Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

- R. R. Tolkien, The Lord of the Rings

We review how the U.S. growth and inflation relate to that of G7 over the last forty years and conclude that not only the decoupling incidents are nothing more than temporary deviations seen as noise in the long run but also that U.S. has actually just recoupled.

OECD has just updated (with December data) their Main Economic Indicators (MEI) dataset a couple of days ago and it is worth revisiting where we stand in terms of G7 (United States, Japan, Germany, France, Italy, Canada and United Kingdom) real growth and inflation. We use G7 because it allows us to look back at least forty years while dataset for emerging markets is not that far reaching unfortunately.

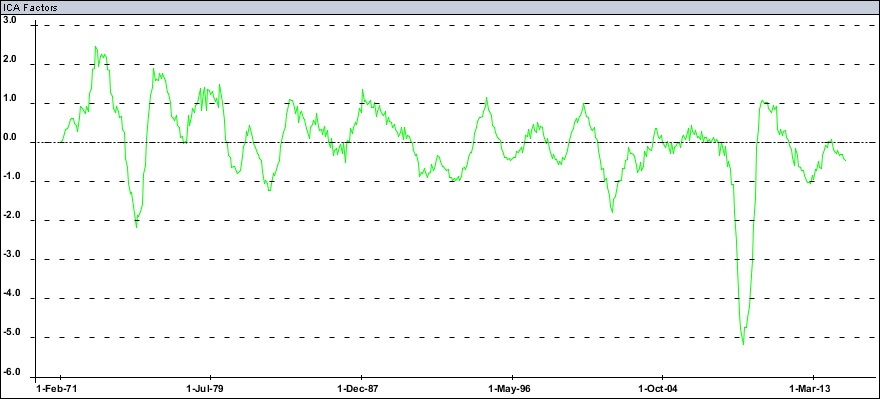

And without further ado, I would like to introduce you to G7 real growth (green) and inflation (red) factors. Please note that scaling of Y-axis on all chart is meaningless (factors are scaled to unit variance) so only relative value of factors is important, i.e. look at the chart but not at the Y-axis.

Nothing surprising here: deceleration in real growth and inflation. Does the U.S. show different trajectory?

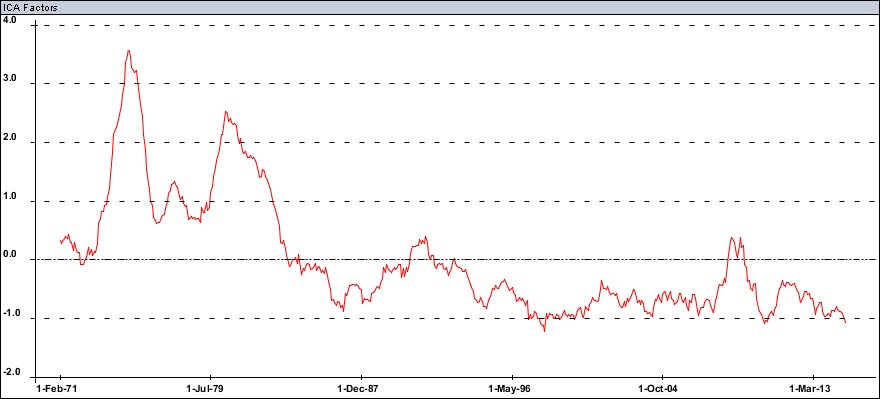

Here is the U.S. real growth factor (red) vs G7 real growth factor (green). As you can the RE-coupling just happened!

Also though there are some dislocations to both sides in the U.S. vs G7 growth series above (and recently indeed) in the long run it all really appears as nothing but the mean reverting noise. Similar story is there for the U.S. inflation.

One note on methodology: for each country we look at large set of economic series and extract inflation and real growth factors. Further we look at joint factors for pairs of factors for each country.

