Lower for Longer

· U.S. Dollar (USD) strength will support low rate environment

· More signs of global economic weakness

· Investors waiting for higher rates likely to be disappointed

· Municipal market positioned to benefit

Pick your poison: weaker oil and copper prices; increasing gold demand; Swiss Franc and Canadian Dollar devaluations; another possible Greek tragedy; launch of European Central Bank (“ECB”) bond buying program; waning emerging markets; weakening U.S. stock prices; global deflation worries.

Barely one month into 2015 and the ECB has finally unveiled its long-anticipated quantitative easing (QE) program, which will commence in March. Recognizing the need to act in a big way, the ECB will begin purchasing a larger than anticipated Euro 50 billion per month of bonds issued by its 19 member countries. Underscoring the perceived severity of the economic crisis facing the Euro region, this program is open-ended and will remain in effect through at least September 2016, much to the chagrin of Germany, the largest and most fiscally sound member of the European Union. Unlike the recently terminated American version of QE, ECB President Mario Draghi will likely have significantly greater challenges in executing his plan.

Reacting to the increasingly dire European economic situation, the Swiss government has elected to stop defending its currency versus the Euro, which resulted in an immediate 20% valuation surge. Meanwhile, the Euro continues to slide, currently at 1.12 versus the USD, down from 1.40 last summer. We anticipate the peg will reach close to parity later this year. While possibly a positive for European exporters, most imported commodities used in manufacturing and production are priced in USD’s. So, the weakening currency is offsetting much of the beneficial decline in oil prices. Worries about the viability of Greece, the most fragile of the ECB member countries, are intensifying following last weekend’s landslide election of the radical left Syriza party.

It appears to us that the broadening global weakness could be beginning to negatively impact the U.S. expansion. Heightened stock market volatility suggests more of a two-way trading environment, if not an outright sustained correction. This pattern will likely give investors pause, especially those who have been spoiled by the mostly one-way direction of the U.S stock market the past two years. Recent Q4 earnings announcements have been mixed and many companies continue to guide 2015 earnings as well as market expectations lower. Investor sentiment might be shifting.

Recently, both the World Bank and the IMF dropped their global growth forecasts for 2015; only the U.S. economy’s growth projection was raised. Eurozone growth is targeted at only 1.2% while unemployment remains near 12%. Japan is mired in recession and implemented its own QE bond buying program last year. Emerging market countries, led by China, continue to disappoint. Many in Latin America, such as Brazil, rely on commodity exports for a major portion of GDP. Softening global demand, intensifying supply competition (e.g., oil), and a strengthening dollar, have combined to paint a fairly disappointing picture. Developing nations are primarily dependent on world trade. Stimulus measures undertaken after the 2008 financial crisis have run their course leaving many with high debt loads.

Exports account for less than 15% of U.S. GDP, so the stronger dollar should not be too disruptive to domestic economic prospects; however, multi-national corporations, dependent on foreign earnings, will likely experience a hit to future EPS. Inflation should remain low even as increased consumer spending on a multitude of less expensive imported goods will aid the domestic economy. Cheap energy costs is shifting spending patterns. The employment picture continues to improve as evidenced by the latest 5.6% unemployment reading.

Given the current state of global events, we see no reason for the Fed to prematurely move ahead with its rate normalization plan as many anticipate occurring by mid-year 2015. The employment picture continues to improve and inflation continues to run well-below the Fed’s 2% target. Therefore, rates will stay lower for longer - perhaps into 2016.

Despite investment yields falling further in January, U.S. government bonds are even more attractive today on a comparative basis. At a yield of 1.80% currently, the UST 10-year note yields 30 bp more than UK Gilt, 140 bp over German Bund, and 160 bp better than Japanese debt. Foreign buyers of U.S. obligations also gain from renewed USD strength.

