Every year it seems to be the same. January arrives and with it the winter blahs set in. The excitement of Christmas Day has passed. The celebration of New Year’s is but a memory. We’re putting away all the holiday decorations. What a pain (literally)! And, forgive me for a parochial slip; the Lions, once again, are out of the football playoff picture and off TV.

Yes, a new year full of promise has begun, but the parties are over.

In the stock market of late, it seems no different. Just like last year, stocks stumbled coming out of the opening gate. After the first year in history (2014) without a single period of four down days in a row, the S&P reeled off such a decline (counting the last two days of 2014) to start off 2015 and then capped it by adding a fifth down day in a row last Tuesday.

And volatility, which had been at record lows in 2014, increased substantially. Every day last week saw a 100-point move in the Dow Jones Industrial Average. And the S&P 500 Index, after a breakeven day on the 2nd, still averaged a greater-than 1% daily move for the first six days of this year.

While reliving 2015’s start may seem like a gray January day with a winter storm approaching, history suggests that that’s not necessarily the case. Last year the market rallied, like this year, after starting with three down days (although after peaking on January 15th, it took twelve trading days before finally bottoming on February 3rd to mark the start of a new move to all-time highs).

Stocks have started the year off before with this level of high volatility. In fact, it has occurred 23 times since 1929. It is worrisome that almost all of the really bad years in market history began this way (like 1929, 1931, 1974, 1987, 2000, and 2008). Still, even including those years that are uglier than the snow by the side of the road a week after a winter storm, the 23-year average for the rest of the year after such a volatile beginning is positive. In fact, the median return for the rest of those years is above average – over 10%!

Our indicators remain mixed, and much depends on how fourth quarter earnings reporting (which begins tomorrow) shapes up. Earnings analysts seem pessimistic and have lowered expectations for much of last quarter, but I have found that when this happens, while they are right sometimes, more times than not earnings have surprised to the upside.

Interest rates also frustrate the Wall Street analysts. While most continue to suggest that an increase in interest rates by the Federal Reserve is imminent, we continue to believe, as we have been saying for the last few months, that the Fed is more likely to wait longer than expected before beginning the tightening process that many fear.

While a better-than-expected unemployment rate was reported last week which bolstered the rate hikers’ argument, such a view is contrary to the message being sent by weaker economic news being recorded around the world. Even in this country, which has been the strongest of the world economies, the economic reports in the manufacturing, service, and housing industries just do not appear to be strong enough to support such a Fed move.

Last week, the Chicago Federal Reserve President seemed to be agreeing with our side of the analysis. On Thursday, Charles Evans bullishly opined that, “I don’t think we should be in a hurry to raise rates.”

Further support could be gleaned from the many economic reports received last week. On the twenty reports issued, eight were better than expected but eleven were worse.

The result of these negative reports (and reflecting the negative tone of the stock market’s first few days of 2015) is that interest rates fell further. Rates continue to surprise investors by going lower, while the impression often is that everyone seems to expect higher rates to come.

As the holiday festivities have winded down and winter has reasserted itself with a polar-vortex-frozen vengeance, investor expectations have fallen like the thermometer readings. The AAII Investor Sentiment survey shows bullish investors declining in number, while the bears have increased their numbers to the highest level since… last January.

Much of the gloom seems to stem from lower oil prices. As I have written in the past, this should be a happy event for most, yet Wall Street seems to be focused on the less-than 15% of the economy negatively affected (the Energy sector), while it seemingly ignores the benefits reaped by all the rest of the population. But while the decline in oil prices has a localized effect in a single industry, the lower prices are like a tax reduction passed out to the rest of the world. Imagine the extra spending power a more-than 50% reduction in energy costs can make to the average person’s budget!

Much of the hand wringing seems to be over a concern that the lower oil prices are a reflection of lower economic activity. However, a quick review of the numbers makes clear that prices are falling because we have too much oil, not because we are consuming less oil. It’s an increase in Supply, not a reduction of Demand.