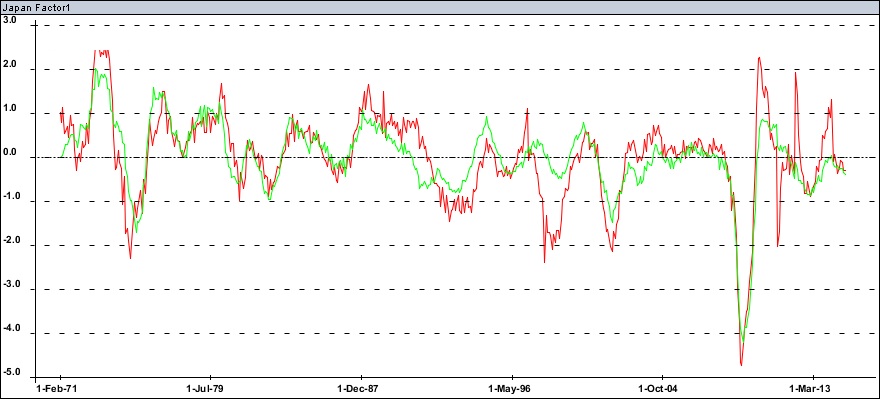

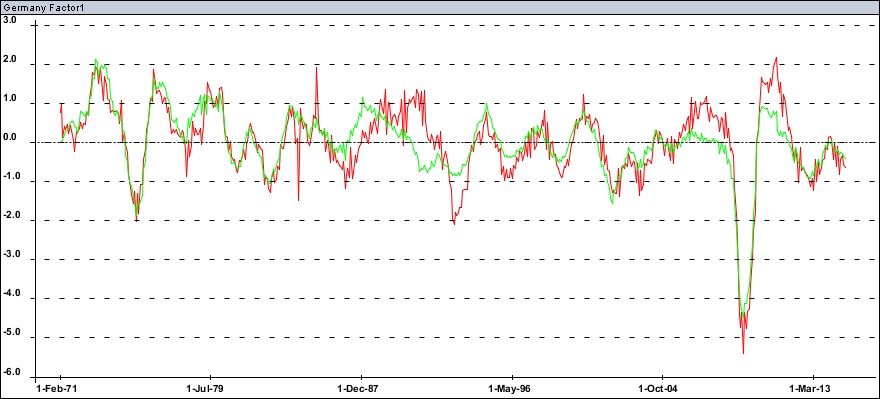

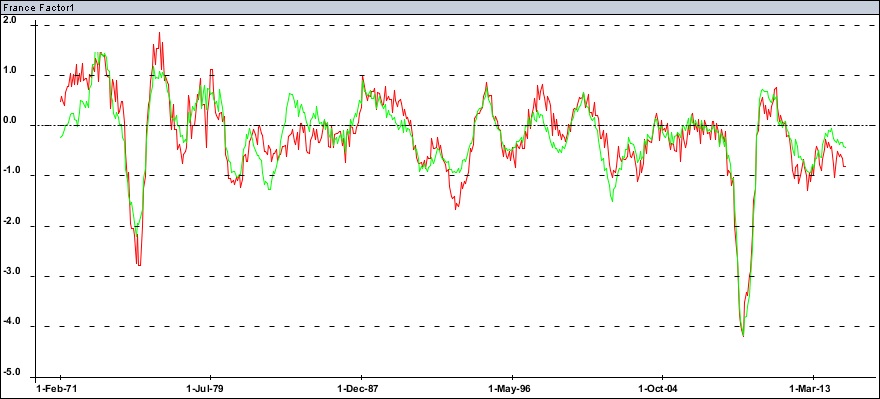

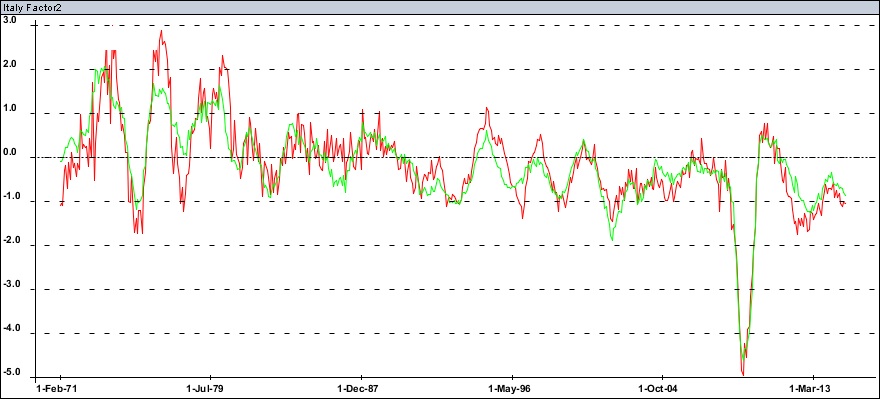

For completeness let us review real growth factors for the rest of the G7.

Japan:

Germany:

France:

Italy:

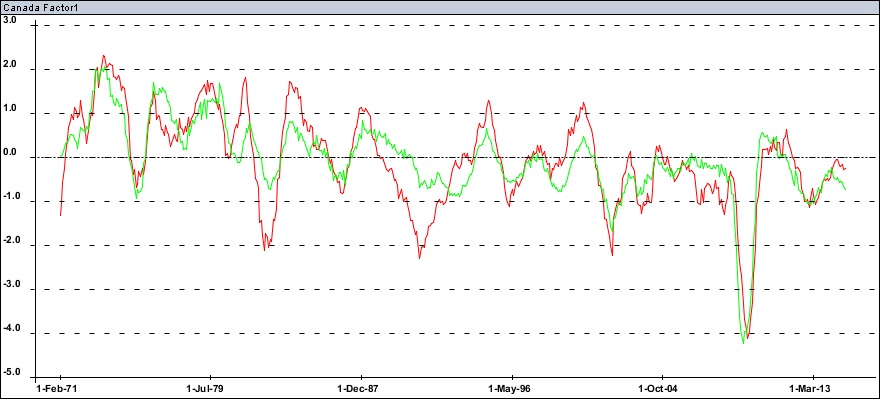

Canada:

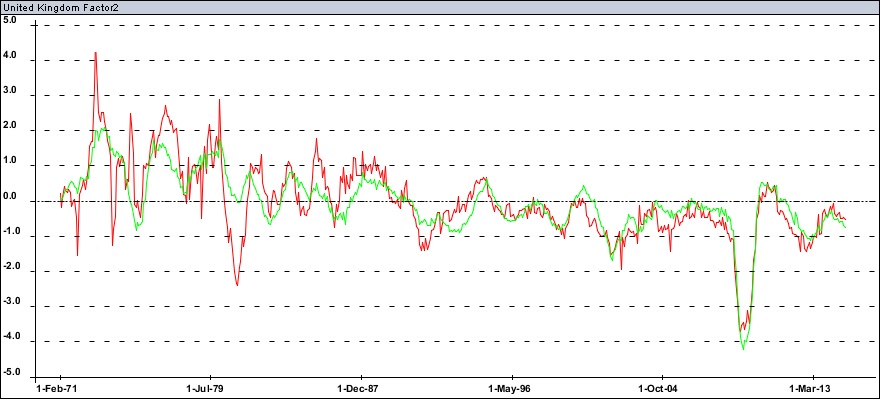

United Kingdom:

Completely similar story holds for inflation.

One note of caution: the U.S. inflation appears to have dipped more recently than for the others in G7 somehow which makes the U.S. real growth appear higher than it really is in recent economic data.

www.dynamikacapital.com/subscribe

© Dynamika Capital L.L.C.