SUMMARY

- We think that investors should prepare for a more volatile fixed-income market in 2015 with the Federal Reserve expected to raise short-term interest rates.

- Despite the potential for increasing price gaps, we think investors should recognize that volatility will also likely bring value back to the credit markets.

- A credit-focused multisector approach to investing may help find opportunity in fixed-income markets during times of increased volatility.

What will the bond market bring in 2015? Our outlook can be summed up in two words: Volatility and opportunity. For investors seeking attractive income, it’s important to understand that opportunities will likely not come without price volatility in 2015. The biggest challenge for investors is how they react to the volatility and increased price gaps that may arise as markets normalize. Indeed, keeping volatility in perspective may be more important than ever.

In this Insight, we discuss our outlook for fixed-income markets in 2015, explaining why a rate hike from the Federal Reserve (Fed) could potentially spur volatility. We also discuss how a multisector approach to bond investing may help income-seeking investors turn this volatility into opportunity for patient investors.

2015: A year of transition

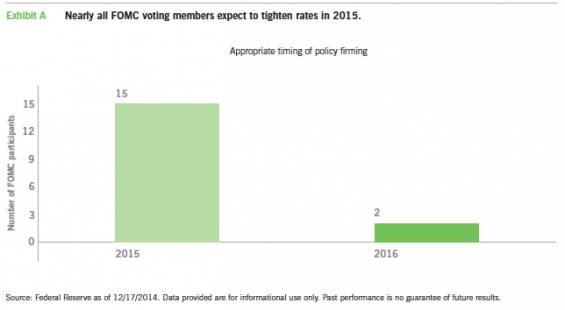

After six years of near-zero short-term interest rates, it appears that the Fed is poised to increase the fed funds rate sometime in 2015 (Exhibit A). Although inflation still remains below the Fed’s 2% target, the U.S. economy continues to strengthen and has diverged from other developed markets. If these trends continue, we think the Fed will likely hold to its plan to raise rates around midyear.

It is our view that markets are now transitioning from the end of the Fed’s bond-buying program (known as quantitative easing, or QE) to the beginning of the Fed’s tightening cycle. To put this in perspective, the last time the Fed embarked on a rate-tightening cycle was June 30, 2004 – more than a decade ago. As this transition continues, we think the markets’ technical conditions will become less favorable and the potential for volatility in fixed-income markets will likely increase.

The return of (normal) volatility

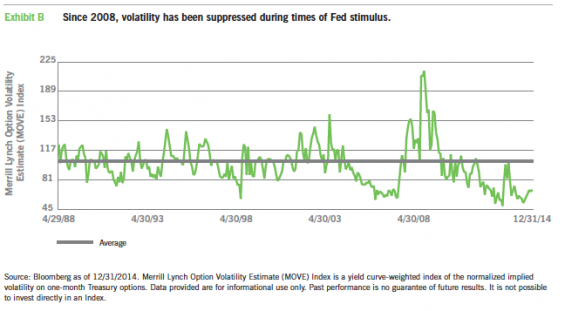

Since the financial crisis of 2008, the Fed’s extraordinary actions intentionally tamped down on volatility; we like to say that volatility has been in a Fed-induced coma over the past several years (Exhibit B). With the Fed expanding its balance sheet and providing greater transparency in its communications, many investors were not concerned about an unexpected change in the Fed’s policies. As a result, investors moved further out on the risk spectrum in a quest for yield and liquidity premiums declined sharply.

The massive volume of funds flowing into traditionally volatile asset classes over the past several years may have helped set the stage for a technical correction. As investors have sought alternatives to the low yields on U.S. Treasurys, we think that many investors did not receive a wide enough spread over U.S. Treasurys to justify the risk. And with liquidity premiums now likely to increase, those spreads appear to us to be too narrow.

The pendulum is now swinging to a less-liquid market as a result of the Fed ending its monthly asset purchases and preparing to tighten short-term rates. Historically, during periods of restricted liquidity, volatility tends to pick up. Some of the increased volatility we have witnessed recently has been fundamentally driven, such as the sharp decline in oil prices in the final months of 2014. But we have also observed instances where lower liquidity has intensified spread moves, causing markets to overshoot to the upside and downside.

Mind the (price) gaps

While the Fed is confident that the domestic economy is strong enough to withstand a reduction in liquidity, the effect will likely be greater “price gaps” when individual markets move up and down. As volatility picks up, part of that increase is recognized in price by an increase in liquidity premiums.

