The domestic economy is growing at 3.0% to 3.5% pace. The budget deficit is plummeting and currently is less than 2.8% of GDP. The price of oil is in a freefall now below $55 per barrel and inflation is virtually nonexistent. The rate of unemployment is below 6.0%. These are idyllic conditions for any economy, especially five years after the largest financial crisis since the Great Depression. So, what’s the problem?

The problem is that the U.S. economy today is being propped up by aggressive monetary policies of the Federal Reserve. We are in the sixth year of a global expansion, and we are effectively still expanding the Federal Reserve’s balance sheet to support economic growth. Normally, that would end in the third year of an expansion. However, drastic times call for drastic measures and the severity of the Financial Crisis required the Fed to implement new tools to support commerce and capitalism. At the same time, Congress and the White House moved forward with both the Dodd-Frank Act and the Affordable Healthcare Act. Those two pieces of legislation have caused significant burdens to the business sector and have acted as a deterrent to job creation and wage growth. In effect, they are acting as hidden taxes that have increased the cost and risk of doing business.

When we started 2014, we believed the economy was on strong footing in spite of the brutal winter weather, and expected to experience stronger growth in the second half of the year compared to the first half. In addition, we believed that the banking system was well capitalized and private credit expansion would accelerate. With abnormally low volatility, we expected volatility would increase toward the end of the year as the Federal Reserve wound down its asset purchase program.

So, now here we are. In contrast to other major global economies including Japan, China and Europe, the U.S. economy appears to be humming along just fine. The Eurozone economy is faced with deflationary pressures, close to a recession and has made little progress in meaningful structural reform since the Financial Crisis. China’s economy is slowing dramatically. Japan has been under deflationary pressure for over twenty years and been unable to spark any meaningful growth in their economy over that time. And, now Russia’s economy which is dependent on the price of oil, appears to be entering a recession. Clearly, U.S. economic growth is the bright spot in the global economic picture.

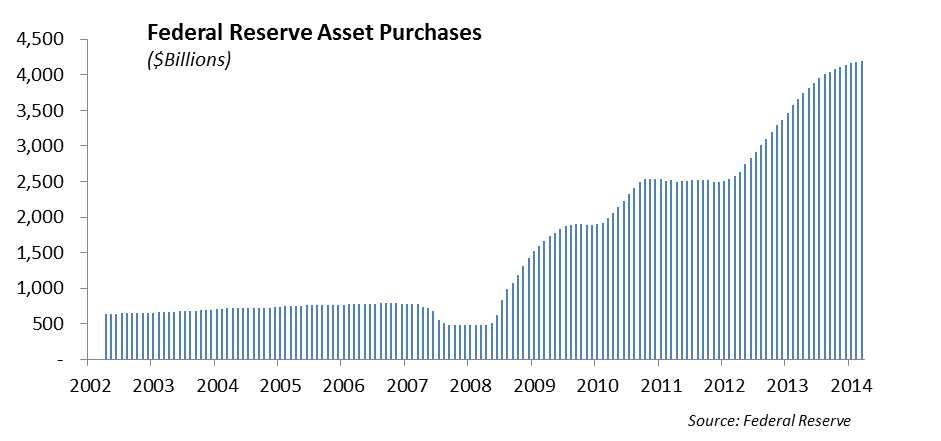

To be clear, we are still not experiencing sustained domestic economic growth. With over $3.5 trillion in cumulative asset purchases, our economy is heavily support by the stimulative monetary policies of the Federal Reserve. In spite of nearly one trillion dollars in fiscal stimulus and record budget deficits over the past five years, this economic recovery has been extremely weak by historic standards. At this point, we would not consider this economic cycle to be normal.

We have come to believe that our form of democracy and capitalism are evolving. Direct government intervention in our capital markets is here to stay and the lines between state-controlled capitalism like Russia and China and our form of capitalism in the United States have become more blurred since the Financial Crisis.

With that said, we expect 2015 will be the year that the Federal Reserve attempts to reduce its monetary support by allowing interest rates to move higher while still holding firm to its behemoth $4.5 trillion bond portfolio. That much anticipated signal will likely have an interesting impact on capital markets. The will be a natural ceiling to high interest rates will go in the U.S. given global capital flows and the ongoing demand for U.S. dollar denominated assets. As a result, in spite of an anticipated rise in interest rates next year, we expect that interest rates will remain low. As long as developed countries such as the United States, Japan and Europe implement asset purchase programs, global interest rates will remain low over the near term.

Ultimately, the problem is that there is too much money around the globe, funded by huge debt issuance, chasing too few good investment opportunities.