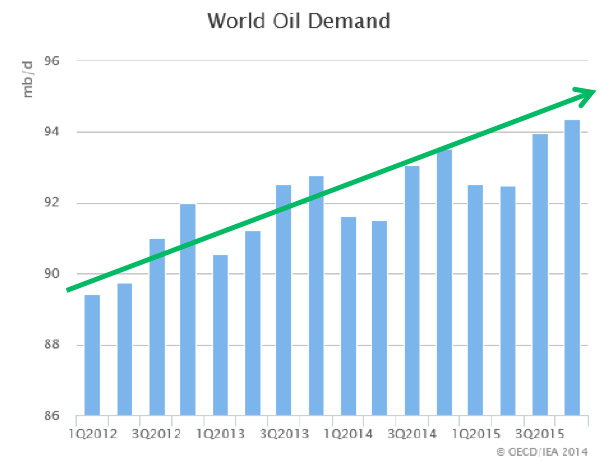

Once again in 2014 the world consumed more oil than it did in the previous year. While experts expect that there may be a pause in the first half of this year, it should be noted that even with that pause the world is consuming more oil than it did in 2012 and much of 2013. In fact, 2015’s oil consumption in its first half is expected to exceed the demand in 2014’s first half. And as the chart makes clear, the trend remains resolutely up.

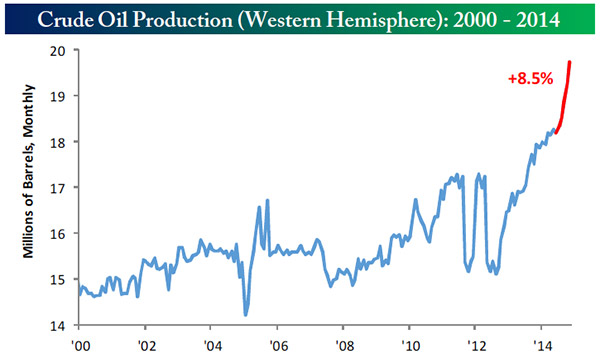

At the same time, it is obvious where the over-supply is coming from. The International Energy Association estimates that world consumption grew by 500,000 barrels a day last quarter, yet the United States by itself produced more than 1.9 million barrels more per day last year! And the curve depicting US production looks like a driller that has hit a gusher!

Bespoke Investment Group

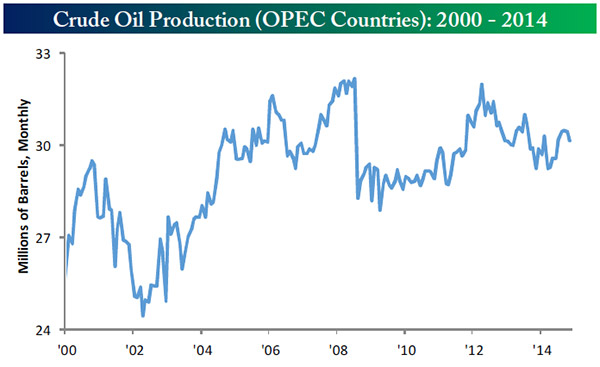

Since world oil production has actually been declining while consumption continues to increase around our planet, without the US production that continues to come online, oil prices could easily have been as high as $200 a barrel. Now, we can all agree that that such an oil price level would have a negative impact on the world economy, yet we can’t seem to agree that a more-than 50% reduction will have a positive effect!

In the end, the number-one determinate of whether or not the party is over in the stock market is the market price trend. In the intermediate term, the trend is our friend, as long as it remains up. And that is the case.

So far the dip in prices experienced has not called into question the direction of the primary ascending stock price trend. As long as that holds, we buy these dips.

That’s good, because I hear dips are an essential part of any good party.

All the best…

Jerry

http://www.flexibleplan.com/market-hotline/disclosures