"90% of what passes for brilliance or

incompetence in investing is the ebb

and flow of investment style.”

- Jeremy Grantham1

As investment boards and committees gather to discuss performance for 2014, eyebrows will most certainly be raised as people review the performance of many of their equity managers. Depending on which database they are looking at, between 80% and 90% of active U.S. equity managers will have underperformed their benchmark this year, making it one of the worst years for active management in the recent past. Those particularly prone to hyperbole will use this as a clarion call to further embrace passive management and rid themselves of their active managers. After all, if only 1 in 10 active managers can actually generate alpha, why would investors bother with the time, headache, or cost of active managers? Not so fast ...

It is incredibly important to avoid extrapolating short-term results. Just because active management in general has been through a difficult period, it does not necessarily follow that what is past is prologue. In today’s increasingly short-term-oriented investment culture, winning stock pickers are deemed to have exhibited superior foresight and brilliance while the losers have suddenly become idiots and are often shown the door. Reality is something quite different. In any given year, there can be a substantial amount of luck involved in outperforming a benchmark. Over a longer horizon, we think it is easier to make the determination between skill and luck. As investors find themselves asking questions about their active managers given their recent poor performance, we believe we have some insight as to what may be driving some of the headlines lamenting that performance.

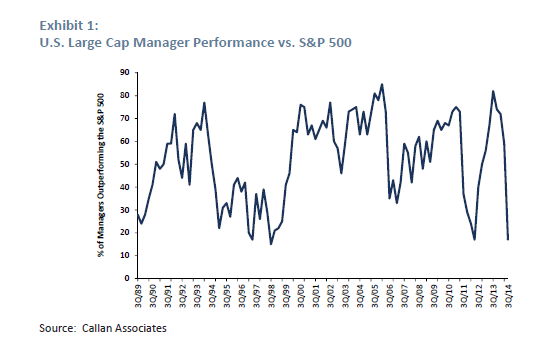

U.S. Large Cap Manager Performance

The past year has proven to be a very challenging period for U.S. equity managers. At the end of the third quarter of 2014 only 17% of large cap managers’ returns had met or exceeded those of the S&P 500 over the prior 12 months (see Exhibit 1). It shows that the recent underperformance is not an unprecedented occurrence, but it is not terribly common either.

If investment managers were each following independent investment strategies, we would expect roughly half of these managers to outperform (gross of fees) in any given period. The data, however, suggests that it is far more typical for either two-thirds of managers to outperform, or for two-thirds of managers to underperform. Almost everyone wins, or almost everyone loses. This strongly suggests that there are some common factors that drive the performance of the typical manager and that these factors ultimately heavily influence their success or failure.

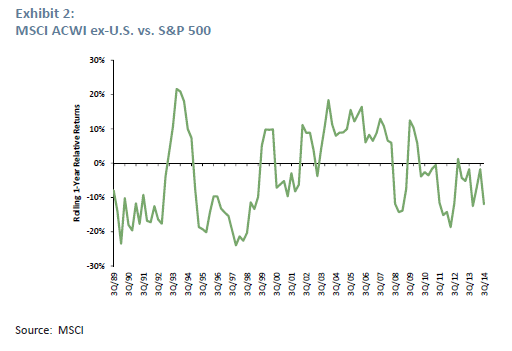

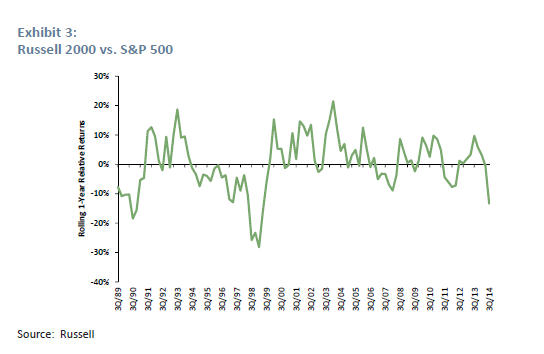

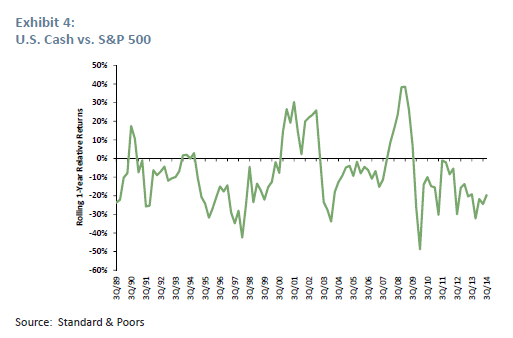

Because the data is broadly representative of the universe of institutional U.S. large cap equity managers, the explanatory factors are not likely to be found in the form of sector biases, value versus growth, or anything else that amounts to taking active positions within the benchmark. After all, for every active manager that is overweight a sector there is another who is underweight. Rather, the explanation must come from some systematic exposures that are taken by the majority of managers that amount to out-of benchmark allocations. To keep things as simple as possible, we will focus here on investments in non-U.S. stocks, investments in small cap stocks, and cash holdings. Using the MSCI ACWI ex-U.S. index, Russell 2000 index, and 3-month T-bills as proxies for each of these asset classes, we have plotted the relative performance of these out-of-benchmark allocations versus the S&P 500 in Exhibits 2 through 4.