The U.S. Economy

Our outlook for domestic economic growth remains solid for 2015. The combination of a strong manufacturing sector, healthy employment picture, low interest rates and significantly lower oil prices will provide a stable foundation for the economy to continue growing and not overheating.

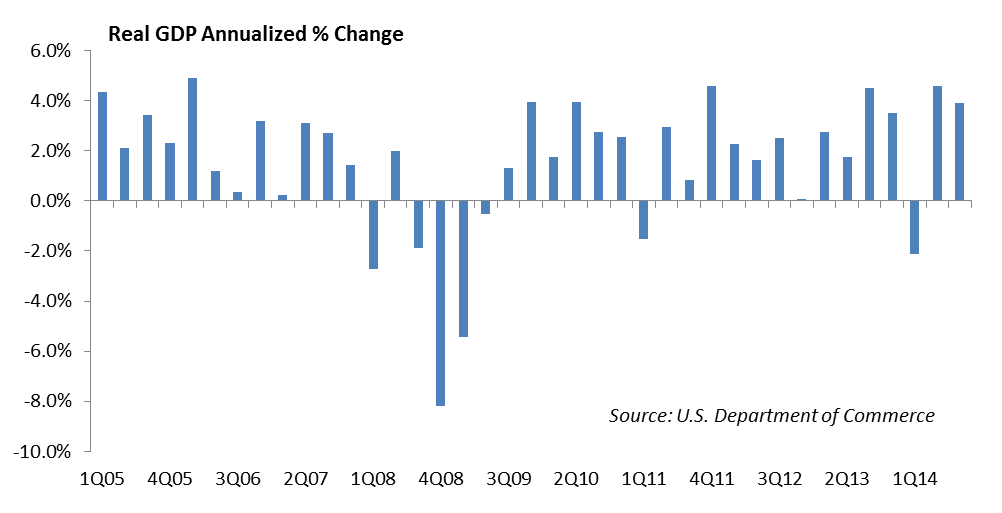

GDP growth has been tracking roughly 3.35% during the second half of 2014 and we are targeting 2.85% growth in GDP in 2015. This is predicated on continued health in employment, stability in the financial system, sustained low oil prices and continued improvement in private credit expansion.

The manufacturing sector has been the bright spot in the economy for the past four years. The ISM survey has peaked at 59 in August, and has settled in near 55 at the end of the year. Any reading above 50 is consider a positive for the manufacturing sector. With robust operating margins and strong balance sheets, corporate profits will continue to be strong in 2015.

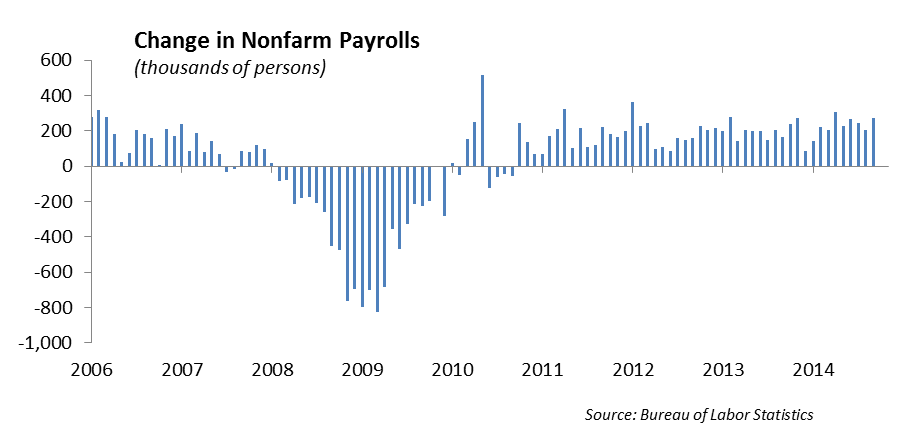

One of the key drivers for U.S. economic growth is employment growth. The economy has produced over 2.7 million jobs through November of 2014, which is the best year for employment growth since 2009. At the same time, claims for jobless benefits have been running lower than at any point since 2000. However, the challenge in the economy is reflected in the quality of the jobs being filled which have tended to be in the low level service, hospitality and construction sectors. Nonfarm payroll growth has been averaging over 200,000 for the past 27 months. While momentum in employment has slowed a bit, we believe there is enough momentum for marginal wage growth pressure next year. This should have a positive contribution to consumer spending.

