With the highest productivity in Europe, a sizeable current account surplus and rock bottom interest rates, is there a case to made for German equities? Germany's competitiveness, export performance and trade surplus should increase as the Euro weakens helping German exporters in markets outside of the Euro bloc.

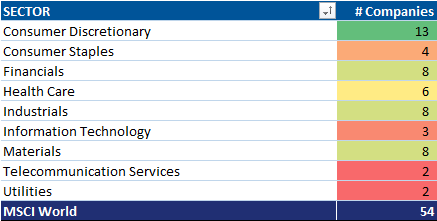

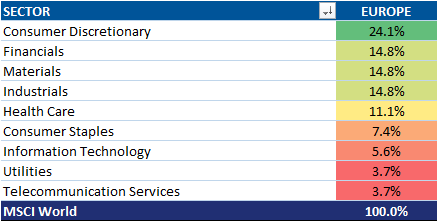

Let's start with a few details to set the context. First, let's look at the composition of the German stock market. Our table below shows the number of companies in each sector in the MSCI Germany index and then the next table shows the percentage of companies in each sector.

MSCI Germany - Number Of Companies In Each Sector

MSCI Germany - Percentage Allocation By Sector

We can divide the MSCI Germany index into two broad segments--cyclicals (consumer discretionary, financials, materials, industrials, information technology) and counter-cyclicals (health care, consumer staples, utilities and telecom). Roughly 75% of the companies in the MSCI Germany index are cyclicals, while counter-cyclicals are roughly 25% of the index. Late cyclicals (materials, industrials....Germany has no energy companies in the MSCI Germany index) are roughly 30% of the index. Growth counter-cyclicals (health care and staples) are just under 19% of the index.

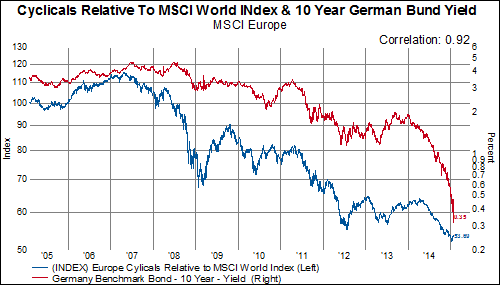

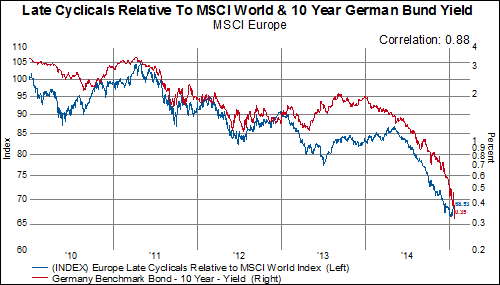

Next let's describe how cyclicals and counter-cyclicals have been performing in Europe. Over the last ten years, MSCI Europe cyclicals have significantly underperformed the MSCI World index. In the chart below, we show the relative performance of MSCI Europe cyclicals vs. counter-cyclicals compared to 10 year German Bund yields. Cyclicals have underperformed counter-cyclicals by 46% over the last 10 years as German yields have collapsed to 35bps.

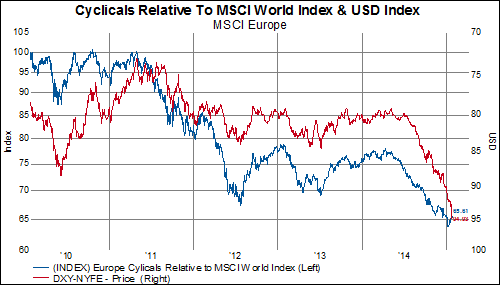

Over the last five years, the relative underperformance of European cyclicals can also be considered against the USD. Strength in the USD (red line, inverse, right scale) is highly correlated to the relative performance of cyclcials (blue line, left scale).

Late cyclicals in particular are very highly correlated (88%) to movements in German yields.

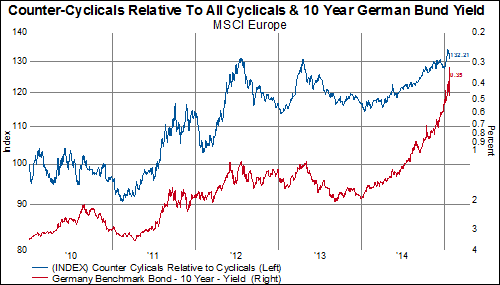

So, it's fair to say that based recent experience, a falling Euro and falling rates in Europe are a bad combination for European cyclicals. On the other hand, these things are good for the relative performance of European counter-cyclicals. In the charts below, we show the relative performance of counter-cyclicals vs. cyclicals compared to German rates.