As part of the market’s transition, the variation of price may come much quicker than many investors expect, which could result in these price gaps. During times of increased volatility, bid-offer gaps have historically widened, making it structurally expensive for investors to trade. Trades can also be subject to slippage, or the difference between an expected price of a trade and the actual price at execution, during times of heightened volatility.

To be sure, we do not anticipate anything on the order of magnitude of the 2008 financial crisis. We expect that markets will be bumpy as this transition plays out, but we do not equate it to another financial crisis. Indeed, the U.S. government has taken structural steps to try to prevent a 2008-like event from happening.

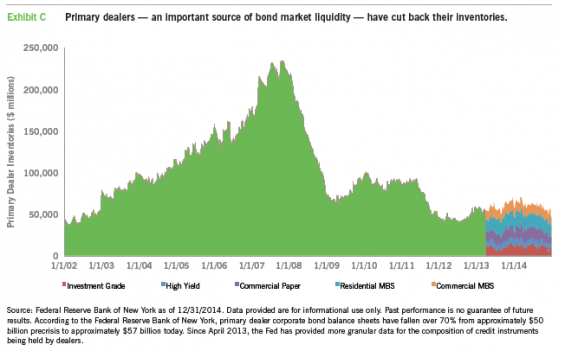

These changes in regulation have created some uncertainty for investors with regard to potential volatility in fixed-income markets. The overall goal of seeking to reduce systemic risk in financial markets – specifically to shore-up capital at the largest banks – has led to reductions in dealer inventory of fixed-income positions (Exhibit C), which has historically acted as a shock absorber during periods of volatility. In short, lowering systemic risk has heightened the potential price volatility for individual investors.

Why investors shouldn’t panic

For many investors, volatility is a euphemism for “losing money.” To us, increased volatility is simply a product of the market transitioning to a new reality and often creates opportunities. Rather than an environment where monetary policy drives markets, investors will need to adapt to an environment where fundamentals are once again in the driver’s seat.

While volatility may be higher than what investors have become accustomed to over the past several years, we view it as return to a more normal level of volatility. We also believe it’s important for investors to understand that price volatility does not always correlate with changes in the quality of an asset.

The good news is that increased volatility may bring value back to the markets, presenting several attractive opportunities for patient investors. We have already seen evidence of this in some of the higher-yielding sectors of the credit markets after recent volatility. For those searching for income opportunities in 2015, volatility may be unavoidable. But there may be ways for investors to both manage volatility and capitalize on it.

- Take a long-term approach. For investors who take a buy-and-hold approach in fixed income, one way to lower the effect of volatility is to simply stay the course.

- Put cash to work. As mentioned, investors will be subject to price gaps during periods of increase volatility. In these situations, buyers may hold an advantage over sellers.

- Avoid selling when volatility increases. As we have noted, slippage can be costly, particularly so when volatility picks up. Less-liquid investments will be particularly vulnerable to slippage when volatility spikes higher.

Consider a professionally managed multisector approach to bond investing

We think that multisector strategies are designed well to take advantage of opportunities that present themselves during periods of heightened volatility. Multisector strategies seek value across the corporate capital structure, including high-yield debt, floating-rate loans, convertible bonds or preferred stock. Multisector strategies can also look to opportunities outside the U.S., including sovereign and corporate debt in developed and emerging markets, as well as currencies.

In our multisector approach to investing, we take a contrarian perspective, recognizing that less clarity in the market means fewer clear signals for investors. In these instances, particularly during times of increased volatility, we seek to take advantage of the undervalued opportunities this uncertainty presents.

A hallmark of our multisector bond approach is taking a longer-term view in order to take advantage of short-term dislocations. Over the course of the cycle, we think that investors seeking above-average returns should consider maintaining a long-term view and be willing to incur the above-average level of volatility. The challenge will be in finding good long-term value, on a company-by-company basis.

Finding these value opportunities in periods of increased volatility and short-term market dislocations requires experience and proper expertise. Unlike investing broadly in one or more sectors, the performance of a multisector strategy is much more likely to reflect the bond-picking skill and expertise of the manager, and may vary significantly from broad bond market benchmarks, like the Barclays U.S. Aggregate Bond Index.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. As interest rates rise, the value of certain income investments is likely to decline. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, except U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors.

The views expressed in this Insight are those of Kathleen Gaffney and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com.