reaction was “yes” and the traders were taking note of the decline in utilities and bonds, and the strength in oil prices and commodities.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

Last week’s trading was something of a mystery. The “risk on” question got a definite “yes” with an increase in stocks and cyclical sectors combined with selling in bonds and defensive stocks like utilities. This happened despite rather soft economic news.

While there is a fairly normal economic calendar, I expect the punditry to focus instead on the new record in stocks. In particular, most will be asking:

Can Energy Stocks Support the Market Breakout?

Background

Over the last two months I have carefully raised and explored the “message” from various markets.

- Oil Prices (12/13/14)

- The bond market (1/11/15)

- Earnings (1/18/15)

- Europe (1/25/15)

- Risk On? (2/8/15)

These themes all gave due respect to the approach of seeking a “message from the market.” This is a favorite for most traders and pundits, but it often serves to explain the past. Few seem to find predictive edge from this approach, although it sounds good on TV.

The alternative is to use economic data and corporate earnings to discover where markets may not be efficient. This helps to identify sectors and stocks that are mispriced. My own approach is to emphasize economic data to predict markets, as I explained in my 2015 Annual Preview. Last week the thesis seemed wrong, but the result was a winner. The jury is still out for this year, but it is a subject of continuing interest.

The Viewpoints

There is a wide range of opinion on the prospects for oil prices and energy stocks. Here are the main contenders:

- Energy stocks have not bottomed. Citi warns to look out for a “20 handle” on crude oil!

- Crude oil supply and demand are not that far out of balance, and the gap is closing. (Barron’s cover story has this and contra viewpoints, stock ideas, MLP’s). FT on falling rig counts.

- Technicals say “no.” Cam Hui digs deep, including this chart:

As always, I have some additional ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good news last week.

- Progress in Greece. While some will see the emerging agreement as temporary and merely delaying matters, this type of negotiated solution is actually quite typical. Each side does as little as possible. There is an opportunity for face-saving. The worst crisis outcome is averted. The best case is that the time will be used constructively, while the worst case implies revisiting the issue. Markets seemed less worried about Greece this time, but the progress was a small positive.

- Eurozone GDP was positive and slightly higher than expectations at 0.3%.

-

Earnings reports have been positive. It may not seem like it, but 78% of reporting S&P companies have beaten on earnings and 58% on sales. (FactSet). Some readers have accurately objected that these results reflect success against lowered expectations. FactSet reports that 80% of companies are reporting a negative outlook and that Q1 forward earnings have been cut more than any time since 2009. The question right now is whether estimates have fallen enough, and apparently they have. The earnings context has been very negative, and WTWA emphasizes the fresh news. That has been more encouraging of late. Brian Gilmartin continues his more upbeat take, writing as follows:

The SP 500 is growing earnings on an operating basis, about 6.5% – 9.5% per year, the last few years, and I expect that to continue through calendar 2015.

q1 ’15 earnings growth is currently expected to be -2%, including Energy’s drag of a whopping -62%, so excluding that drag, the SP 500 earnings growth on an operating basis is expected at +4.4%

Full-year 2015 earnings growth is expected at +2.4%, so excluding Energy’s drag of 53%, growth on an Ex-Energy basis is roughly +7.5%.

- Ukraine cease fire. I am scoring the cease fire as a positive. It was better than nothing and I give deference to the market reaction. With that in mind, the initial response from combatants was to increase hostilities. Few serious analysts have great hope for rapid progress. For investors, we are not even close to the reduction in reciprocal sanctions – the factor that would stimulate European growth and worldwide equity markets. Issues via Brookings.

The Bad

The bad news included some significant economic reports.

- West Coast port strike continues – a slowdown and a lockout.

- Weekly jobless claims climbed. The 304K was a disappointing shift from the last two weeks.

- Michigan Consumer Sentiment fell to 93.6, dropping from 98.1 and missing expectations. The chart from Doug Short is the best, showing why this series is an important economic read.

- Farmland values are falling in the Midwest – for the first time in decades. Strong crops – lower prices. (Jesse Newman WSJ).

- Retail Sales missed badly, even when you massage to exclude gasoline sales and include other adjustments. Steven Hansen at GEI has the analysis. (Scott Grannis has the bright side). Calculated Risk calls the result “OK” and provides this chart:

The Ugly

The human cost in Ukraine continues as fighting rages. (WSJ).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are welcome. I am seeing plenty of bad charts, but little refutation.

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s Big Four summary of key indicators.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. Georg continues to develop new tools for market analysis and timing. Some investors will be interested in his recommendations for dynamic asset allocation of Vanguard funds and TIAA-CREF asset allocation. He has added a method for Vanguard Dividend Growth Funds. I am following his results and methods with great interest. You should, too. This week Georg updates his Business Cycle Index, which made another new high.

Cullen Roche takes a look at the misery index, now at an eight-year low. He even checks out how it would score using Shadow Stat’s “phony inflation” approach.

