Global Economic Perspective: January

Data Have Continued to Point to a Solid US Economy

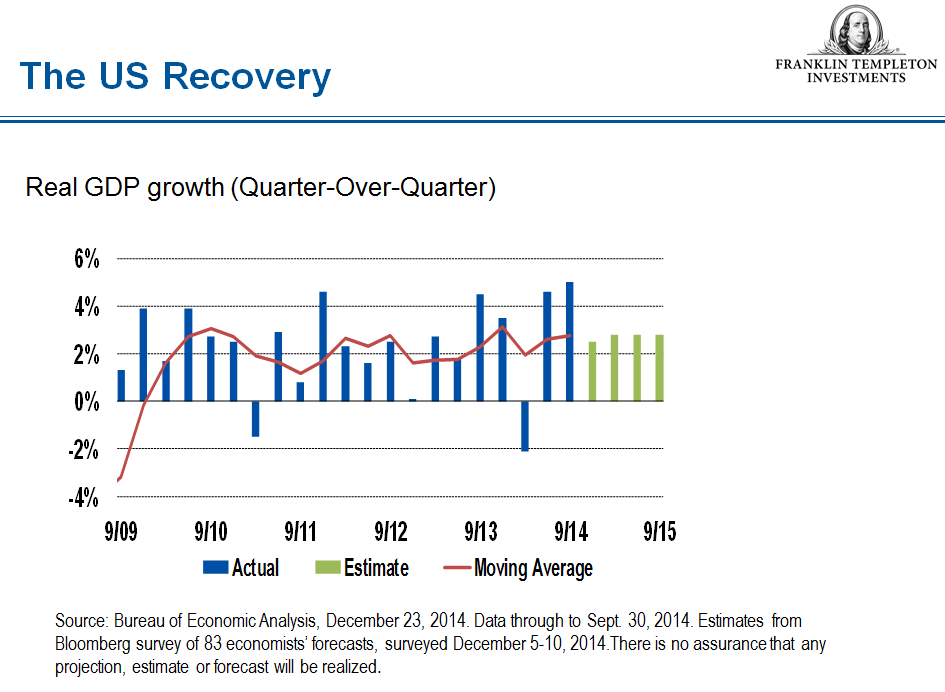

After a much better-than-expected annualized growth rate of 5% in the third quarter of 2014, the stars would seem to be fairly much aligned for continued US growth in the months ahead. Job growth has continued apace, interest rates and energy prices have remained low, and consumer and business confidence has been buoyant. As we start the new year, the main areas of uncertainty would seem to be the pace of growth and the implications of recent price and employment trends for the timing of monetary tightening by the US Federal Reserve (Fed).