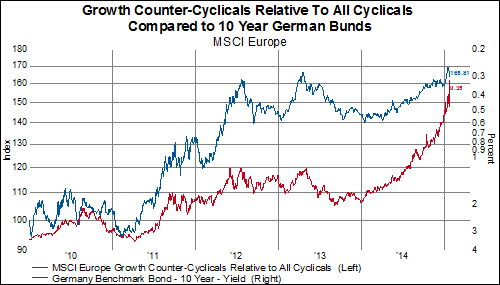

The relative performance of counter-cyclcials vs. cyclicals has recently broken out to new highs. Counter-cyclicals have outperformed by 33% over the last five years. Drilling down to the growth counter-cyclicals, the same observation holds. Growth counter-cyclicals have outperformed cyclicals by 65% over the last five years.

To summarize:

1) Only 25% of the MSCI Germany index are counter-cyclicals

2) Counter-cyclicals relative outperformance is highly correlated to the Euro and German rates

3) Counter-cyclicals have significantly outperformed over the last 5-10 years

4) Likely, if the Euro continues to fall and German rates continue to fall, counter-cyclicals should continue to outperform

Now, lets take a look at a group of German companies to see what we have to pick from. Our investment strategies are based on the concept that companies that spend huge amounts of money on intangible forms of capital are systematically mis-understood in the marketplace due to conservative accounting standards that compel these companies to expense their intangible investments. So, we'll focus on the German companies inside of our Gavekal Knowledge Leaders Developed World Index (link for more information).

Gavekal Knowledge Leaders Developed World Index - German Companies

Gavekal Knowledge Leaders Developed World Index - German Companies

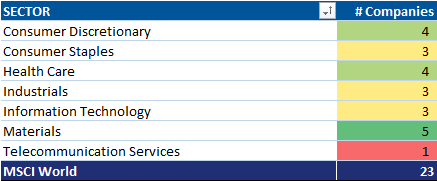

Our index has 23 German companies, with a high proportion of our index represented by counter-cyclical companies. Roughly 30% of our index is growth counter-cyclicals, there are no financials in our index and technology companies are 13% of our index compared to 5.6% in the MSCI Germany index. In the table below, we list all the companies in the Gavekal Knowledge Leaders Developed World index.

Gavekal Knowledge Leaders Developed World Index - German Companies

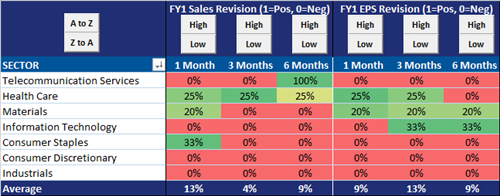

Ok, let's begin the investment case with the biggest problem we have with these companies. We are US based investors and do not hedge the currency risk, so all of our systems are designed around this perspective. When the Euro is sinking, it causes our USD measurement of sales and earnings momentum of Euro denominated companies to look terrible. In the table below, we show the percent of German companies in our index that have positive sales/earnings revisions in the last 1, 3, 6 months. Only 9% of the companies in our index have had positive sales/earnings revisions over the last six months, meaning 91% of companies have experienced falling estimates. So far at least, any expected fundamental benefit of a falling Euro is not making its way into sales/earnings estimates.

Gavekal Knowledge Leaders Developed World Index - German Companies

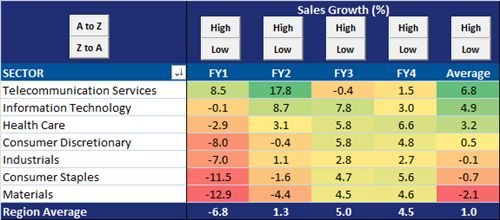

There has been an especially large hit to FY1 sales estimates, which really drags down our four year average projected top-line growth. Sales growth is estimated to be down almost 7% in USD terms this year.

Gavekal Knowledge Leaders Developed World Index - German Companies

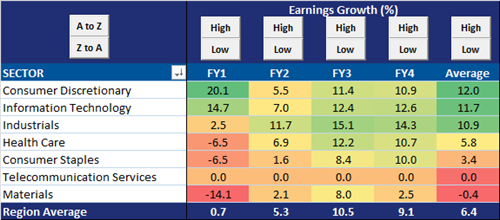

There has been a similar impact on earnings projections, though it appears to us that earnings may still be out of line with top-line expectations. If USD revenues are down 7% this year, it is highly unlikely earnings will rise by almost 1%.

Gavekal Knowledge Leaders Developed World Index - German Companies

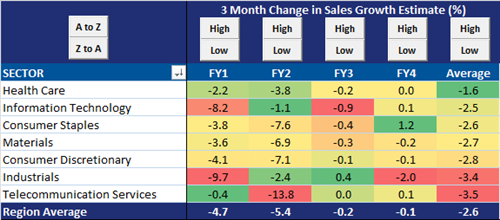

To calibrate those top-line and bottom line estimates, we show next the three month change in the next four years estimates. So the health care, that is now expected to have sales contract by 2.9% this year (tables above), has seen its growth for this year drop 2.2% over the last three months. This means, sales growth for FY1 just three months ago was -.7%. Similarly, industrials are now expected to experience a 7% contractions in sales this year, which has fallen 9.7% over the last three months. That means as recently as November, analysts expected these German companies to have top-line growth of +2.7% for FY1. These are big reductions in fundamental estimates. Growth counter-cyclical sectors and technology have been spared a lot of the damage.