The Week Ahead

It is a normal week for economic data.

The “A List” includes the following:

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Housing starts and building permits (W). Permits provide a good sense of future construction.

- Leading indicators (Th). Still seen by many as a good recession warning.

The “B List” includes the following:

- FOMC minutes (W). Pundits will squeeze hard to find some new information.

- PPI (W). Still not important with overall inflation so low. Someday, but not yet.

- Industrial production (W). Volatile series is difficult to predict, but still important.

- Crude oil inventories (Th). Maintains recent interest and importance.

There is plenty of FedSpeak. Important corporate earnings continue, although the season is winding down. There are regional Fed reports, but these are usually not important.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

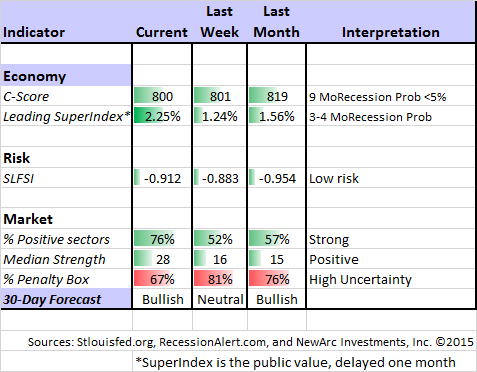

Felix has moved to a “bullish” posture for the three-week market forecast, but it continues to be a close call. The data have improved a bit, but are only slight better than the recent neutral readings. There is still plenty of uncertainty reflected by the high percentage of sectors in the penalty box. Our current position is still fully invested in three leading sectors, and we have gotten more aggressive. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com.

As I have noted for five weeks, Felix continues to feature selected energy holdings. Felix is not just a momentum trader!

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a new page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

My bold and contrarian prediction for 2015 – that the leading sectors would lose and the laggards would win – looked a lot better over the last two weeks. If I am correct, there is a very, very long way to run for the cheapest market sectors – energy, technology, cyclicals, and financials.

Other Advice

Here is our collection of great investor advice for this week:

Stock and Sector Ideas

Growth and value ideas converging? Bill Nygren of Oakmark explains and also has some ideas, including GOOG, MA, and WFM. More value plays with dividends from Dennis Ruhl of JP Morgan (via Barron’s).

“Safe” energy plays. “Aggressive” plays. (Both from Barron’s).

Tim Melvin shows why liquidity is over-rated for the individual investor. Regular readers know that I like his theme of regional bank stocks.

Bill Miller likes AMZN, AAPL and BABA.

Watch out for falling REITs.

Market Outlook

Michael Batnick revisits the listing of things people used to worry about instead of buying stocks. Enjoy his list of these golden oldies (the 1929 chart?) as well as this distribution of market returns over the last 89 years.

Ben Carlson shows that rising interest rates are consistent with higher stock prices, using the table (below) of average annual returns. I explained the reason for this in 2010, charting the curvilinear relationship between interest rates and stocks. Basically, extremely low rates are associated with intense skepticism about earnings and the economy. The move to normalize rates is positive for stocks.

The “fighting the Fed” part does not start for years. Sam Ro has the data:

Final Thought

I do not know whether we have reached a bottom in energy prices, but I have identified two important themes.

First, low US interest rates reflect a crowded leveraged trade. European bonds (for a change) represent the funding currency and US bonds the source of return. The interest rate margin is only about 1%, but the trade may be leveraged at 15-1. The currency risk in these trades is often hedge, but I suspect that many funds are “going commando” by relying on dollar strength.

This trade is vulnerable to a weaker dollar or to rising US interest rates. If either or both of these occur, long-term rates could rise rapidly as the trade is unwound.

Second, some hedge funds are investing in distressed bonds of energy companies and hedging by shorting the stocks. This puts continuing pressure on stocks, while providing a bit of support in the debt market. The hedge ratio is theoretical, since these are not convertible bonds. A significant increase in the stock prices could lead to short covering as the trade is unwound. This is difficult to measure and to play, but watching short interest in energy stocks is one idea. Bespoke charts it (via BI).

Risk and Reward

There is enough strength in the rest of the market that leadership from energy is not necessary for good returns. I want to reemphasize last week’s final thought. What is often thought of as safe has become risky.

Risk. Many investors wisely begin by thinking about risk. That is how I start each interview with a potential client. Everyone has the need to protect a portion of the investment portfolio, with the assurance that any losses will be modest.

It is not always easy to identify safety. Last year’s most successful investments were bonds and bond proxies. The quest for safe yield has become a crowded trade. Those celebrating the success of bond mutual funds and their utility payouts should look at this week’s results. It is a very small taste of what will happen when interest rates return to more normal levels.

Reward. And we all need some investment reward, either to keep pace with inflation or to increase the retirement nest egg. There is excessive focus on arguments about the overall market valuation. There are plenty of cheap stocks and sectors.

Financials, technology, and consumer discretionary are all attractive and cheap.

(c) New Arc Investments