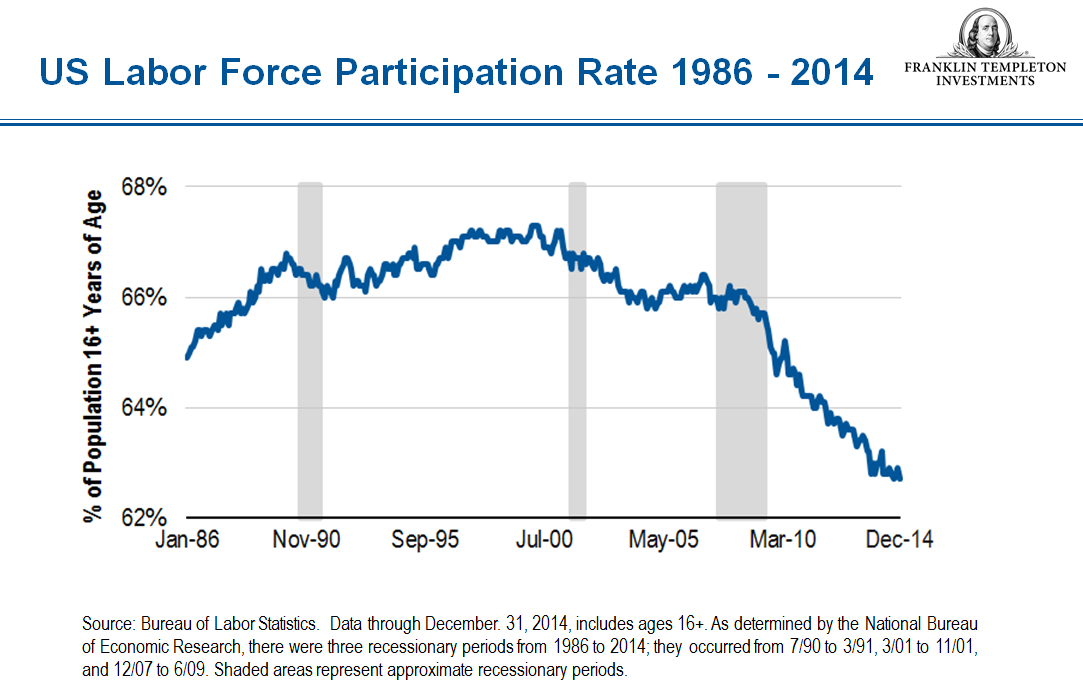

There was one item of data weakness in the first days of 2015 to remind us that the recent pace of growth may not prove sustainable. Although still strong, one closely viewed leading indicator, the Institute for Supply Management’s (ISM’s) manufacturing purchasing managers index (PMI), shifted back in December. Despite big improvements in job creation and a fall in the headline unemployment rate, broader indexes of US unemployment are still in the double digits and the labor force participation rate has remained at a low level last seen in the 1970s. Nor is the fall in energy prices of universal benefit to the US economy. The US shale industry has come under tremendous pressure, as have those who finance it. Energy-related capital expenditures (capex), which represent a sizable chunk of US business investment and have been growing faster than other forms of capex, can be expected to fall.

But we think the hit on US economic output overall, compared to some countries that rely heavily on oil revenues, should be relatively insignificant and that it should be more than offset by the increased spending power for consumers that comes with cheaper oil. Already there are signs of increased disposable income being spent, with real personal consumer expenditures (PCE) increasing by a solid 3.2% in the third quarter of 2014, according to the Bureau of Economic Analysis (BEA). As a result of trends in oil prices and employment, consumer spending—almost 70% of gross domestic product according to the BEA—can thus be expected to contribute significantly to the continued growth of the US economy.

The statement released at the end of the Federal Open Market Committee’s (FOMC’s) meeting in December was marked by caution, with the FOMC saying it could be “patient” in its moves to normalize monetary policy. But sustained US economic growth—especially if, as in the third quarter, it comes in above-trend—could potentially place the Fed in a difficult position to hold the line on rate increases. The Fed’s unease comes from the combination of broadly good growth and labor-market trends on the one hand and low inflation on the other. The Fed is discounting the effect of oil prices on headline inflation, saying it is “transitory,” and is instead focused on core PCE (excluding food and energy prices). Core PCE rose at an annualized rate of just 1.4% in November, down from 1.6% in October, and some way off the 2% rate the Fed would generally like to see. Core inflation has remained tame in spite of strong job creation. Yet while the US economy created just under 3 million jobs in 2014—the best year for the US labor market since 1999—the labor force participation rate has remained low. In spite of a strong nonfarm payrolls figure for December, the participation rate actually fell during the month. The rate was basically the same as it was one year ago and points to continued labor-market slack. Hourly wages tell a similar story: After growing by 0.4% in November, they fell back again (by 0.2%) in December. Wage growth has been so poor that the US middle class has yet to regain its pre-2008 median income levels.

But we may be on the cusp of change in all these areas of concern for the Fed. The participation rate for prime-age workers (those aged 25–54) has been declining over the long term but stabilized in 2014, according to the Bureau of Labor Statistics. Because of the economy’s strengthening and the drop in the official unemployment rate, we could potentially begin to see an increase in the number of better-paying jobs, which would lure discouraged workers back into the labor force. A tightening jobs market could spark wage growth and eventually boost inflation. And while hourly wage figures have been disappointing thus far, real wages have begun to rise thanks to low inflation and falling energy prices.

All things considered, while the latest minutes from the FOMC meeting show concern about downside risks from the rest of the world, and while US inflation has continued to undershoot, we believe the prospects look ripe for a mid-2015 rate rise, as the Fed itself has been broadly hinting, we believe rate tightening could initially be modest.