Gavekal Knowledge Leaders Developed World Index - German Companies

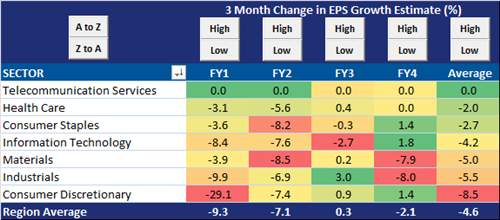

Recent downgrades to earnings have been even more severe, with an average reduction of earnings growth in FY1 of -9.3%. FY2 growth has come in by 7.1% over the last three months, and average growth over the next four years has come down by 4.6%. Once again, counter-cyclical sectors have been spared most of the damage.

Gavekal Knowledge Leaders Developed World Index - German Companies

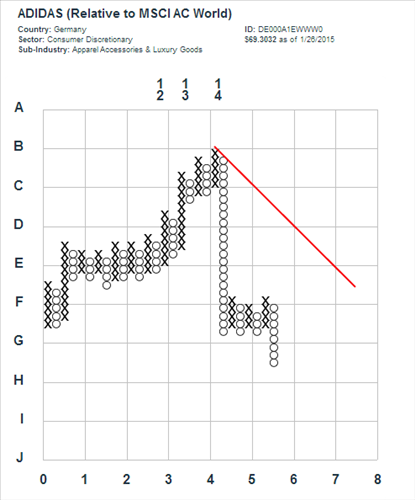

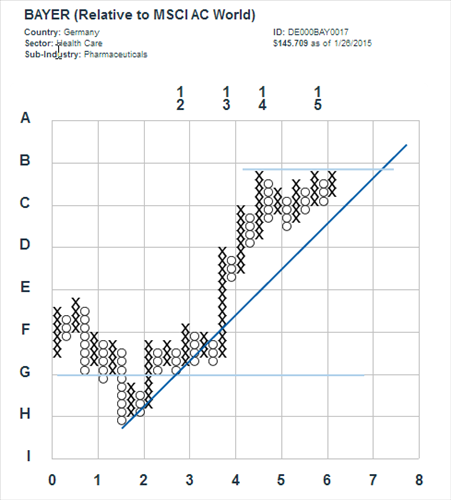

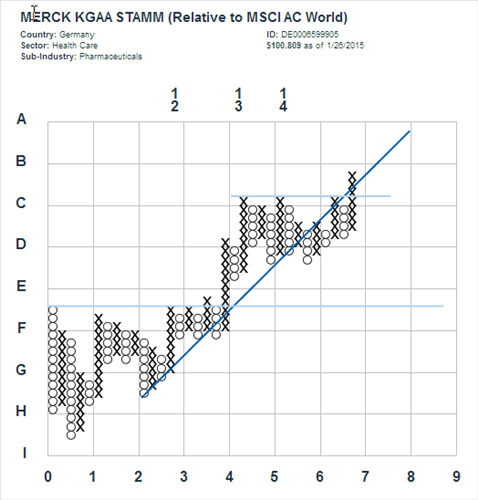

The price momentum of many German companies has been pretty structurally weak over the last few years. In our point and figure charts each X is a 2.5% relative increase compared to the MSCI All Country World index (MSCI ACWI) and each O is a 2.5% relative underperformance. All prices are in USD. We require a box reversal, or 7.5%. There are many companies that are in structural relative strength downtrends suggestive of distribution. Adidas is an early cyclical and good representation of what many cyclical charts look like.

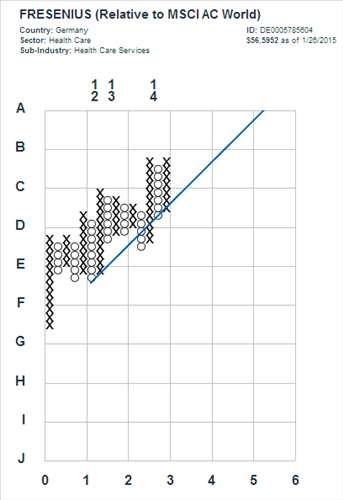

On the other hand, there are some constructive looking patterns among some of the growth counter-cyclicals. Below we show Fresenius, Bayer and Merck KGAA.

Bringing together our conclusions on German stocks, we think:

1) On a macro level, counter-cyclicals should be favored over cyclicals to the extent the Euro continues to drop and German rates continue to fall.

2) One should focus on our Gavekal Knowledge Leaders Developed World index companies to gain a greater exposure to growth counter-cyclicals and technology companies in Germany.

3) Cyclicals have borne the brunt of recent sales/earnings revisions, with the slight exception of technology

4) Select counter-cyclicals are in structural relative strength uptrends and should be the first place to look for new German investment ideas.

5) In particular we can make a case Fresenius, Bayer and Merck KGAA.

Read more commentaries by GaveKal Capital