There is a growing structural problem in the labor market as displaced workers, no longer affiliated as direct employees to a company on a W2 form, act in a capacity of an independent contract worker under Form 1099. Without getting overly technical, the contract worker is not entitled to benefits including healthcare coverage. This is one of the ways that employers can keep their compensation expense lower under the Affordable Healthcare Act since they aren’t required to pay benefits and pass the burden for healthcare coverage onto the contract worker.

At the same time, domestic inflation remains subdued, in fact too low. The Federal Reserve’s concern has been combating the spiraling effects of deflation which is one of the reasons they implemented the quantitative easing program and held short-term interest rates at zero for a prolonged period of time. The rapid decline in oil prices will likely exacerbate the deflation concerns.

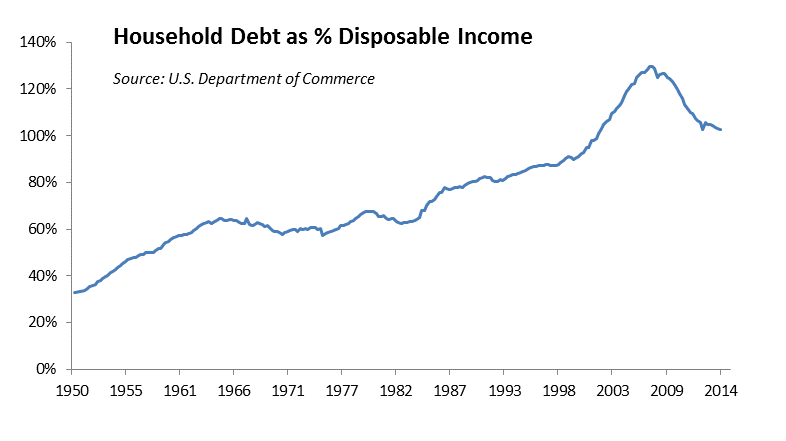

Personal consumption expenditures represent the largest part of the U.S. economy at roughly 68% of GDP. With the improvement in employment and household balance sheets, we expect the consumer sector to show strength next year. On the surface, the consumer has shown signs of improved health already. Interest payments as a percent of household income have declined significantly since 2009. The personal savings rate has been above 4% for the past seven years. However, household debt has been moving higher as incomes have notched higher.

We expect to see continued economic growth over the near term; however, there are warning signs that raise concerns for the economy in 2016. Imbalances build up in capital markets during periods of low volatility and, we are seeing evidence of those imbalances today. These imbalances include the shift of leverage to the government sector over the past five years, excessive equity valuations, the high correlation between asset classes, the persistent budget deficits in European countries, the huge amount of student loan debt, cybersecurity issues, the problems around implementation of rules under the Dodd-Frank Act, and the lack of capital supporting secondary trading on Wall Street.

In addition, we expect the structural problems imbedded in the economy around job creation and wage growth will continue to persist. This is part of our new reality in an evolving democracy. The dispersion in income levels among households has worsened over the past ten years according to data by the Census Bureau. However, for the first time in six years, incomes in the U.S. ticked higher.

The Role of the Banks in our Financial System

Banks play an important role in our financial system as a means to extend credit and support monetary policies of the Federal Reserve. However, their effectiveness in exercising that role has been neutered since the Financial Crisis. There are two main reasons for this: first, because of additional regulatory requirements, banks have been forced to raise capital levels. As banks are in the process of shoring up capital, it has been more difficult to make loans due to the additional capital required. Second, the repeal of the Glass-Steagall Act in 1999 allowed banks to generate revenue from many other sources. For example, lending became more transaction oriented as banks syndicated loans and then sold them off in the bank loan market.