Oil Price Drop Likely to Push Up World Growth

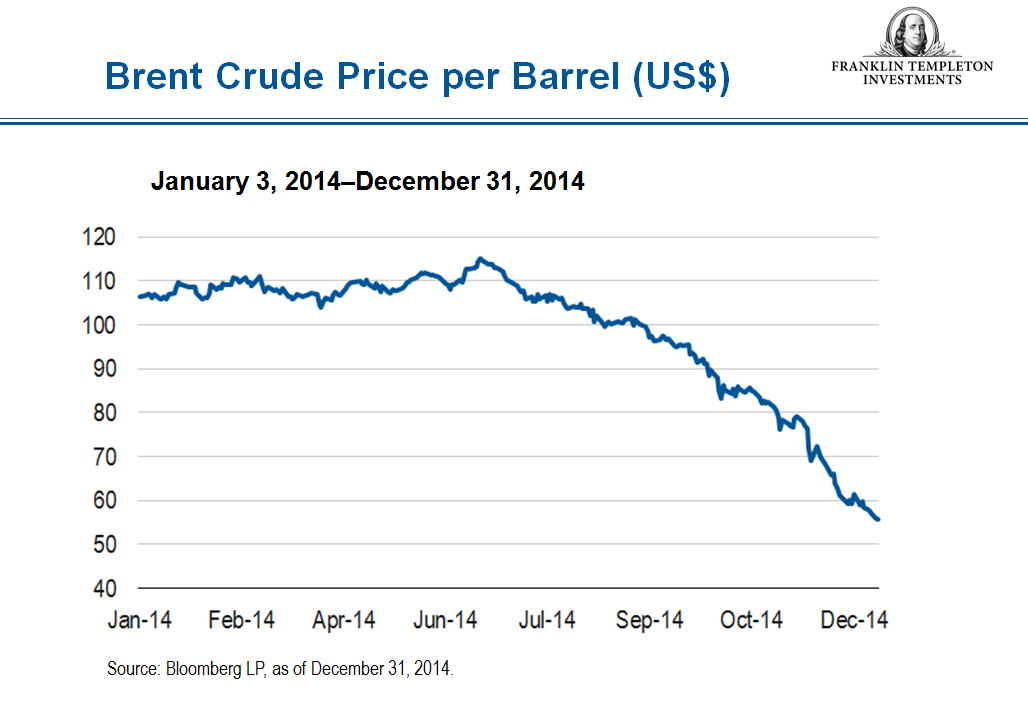

Oil prices have continued their relentless decline from a 2014 peak of over US$110 per barrel of crude in June. By the end of the first week of January 2015, prices had fallen below the US$50 mark, and with the Organization of the Petroleum Exporting Countries (OPEC) resisting pressure to cut production to support prices, many observers believe they could fall further in the coming weeks.

Aside from the impact on a number of oil-dependent economies, the trend is positive for the global economy, in our view. Lower energy prices typically raise real income for consumers and help keep a lid on inflation, thus helping ensure that monetary policy remains accommodative. The Fed and the Bank of England may feel they have more time before they need to raise rates even modestly this year, while in the eurozone and Japan, which both face the scourge of deflation, the case for further monetary easing is bolstered by the drop in energy prices. The People’s Bank of China also can point to falling inflation to relax monetary policy in the face of China’s moderating economy.

Just as encouraging, a number of emerging-market economies have seized the chance offered by plunging oil prices to reform “distorting” fuel subsidies, hence shoring up public finances and better preparing themselves for economic slowdowns. Countries ranging from Egypt to Malaysia, and from India to Indonesia, have all moved toward cutting fuel subsidies in recent months. We regard the curtailment of energy subsidies as one of the biggest changes to a decades-old system that has tied up budget funds and bloated energy imports in many places. Even some Gulf nations such as Oman (which faces a fiscal deficit) have moved to cut energy subsidies. There are signs that the downward pressure on oil and natural resource prices is also helping the cause of reform in countries such as Brazil (considered one of the “losers” from falling oil prices). There, newly re-elected President Dilma Rousseff announced sweeping welfare reforms at the end of December designed to shore up the country’s finances and help preserve its all-important investment-grade credit rating, while in Saudi Arabia, sweeping government cabinet changes were announced at the end of last year in an apparent effort to accelerate the pace of economic and political reform.

