In 2010, International Business Machines’ (IBM) then-CEO Sam Palmisano unveiled the company’s 2015 Roadmap in which management detailed its plans to grow (non-GAAP) operating earnings to “at least $20” per share by 2015. This plan was the successor to a 2010 Roadmap, originally unveiled in 2007, in which management outlined its plan to deliver “at least $10” in earnings per share by 2010. Since the company ultimately exceeded its 2010 Roadmap expectations and delivered $11.52 in 2010 earnings per share, the 2015 Roadmap was generally met with enthusiasm by IBM shareholders. However, the 2015 Roadmap has proven to be a bumpy ride. On October 20, 2014, along with a disappointing third quarter earnings report, current CEO Ginni Rometty disclosed that the company will fail to achieve “at least $20” in (non-GAAP) operating earnings per share, the cornerstone of the much-publicized 2015 Roadmap. This development provides a worthwhile context within which to assess some of the advantages and disadvantages of long-term earnings roadmaps, and provide an update on why we continue to view IBM as an attractive investment despite management’s acknowledgement that the 2015 Roadmap was overly optimistic.

Pros and Cons of Long-Term Earnings Roadmaps

While I am not a proponent of long-term earnings roadmaps, I can understand the appeal of such a tactic to the CEO of a business like IBM. IBM’s core businesses are generally much less volatile and much more resilient than typical technology businesses, and a long-term earnings roadmap was one method of illustrating this. In addition to conveying management’s view that the company’s operating earnings could nearly double between 2011 and 2015, the 2015 Roadmap detailed the favorable operating margin impact of operating leverage in the company’s software business, cost reductions in its services businesses, and a continuing business mix shift toward more profitable products and services. Recognizing that technology companies’ capital allocation track records have been mixed at best, the 2015 Roadmap also included an expectation that the company would generate approximately $100 billion in free cash flow between the beginning of 2011 and the end of 2015. Management committed that approximately 70% of that free cash flow would be returned to shareholders in the form of dividends ($20 billion) and share repurchases ($50 billion), and that an additional $20 billion would be used for acquisitions.

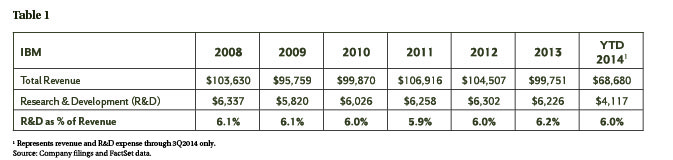

Although these objectives seemed reasonable enough at the outset of IBM’s 2015 Roadmap, the long-term earnings roadmap inevitably became a short-term earnings roadmap as time passed and 2015 approached. As revenue growth proved more challenging to achieve than management anticipated, the company also became more aggressive in its share repurchases. At the end of the third quarter of 2014, with five quarters remaining in the timeframe covered by the 2015 Roadmap, the company had already exceeded the $50 billion total share repurchase commitment by $4 billion. Some investors questioned whether these repurchases were the best use of capital, or were simply driven by management’s desire to reduce the share count in hopes of meeting the 2015 Roadmap operating earnings per share target. While we were generally pleased that IBM was repurchasing shares at a discount to our estimate of intrinsic value, we would have been concerned had these share repurchases been funded by drastic reductions in research and development spending. Because research and development is an important driver of product enhancement and innovation, and thus future revenue and profit, we believe it is important to monitor IBM’s commitment to research and development (R&D) spending despite a focus on cutting costs in other areas. As illustrated in Table 1, during the years covered by the 2015 Roadmap, R&D spending remained approximately 6% of revenue, consistent with the years preceding the 2015 Roadmap.

IBM’s R&D spending provides an interesting contrast to Hewlett-Packard’s R&D spending between its fiscal years 2002 and 2010. To be fair, Hewlett-Packard made large acquisitions of both Compaq and Electronic Data Systems that somewhat decreased the company’s necessary R&D spending as a percentage of revenue, but in my view, this only explains part of the significant reduction in the company’s R&D spending.

Underinvestment in R&D can have substantial negative impacts on a business, as was ultimately the case at Hewlett-Packard. So while we generally view IBM’s share repurchases as an attractive use of capital, we believe it is imperative that the share repurchases be done in combination with a continued commitment to R&D spending.

In my view, possibly the most significant downside of earnings roadmaps is the excessive focus placed on a single year’s earnings, which in the case of IBM was 2015. I would much prefer that management focus on continuously growing the intrinsic value of the business rather than managing the expectations of employees, analysts, and the press with regard to any single year of earnings. While we were disappointed that IBM failed to execute on portions of its 2015 Roadmap, the company’s 2015 earnings and free cash flow are a relatively small component of our estimate of intrinsic value, and we continue to believe that IBM shares are priced well below their intrinsic value.

Attractive Businesses at an Attractive Price

IBM’s software and services businesses account for the vast majority of the company’s profits, and each business has characteristics that make it fundamentally attractive and resilient. IBM’s software, the largest contributor of profit, is integral to the functioning of customers’ IT environments, and customers rarely want to endure the complexity and cost associated with switching to another provider. The services businesses give IBM an opportunity to solve substantial problems for customers in a mutually value-creating manner, and these service engagements often result in increased customer trust and dependence on IBM solutions. In addition to software and services, IBM possesses what is essentially a monopoly in the mature but lucrative mainframe hardware market and also operates a non-mainframe hardware business and a relatively small but profitable financing business.

We believe the combination of these businesses constitutes an attractive technology company that is well-positioned to grow intrinsic value per share over the long-term. The disappointment associated with the company’s 2015 Roadmap, and uncertainty about future growth, has resulted in a market price that is well below our estimate of IBM’s per share intrinsic value. If management is able to execute relative to fundamental expectations that are now lower than what was detailed in the 2015 Roadmap, we believe that IBM shares will provide attractive returns to shareholders.

The views expressed are those of the research analyst as of January 2015, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2015 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management