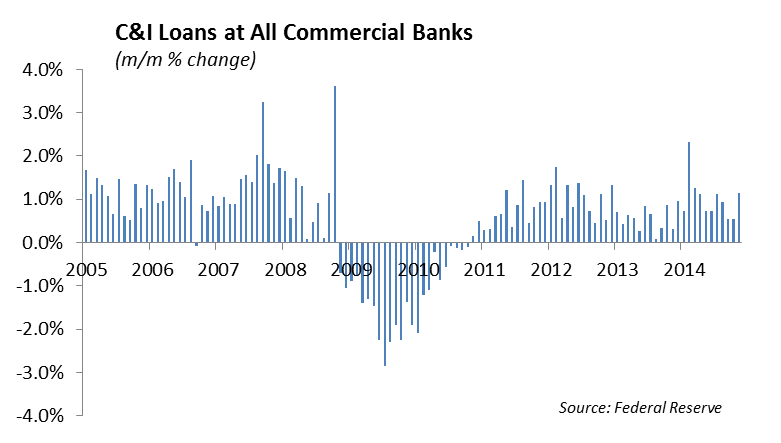

Banks have been forced to endure increasing regulatory oversight and increase capital levels from a dismal 4% to over 13%. This increased scrutiny has made for a difficult lending environment to small businesses which are the back bone of the economy. As a result, private credit expansion, part of the life-blood of sustained economic growth, has been muted since the Financial Crisis. Bank lending to small business is a structural problem in our economy that still needs to be addressed. While C&I loans have increased, we continue to hear discussions that small businesses still cannot access credit. The banks say they can’t lend because the regulators penalize the loans. Loans to businesses and consumers at U.S. banks have increased 12.8% over the past twelve months. With bank capital levels shored up, we expect there is potential that loan growth will continue to accelerate which will be a significant contribution to economic growth next year.

Monetary Policy

In our view, the face of the domestic capital markets forever changed as a result of the Financial Crisis. We are still in a huge experiment that the Federal Reserve implemented in order to stabilize the financial system and the capital markets. The tools that the Fed implemented had never been used in our capital markets prior to this period of time following the Financial Crisis. We are moving through a four-phase process following the Financial Crisis in which the Federal Reserve has sought to stabilize the capital markets to where capital markets trade with less government intervention and interest rates move back to trading in a targeted range.

During the first phase, the Federal Reserve implemented dramatic stimulus programs, known as Quantitative Easing, which included buying up to $80 billion in securities in the open market every month. This had the effect of stabilizing the capital markets, suppressing volatility and forcing interest rates across the yield curve lower all in an effort to stimulate economic activity. In our opinion, this proved overwhelmingly successful.

The second phase of the Fed’s journey was tapering the quantitative easing program in a manner that did not spook the markets and at the same time continued to support growth in the labor markets and rising inflation. This past October, the Federal Reserve successfully curtailed the active monthly purchase part of its asset purchase program. As a result, the Fed now holds a war chest of $4.5 trillion in U.S. Treasury and mortgage-backed securities on its balance sheet.

We believe we are now entering the third phase of a four-phase process that the Fed is navigating after the Financial Crisis. The third phase describes the period of time between the last bond purchases in October and the first hike in interest rates. Specifically, we are looking for how the Federal Reserve will wordsmith the “considerable time” language in its statement following the next Federal Open Market Committee meeting.

The fourth phase will be defined by the pace the Fed allows the Fed Funds rate to trade. We expect the Federal Reserve will use several unconventional tools to force interest rates higher including reverse repo and increasing the interest rate on excess reserves held on its balance sheet. We also expect the Fed to maintain a large bond portfolio on its balance sheet for the better part of the next decade.

The Global Economy

The global economy has experienced significant slowing over the past year as global demand has declined and deflationary risks penetrate many of the larger economies around the globe. We expect global demand to pick up over the second half of 2015. This is predicated on three major themes: an increase in consumption, an increase in private credit expansion as a result of improved health in the financial sector, and higher likelihood of stimulus in Europe, Japan and China. In addition to these three themes, we expect that lower oil prices will help global growth as well as consumers have more disposable income and businesses have improved margins due to lower fuel costs.

Europe

The word we use to describe European leadership has always been “dithering.” The Eurozone economy is languishing due to major structural problems. And, for all their talk and bickering, the leadership continues to dither, failing to muster the courage to make the difficult decisions necessary to fix the problems imbedded in the European Union. The Eurozone is now faced with a dangerous combination of slowing growth and deflation, and the leadership has done little to address either.

We expect the Eurozone economy to expand at a rate of 1.1% next year and inflation to remain below 1%. Germany and France, two of the strongest economies have had their forecasts reduced next year to 1.1% and .7% respectively by the European Commission. Both France and Italy are in a tussle with the EU over their 2015 budget which doesn’t conform to the 3% budget deficit limit.

High rates of unemployment, low job growth, a lack of business formation and private credit expansion are all problems throughout the region. Facing a slowing economy, the European Central Bank began talking about a bond buying program last September. We expect given the severity of the slowdown in the Eurozone economies and the pressure from the southern countries to help provide some stimulus, the ECB will begin implementing a version of quantitative easing during the first quarter of 2015. There is tremendous controversy around a QE program for the ECB and we expect it will underwhelm since interest rates in Spain, Italy and Germany are already near historic low levels.

