Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

Global Carry (known as Risk Parity to some) got a bit of a headwind in December (as we proclaimed it to do on Black Friday) but went straight back to Rock ‘n’ Roll as this year started, good to great. And while the other utterly famous star – the Yen is patiently await, shocked and subdued by her competitor act, all the eyes are on the King of Rock – the Dollar. Some still have his last year stellar performance tune on the mind, but is he about to sing “The times they are a changin’”?

There are three major drivers of global assets (in order of importance):

- - the Global Carry factor (a.k.a. Risk Parity)[1]

- - the Yen factor

- - the Dollar factor

These three factors are responsible for the majority of variance and directional moves of the liquid financial assets and are the key drivers of performance of equity and bond markets.

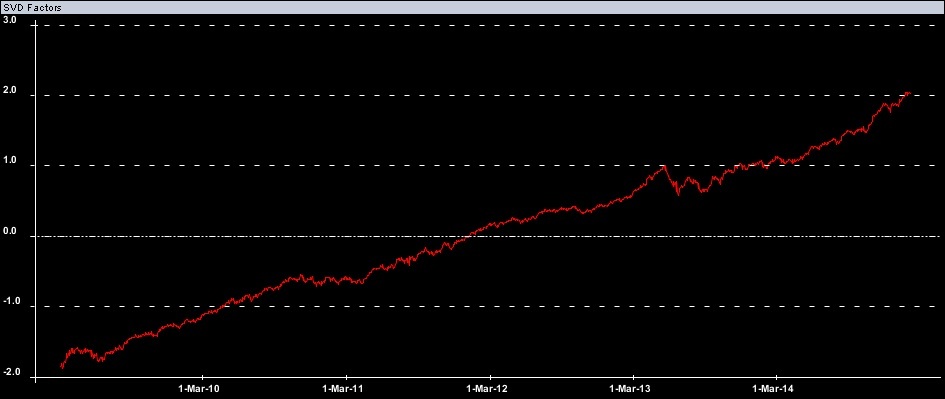

Global Carry performance since March 2009 is nothing but stellar (especially given it down to earth simplicity):

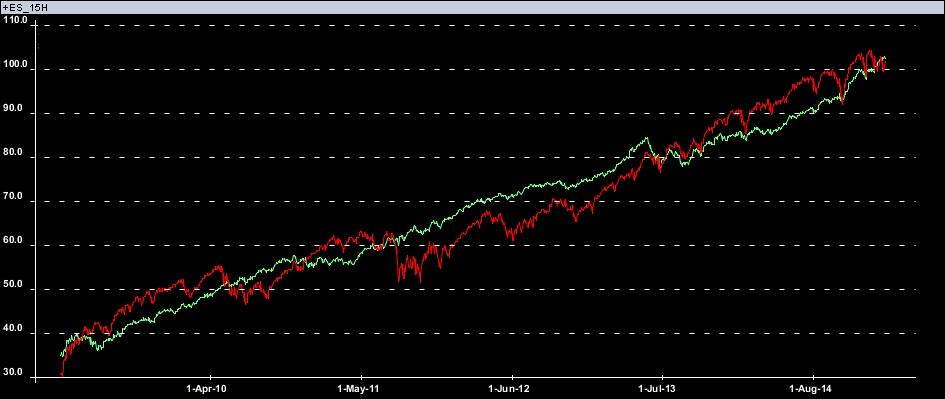

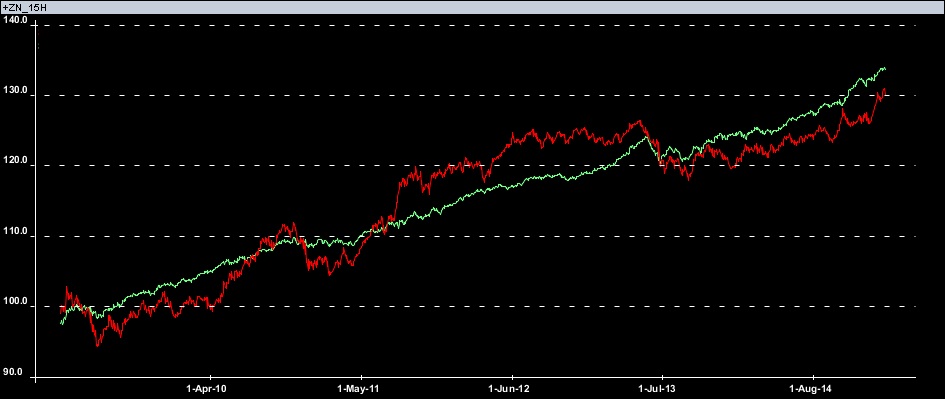

Here is how the Global Carry factor performance compares with that of SPX and US 10y Note (the Global Carry is depicted in salad color):

