Dear Fellow Investor,

As long-duration common stock owners, we are always interested and entertained when the media covers company earnings. To understand why, we think you need to know the facts behind the intrinsic value of a company, what it means to be a business owner and what differentiates a good business from a great one. Our contention is that there is little or no correlation between short-term stock price movements at the time of earnings reports and long-term success in common stock investing.

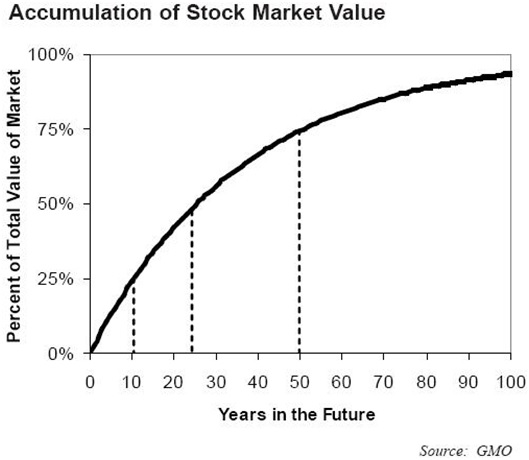

Ben Inker of Grantham, Mayo, Van Otterloo, studied publicly-traded common stocks to determine the composition of the intrinsic value mathematically. The chart below shows his results:

As the chart shows, 75% of the intrinsic value of a company is derived from cash flows more than 11 years later. An astounding 50% comes from flows more than 25 years from today!

We interpret this to mean that today's earnings reports are statistically inconsequential to intrinsic value. Huge price swings based on perceived hits or misses in the quarterly earnings report are laughable for the long-duration investor. To us, a more important metric for computing intrinsic value is to keep track of the attributes of a business that contribute to the longevity of it. Some examples of these metrics include strength of balance sheet, size of moat and stickiness of customers.

Homebuilders offer a wonderful prism with which to view these qualities. The most recent reports were stellar for profits, but most of the companies have shared that the current environment includes some profit-margin compression and lowered guidance for 2015. We are interested in their future because the home ownership among Americans 25-35 years of age is historically low and a majority of these folks will mature and buy homes. There has rarely been as big an economically positive spread to home buying in relation to renting in the USA.

One of our companies, NVR (NVR), the maker of Ryan homes in the Mid-Atlantic region, saw its stock tumble $61 (5.5%) inter-day on January 26, 2015. A $61 price change for a $1 miss on quarterly earnings defies Inker’s research. Only news associated with major changes in their business or industry, which seriously damages long-term business activity, could justify that kind of price volatility. Since the financial meltdown of 2007-09, numerous homebuilding companies closed their doors.

Earnings announcements, we think, confuse what it means to be a business owner. If you believe that owning part of a business through common stock ownership should be the same as owning the whole company, your attitude is dramatically different than most stock market participants. The owner of the entire business wants the free-cash flow to be large and growing. This is the way a business creates wealth: returning cash to the owners.

We were recently reminded of the importance of free-cash flow last week by a technology expert commenting on eBay’s (EBAY) recent earnings report on CNBC. EBay’s Marketplace reported that it generated $3 billion in free-cash flow in 2014, but that their earnings growth struggled this year due to a variety of factors (Google SEO change, currency headwinds, password resets). The tech expert then pointed out how much better of a business he thinks Amazon is than eBay’s Marketplace. We think it’s worth noting that Amazon’s free-cash flow in the last twelve months ended 09/30/2014 was $1.076 billion.

EBay announced that they’re breaking into at-least two companies. We’ve seen analysts estimates that value eBay’s Marketplace business at somewhere around a $30-billion market cap. This means that the sole owner of that business would be getting 10% of their money back each year in free-cash flow. Amazon, on the other hand, has a market cap of $145 billion and their $1.076 billion in free-cash flow would be great to receive as the sole owner, but we wouldn’t want to pay $145 billion to get at it. We have respected peers who believe that Amazon will eventually gush free-cash flow as they grow and mature, but that in our minds goes into the “too hard” to predict pile.

Lastly, quarterly earnings reports are notorious for ignoring how a good/great company is dealing well with difficult current circumstances and doing so in a way that leads them to great future success. In his book, Good to Great, Jim Collins explains that great companies have bad luck and good luck like any other company. He argues that great companies make the best of their bad luck situations and maximize the benefits of their good luck. We are much like Warren Buffett in our view of quarterly reports: when outstanding companies struggle temporarily, we ask whether the current difficulty is making their moat stronger or weaker and how this affects their long-term profitability.

Bank of America (BAC) and JP Morgan (JPM) provided recent examples of earnings reports which only focused on current circumstances and not how the report affected the moat. The stocks fell sharply as momentum investors showed some panic. Many macro-economic experts are convinced that U.S. interest rates will remain low and don’t want to touch these bank stocks until interest rate spreads improve.

On top of spread worries, investors fear that the regulatory and political climate will be miserable as far as the eye can see. These spread and regulatory issues only widen the moat of these banks in what is a very sticky customer business in the first place. We love the cheap prices in relation to book value and the contentiousness of these companies. Stock price volatility surrounding a company’s earnings announcement has little correlation to its long-term success and instead amplifies the cacophony earnings season adds to the noise the long-duration investor seeks to avoid.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.