It is not uncommon for managers to have several percentage points of their portfolio allocated to each of these asset classes, and therefore underperformance from any of these will act as a drag on the performance of the overall portfolio. To get a sense of the magnitudes involved, we can see from the exhibits that in the 12 months ending September 30, 2014 the S&P 500 beat both international and U.S. small cap stocks by around 10% while outperforming cash by 20%. If a manager were to have had 5% of his portfolio in non-U.S. stocks, 5% in small/mid cap U.S. stocks, and carried 1% in cash, thenhe will have effectively started with a deficit of 120 bps versus the benchmark. That is a lot of ground to make up from stock picking within the S&P 500 alone.

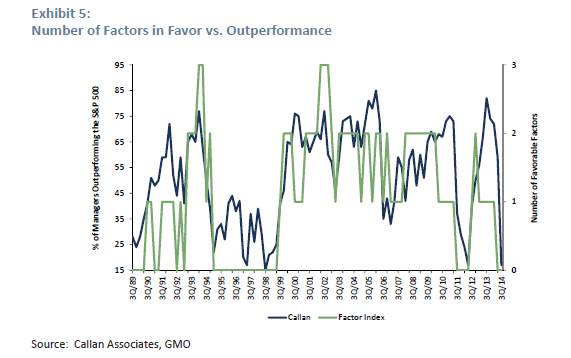

To help understand the longer-term influence of these out-of-benchmark allocations on overall manager performance, we constructed a very simple index that counts the number of our style factors that have been helping managers at any point in time. This is plotted in green in Exhibit 5. The minimum score is zero when all three factors underperform the S&P 500, and the maximum score is three. In Exhibit 5 we have overlayed this index with data representing manager outperformance. While relatively rare, periods in which all three factors were working against managers were trying periods indeed. The most recent bout of manager underperformance coincides with all three factors losing to the S&P 500, as do previous periods of extreme underperformance in 2011-12 and 1995-99.

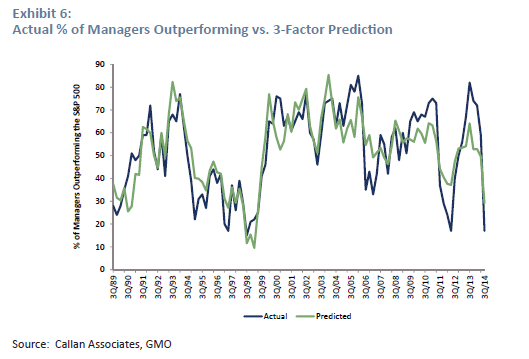

In fact, we can do somewhat better and attempt to “explain” the data. To that end we have set up a simple three-factor model in which we regress the performance data for U.S. large cap managers as plotted in Exhibit 1 against the contemporaneous rolling 12-month returns of each factor as plotted in Exhibits 2 through 4. Using the results of this regression, we can estimate the percentage of managers that would be expected to outperform at each point in time given only the relative performance of our three factors. The predicted and actual data are overlayed in Exhibit 6. The conclusion to be drawn is that a very large proportion of the historical variability of large cap managers’ ability to add alpha is explained by our simple three-factor out-of-benchmark model.2

To Fire or Not to Fire?

As you look across your roster of equity managers, there will be a myriad of explanations as to the reasons for poor performance. Some of those explanations will be valid and others will sound much more, um, creative. But for active management as a whole, 2014 was a year when the forces in our three-factor model were aligned in such a way as to make it an especially difficult environment for active managers to outperform. U.S. equities trounced non-U.S. equities, large cap stocks trounced small cap stocks, and equities trounced cash. That was a lot of trouncing going on. And, sure enough, active management was trounced. But you cannot let the results of 2014 dictate the outcome of any debate on the merits of active investing versus passive investing. Extrapolating a short-term trend into the future can be a very difficult way to compound wealth. There are merits to passive investing. But there are also merits to active investing. Active management allows for the continuous assessment of the state of the market and to make intentional choices about how best to take advantage of opportunities and mitigate risk. Passive management precludes the ability to add value in this way. If you did appropriate due diligence and the people, philosophy, and process of your investment manager has not changed, the short-term pain you are feeling may simply be due to the ebb and flow of style. Reacting to the short-term pain of underperformance and locking in a loss may feel good but can be very costly. It is unlikely that 2015 will result in the same performance for active managers as 2014. It is certainly possible, but we think it is unlikely. Investors are much better served by focusing on their investment philosophy and process than by responding to short-term results and headlines.

1 “Everything I Know About the Market in 15 Minutes,” various speeches.

2 The coefficients of the regression are significant at the 5% level and the adjusted R^2 is 70%.

The authors would like to thank Sam Wilderman for his early work on this subject as well as Yifei Shea for the quantitative work involved in this presentation. We would also like to thank our colleagues at GMO for all of the thoughtful suggestions for this paper.

Disclaimer: The views expressed are the views of Neil Constable and Matt Kadnar through the period ending February 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

© GMO