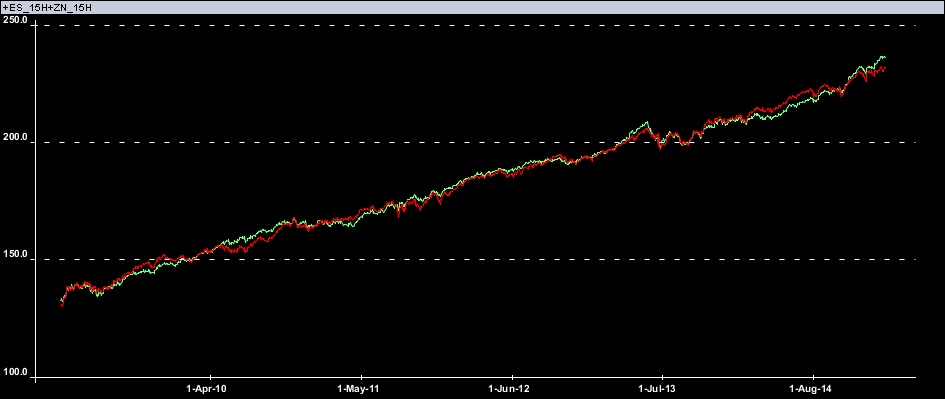

But when you aggregate simple portfolio of SPX and 10y Note above (hence Risk Parity) you get wonderful Global Carry performance tracking (red is portfolio):

Note that the recent underperformance of this simple tracking portfolio (SPX + 10y Note, red) in comparison with the Global Carry factor (salad) is due to the dollar pick up. Though strong dollar helps US bonds performance, it hurts US equities performance more. Nonetheless, it is a great proxy.

The reason why we called it Global Carry is simple: this factor propagates well beyond its simple Risk Parity incarnation presented above and is found as part of the driving force behind most of global liquid financial assets performance.

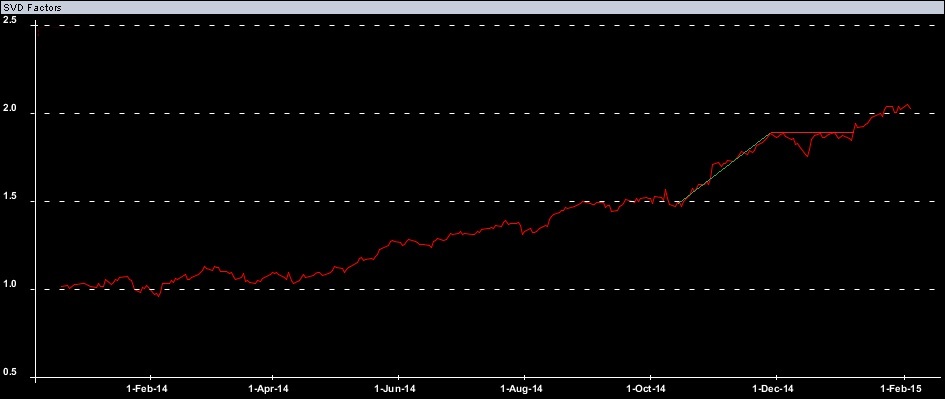

Zoom in on its performance since the beginning of 2014:

We highlighted October/November run up (green) and December correction and stagnation (red) which we called at the end of November on Black Friday.[2][3] This correction was pretty clear in the December performance numbers of the commercial Risk Parity providers.

But while the Global Carry is back to Rock ‘n’ Roll, it is the other global factor that captures our attention this time. Before we go to the dollar though let us quickly revisit the Yen factor. Japanese Yen performance is substantially driven by the Global Carry factor of course as the Yen is carry currency and this factors depreciates it. Besides that the Yen is factor on its own (which might be proxied by Yen corrected by the Global Carry factor):

Of course the periods of central bank Yen strength control are especially clear in the Yen factor above (horizontal red lines). Not much directional action recently though as the Dollar factor took the stage.

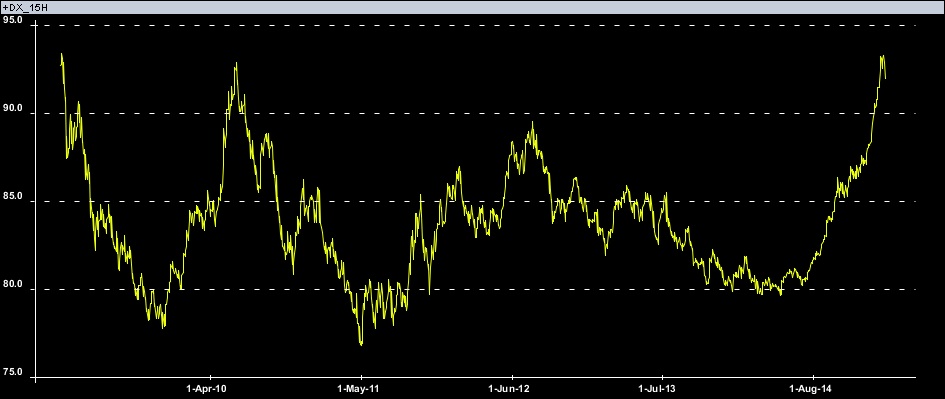

So here is the Dollar factor (note that this is not Dollar index as Dollar index is exposed to Global Carry and Yen factors but it rather close to it):

March 2009 and June 2010 peaks are not the ones to ignore and we were at this level all last week. Ready for a dive? Not claiming one to happen but risk managing dollar factor exposure is of the paramount importance right now.

The dollar crash today (3-Feb-2015) is practically the sole reason why equities, interest rates and oil rallied. How much of the dollar factor exposure do YOU have?

www.dynamikacapital.com/subscribe

© Dynamika Capital L.L.C.

[1] “Global Carry a.k.a. Risk Parity”, Dynamika Commentary, 16-Oct-2014

[2] “Global Carry gone parabolic?”, Dynamika Commentary, 29-Nov-2014

[3] “Global Carry is correcting”, Dynamika Commentary, 10-Dec-2014