The threat of higher interest rates is dominating many 2015 outlooks for investors and professional forecasters alike. Consensus expectations call for the Federal Reserve (Fed) to begin tightening in the second half of the year, with market rates to rise in concert and bond prices to fall. But the changing composition of voting members on the Federal Open Market Committee (FOMC) is a looming variable that I believe will likely impact the pace and severity of Fed action.

A more dovish Fed favoring low interest rate— combined with indications of global economic slowdown and falling asset prices — may translate into a more benign rate environment for 2015 than expected. With this in mind, investors may want to reconsider stripping away all interest rate exposure from their income allocation and instead consider a more diversified and balanced maturity structure.

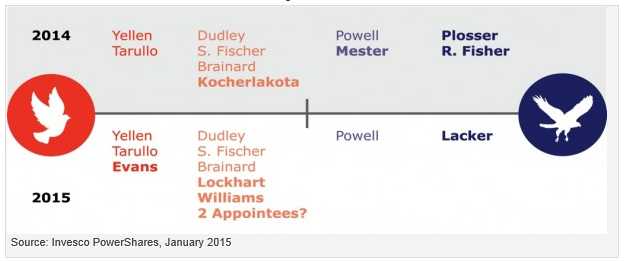

FOMC rotation favors dovish views

In my view, the January 2015 changes to the membership of the FOMC will bring about an even more dovish weighting to voting, based on historical voting patterns and public comments made by members.

- Three voters viewed as hawks or hawkish because they favor higher interest rates — Charles Plosser, Richard Fisher and Loretta Mester — are rotating off.

- The only dovish voter stepping aside is Narayana Kocherlakota, who actually has a fairly balanced history of voting patterns.

- Committee additions include three with dovish views: Charles Evans, Dennis Lockhart and John Williams.

- President Barack Obama can fill two additional vacancies, and I would expect his appointments to carry dovish inclinations.

- Jeffrey Lacker, who has expressed very hawkish views, also joins the FOMC, but he will likely be the loner at that end of the spectrum.

FOMC 2015: Dominant Doves May Create a More Patient Fed

Implications for investors

If a more dovish Fed takes a slower, steadier approach to tightening than anticipated, fixed investments with longer average durations may not be the portfolio-killers they might otherwise be in an environment where the interest rate rises more rapidly. In fact, peppering portfolios with some exposure to longer duration may offer an opportunity for enhanced yield and total return, as well as diversification from equity risk. While a fixed income allocation built for Fed tightening may still be appropriate for many investors, blending a little duration into a portfolio may be beneficial if rates once again defy expectations and continue to fall.

Adding duration into a fixed income allocation

After talking to their financial advisors, investors may want to consider increasing their exposure to high-quality, longer-duration strategies. For example:

- PowerShares Build America Bond Portfolio (BAB), tracks an underlying index that invests in taxable municipal securities. BAB, which carried duration of roughly nine years as of Dec. 31, 2014.

- PowerShares National AMT-Free Municipal Bond Portfolio (PZA)* offers tax-efficient exposure to duration in an uncertain tax environment. PZA showed duration of eight years as of Dec. 31, 2014.

- PowerShares Emerging Markets Sovereign Debt Portfolio (PCY) offers duration exposure for investors willing to accept emerging market exposure. PCY’s underlying index invests in a portfolio of emerging market sovereign debt denominated in US dollars, and the fund carried duration of nine years as of Dec. 31, 2014.

Important information

The Federal Open Market Committee (FOMC) is a 12-member committee of the Federal Reserve Board that meets regularly to set monetary policy, including the interest rates that are charged to banks.

Duration is a measure of the sensitivity of the price of a fixed income investment to interest rate changes.

*Effective July 8, 2014, the Fund’s name, investment objective, investment policy, investment strategies and underlying index changed. The Fund’s name changed from PowerShares Insured National Municipal Bond Portfolio to PowerShares National AMT-Free Municipal Bond Portfolio, and the underlying index changed from BofA Merrill Lynch National Insured Long-Term Core Plus Municipal Securities Index to BofA Merrill Lynch National Long-Term Core Plus Municipal Securities Index.

Before investing, investors should carefully read the prospectus/summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the Fund call 800 983 0903 or visit invescopowershares.com for the prospectus/ summary prospectus.

Diversification does not guarantee a profit or eliminate the risk of loss.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the Underlying Index.

Investments in fixed-income securities, such as notes and bonds, carry interest rate and credit risk. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. Credit risk is the risk of loss on an investment due to the deterioration of an issuer’s financial health. Due to anticipated Federal Reserve Board policy changes, there is a risk that interest rates will rise in the near future.

For BAB and PZA, municipal securities may be affected by political changes as well as uncertainties in the municipal market related to taxation, legislative changes or the rights of municipal security holders. The market for municipal bonds may also be less liquid than for taxable bonds.

For BAB, there is no guarantee that municipalities will continue to take advantage of the BAB program in the future and there can be no assurance that BABs will be actively traded. Furthermore, under the American Recovery and Reinvestment Act of 2009, the ability of municipalities to issue BABs expired on Dec. 31, 2010. As a result, the number of available BABs in the market is limited. In addition, illiquidity of the BABs may negatively affect the value of the BABs.

For PZA, there is no guarantee that the Fund’s income will be exempt from federal or state income taxes

For PCY, the Fund will invest in foreign bonds and, because foreign exchanges may be open on days when the Fund does not price its shares, the value of the non-US securities in the Fund’s portfolio may change on days when you will not be able to purchase or sell your shares.

For PCY, sovereign debt securities are subject to the additional risk that – under some political, diplomatic, social or economic circumstances – some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due. The fund may have limited legal recourse against the issuer and/or guarantor of sovereign debt when default occurs. As a holder of government debt, the Fund may be requested to participate in the rescheduling of such debt and to extend further loans to government debtors.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.