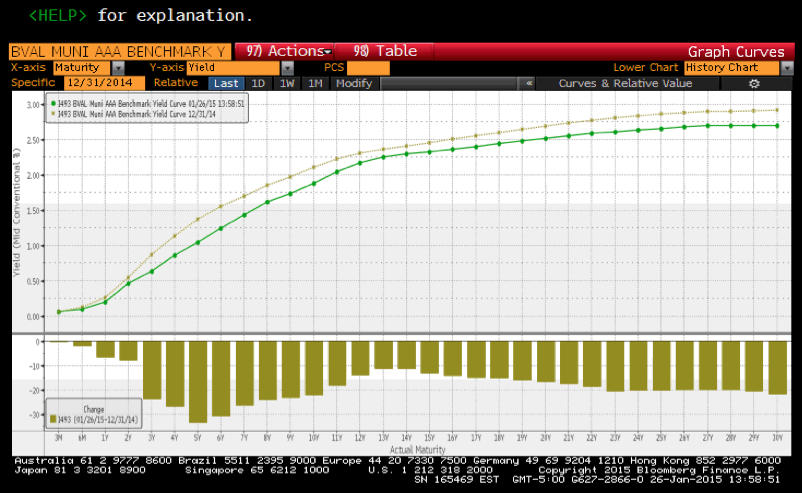

Bond yields have the potential to move even lower from here and we are positioning client portfolios to take advantage of the still constructive environment. The more volatile trading environment in virtually all financial markets is not surprising after the prolonged period of tranquility exhibited last year. The whipsaw trading patterns in stocks and Treasuries has been evident in the tax-exempt arena as well. The graph below depicts the shift of the municipal yield curve in January. While yields have dropped across all maturities, the greatest effect was registered in the short and long term maturity ranges. Intermediate maturities (10 to 20 years) have not participated to the same degree, thereby registering less yield decline. The resulting “steepening” of the curve in the intermediate range renders it the most attractive for investment.

The strong responsiveness by Treasury yields to the aforementioned factors has left municipals trailing in the race to lower rates. 10-year “AAA-rated” municipals currently yield more than 100% of similar maturity Treasuries. The relative attractiveness should attract buying interest from additional non-traditional tax-exempt buyers.

Shift in the Municipal Yield Curve From Year-End 2014

Source: Bloomberg

The municipal market will continue to take its direction from Treasuries. Favorable market technical conditions are in place for sustaining lower rates. Investor demand has been very robust since the start of the year, which has translated into strong money flows into tax-exempt mutual funds, including nearly $1 billion just last week, nearly twice the weekly average of 2014 according to the Investment Company Institute. Also, there is significant amount of outstanding securities maturing through February. Market reduction continues: last year the $3.5 trillion municipal market contracted by 4% and further shrinkage is expected this year.

Following the State of the Union speech last week, there has been renewed discussions in Washington about solutions to address the critical need for infrastructure spending throughout the country. The President called for legislation to create public/private partnerships. Near-term, we think the prospect for a bipartisan agreement is remote. While the financial state-of-the-states is much improved, fiscal discipline is still the primary focus in most state capitals. Mounting pension and health care costs, combined with new requirements for more conservative actuarial earnings assumptions precludes much in the way of capital spending initiatives. Municipal borrowers should at least be encouraged by the outlook for sustained lower borrowing costs for a longer period of time.

smcfixedincome.com

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary is neither an offer to sell nor a solicitation of an offer to purchase securities, any other investments or any other product sponsored or advised by SMCFIM, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. Such an offer or solicitation may be made only by the relevant documents for the relevant investment vehicle and/or investment program. This commentary is not, and may not be used as, a recommendation of any security, investment program or vehicle. There is no assurance that any securities discussed herein will remain in a client’s account at the time you receive this commentary or that securities sold have not been repurchased. The securities discussed do not represent the client’s entire portfolio and in the aggregate may represent only a small percentage of the client’s portfolio holdings. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2015 Spring Mountain Capital, LP. All rights reserved.