Europe continues to put Band-Aids on its illness. Until the Eurozone has binding taxing authority and the ability to issue euro-denominated debt, the co-op currency of the euro will be challenged. Next year we expect to see a stimulus program from the ECB which will allow the central bank to purchase sovereign debt. Unlike the U.S. which has a republic, a central bank that can act as the lender of last resort, and an AA+ credit rating, the Eurozone has a mishmash of sovereign credits which have varying degrees of creditworthiness. We believe any attempt at a quantitative easing program by the ECB will be doomed to failure. Purchases of sovereign debt under a QE program are effectively a transfer of risk from the country to the ECB. This is a dangerous precedent that will ultimately act to speed up the demise of the euro in its current form.

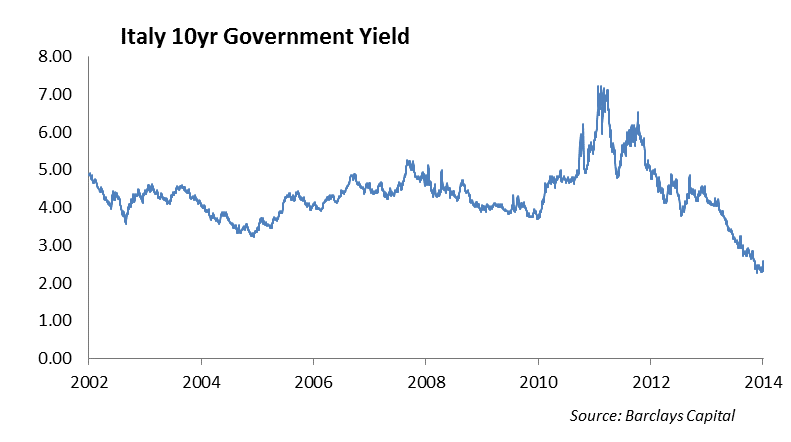

In spite of the lack of a conforming budget in 2015, Italy 10 year debt traded at a yield of 1.89% at the end of the year, a level substantially below the yield on US Treasury debt. Based on fundamentals, there is no logical explanation in our mind for Italy’s debt to trade this low. However, the market is likely discounting a bond purchase program by the ECB which will likely have some benefit to Italian bond holders.

The Recession in Russia

“Russia is a gas station masquerading as a country” – Senator John McCain

The sharp drop in oil prices combined with sanctions from the West have pummeled the Russian economy and knocked the ruble to a record low of 54 rubles to the dollar at the end of the year. We expect that Russia will slip into a recession next year and its economy to contract between 4% and 5%. Depending on the Russian government’s response to the political pressure and sanctions, the country may reverse its movement toward privatization and capitalism, which could change the face of the country over the next two years. Clearly, Russia is not going to relinquish its land grab after its invasion of Crimea and support for the rebels in the Ukraine. The Western sanctions will put pressure on Russia’s ability to finance its economy through exporting oil which will put pressure on its banks and industrial companies like Gazprom.

Barred by sanctions form European and U.S. capital markets, Russian banks are faced with plunging equity values, a sharp increase in bad loans and the mounting burden of dollar denominated debt as the ruble weakens. By the end of last year, the Russian Central Bank increased short term interest rates to 17.5% to stem the collapse in the currency and tripled the size of its bailout program for Trust Bank to $1.9 billion. The Russian government moved quickly to prop up two other banks. We expect Russia to take steps necessary to preserve its communist government at the expense of its finances.

China

China is the world’s top exporting nation and the main trading partner for many countries. China’s economy, long seen as an engine for global growth, has been hit hard this past year by a combination of slumping real estate, an increase in bad loans in its banking sector, weak domestic demand, and tumbling industrial production. In the third quarter of 2014, China’s economy grew by 7.3% from a year earlier, its slowest rate in over five years. Under President Xi Jinping, China’s leadership has laid out a path towards comprehensive reforms that are intended to introduce real market dynamics. However, there has been little to show for it in 2014 as China battles a slowing economy and heightened deflationary risks. The Peoples Bank of China cut interest rates in November for the first time since 2012. Until there is real reform, their economy remains reliant on state funded investment and exports. We expect as global demand increases over the second half of next year, China’s economy will benefit.

Summary

The lingering effects of the Financial Crisis have had a profound impact on our capital markets and economy. These effects have impacted how the capital markets operate, how banks function within the financial system, and how monetary policy is implemented. In addition, they have resulted in structural problems in our economy that have impaired sustained economic growth. These structural problems include high corporate taxes, healthcare reform, and financial regulatory reform.

We expect 2015 will be a transitional year for investors as expected returns on publicly traded financial assets are significantly lower than prior years as volatility increases. This year, we are covering our 2015 Investment Strategy in a separate publication.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2015 Winthrop Capital Management