At the same time, we believe the prospects for a number of energy-reliant countries do not look bright in the short term. Select countries that lack reserve funds and that rely heavily on oil to support state budgets and current account balances will likely suffer from lost revenue and lower growth. In Russia and Venezuela, oil-related revenues represent a significant portion of their respective total fiscal revenue. These countries have already been facing deep economic problems and are likely to experience more strains should depressed oil prices persist. There might be the risk of further geo-political instability involving countries like Russia, Iran and Iraq as a result of their declining macroeconomic prospects. However, we believe that while there are losers from the dramatic fall in oil prices of the past six months, the global economy as a whole should benefit from lower oil prices in the coming months.

European Outlook

There was a sense of déjà vu to the early weeks of 2015 for the eurozone, with yet another reminder of the bloc’s pallid economic recovery and renewed political uncertainty in Greece. The final reading for Markit’s December PMI for the manufacturing sector missed consensus expectations and was only marginally above the 50 level that shows expansion. Markit said rates of growth for output, new orders and employment “all continued to track close to stagnation.” The Markit composite PMI index that covers both services and manufacturing also disappointed. Overall, the eurozone probably notched growth of less than 1% in 2014, below even the feeble 1.2% growth that the European Commission was forecasting last May.

As for Greece, the radical-left Syriza party emerged victorious from snap elections in late January. The head of Syriza and new Greek prime minister, Alexis Tsipras, has been working to dispel investor fears that it would tear up Greece’s bailout agreement with international creditors—but in any case, mechanisms have been put in place that should ensure, it is hoped, that a renewed run on Greek debt will not provoke a wholesale eurozone sovereign bond crisis, as it did in 2010. While yields on French, Italian and Spanish benchmark 10-year bonds had fallen to historic lows by early 2015, only time will tell whether the establishment of a form of European banking union and the huge reduction in financial institutions’ exposure to Greece means the contagion effect from any renewed debt crisis is more limited than in 2010–2012. Nonetheless, any negotiations with Greek lawmakers about possible debt writedowns after the election could be fraught.

A seemingly panicky, middle-of-the-night decision by Russia’s central bank to hike its main interest rate to 17% in mid-December further contributed to the sense of déjà vu. Fears of a re-run of Russia’s 1998 financial crisis and debt default have been calmed, at least temporarily, by defensive moves carried out by the Russian authorities. At the same time, the effect of a further deterioration in Russia’s finances could be a big blow to European companies and banks with exposure to that country.

On a brighter note, the fall in oil prices and drop in the value of the euro are making life easier for European households and corporations. But we think the beneficial effects should not be overstated. The drop in the euro and the much higher tax rates imposed on oil products in Europe mean that the effect of the cut in oil prices is less pronounced than in the United States. Just as importantly, the drop in headline inflation caused by plunging oil prices is contributing to deflation in Europe, increasing the real value of debts and potentially encouraging people to postpone purchases.

The scepter of deflation finally pushed the European Central Bank (ECB) on January 22 to announce a bond-buying package of €60 billion per month for 18 months starting in March. This is a massive injection of new money into the system that might be expected to lift eurozone inflation out of negative territory (the annual eurozone inflation rate was estimated at -0.2% in December), and could eventually boost inflation expectations, and therefore household and corporate spending. But at this stage, it is not at all clear that the ECB’s avowed aim to expand its balance sheet by €1 trillion would allow it to reach its inflation target of below but close to 2%, especially if energy prices continue to fall. At the same time, creditor states who oppose any notion of fiscal transfers ensured that 80% of the bonds that the ECB buys will be bought by national central banks at their own sovereign risk, not the ECB’s. Indeed, long-standing northern European reluctance about the whole idea of allowing the ECB to print money to buy government bonds points to important tensions within the ECB’s Governing Council that may have dramatic consequences further down the road.

Even before the January 22 announcement, the prospect of QE had already helped lower the yield on eurozone government bonds to historic lows, thus helping the finance ministries of highly indebted countries such as Italy, as well as banks in these countries. But it remains to be seen whether QE will change the current pattern of low growth and inflation. And amid the ongoing debate about the appropriate balance between austerity and growth policies in Europe, there is the gnawing doubt that injections of fresh money from the ECB will make it easier for southern European governments to renege on their commitment to fiscal consolidation and reform. Nonetheless, many market participants see the risk of deflation as far more urgent than fiscal consolidation, thus pleading in favor of the ECB’s latest intervention. However, we note that in our view, QE is no replacement for the structural reforms that could make eurozone economies more flexible and ensure the long-term viability of the single-currency project.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

© Franklin Templeton Investments

© Franklin Templeton Investments