A Devoted Contrarian Needs Patience

Some Recent Examples

I have an ongoing argument with one of my loyal clients. She remembers a paper I wrote on May 14, 2007, entitled, “The Boys Who Cried Wolf.” It concluded:

Many investors whose judgment and long-term performance I respect have been warning for a while that some kind of serious trauma eventually will be the price to pay for the excesses and complacency of recent years. But, as in “The Boy Who Cried Wolf” tale, their warnings have become progressively discredited as economies and financial markets brushed off successive crises. Under pressure from public opinion, the number of boys crying “wolf” has been melting like ice under the sun. But, as Victor Hugo wrote in a pamphlet against Napoleon III:

“If but one remains, I shall be that one.”

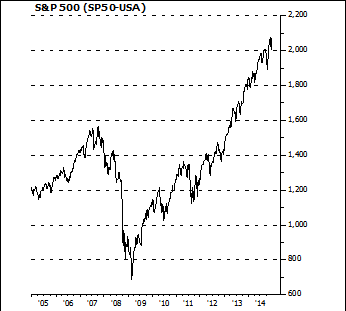

When I wrote this, the stock market was very close to its peak preceding the Great Recession of 2008-2009. Over the following 20 months, the S&P 500 Index proceeded to lose more than 50 percent of its value. We did make some adjustments to our portfolios, and in hindsight more would have been better. Naturally, my client remains convinced that, having anticipated the trouble to come, we could have sold out her investments entirely in mid-2007 and bought back in the spring of 2009. Unfortunately, it does not work that way.

First, as implied by the paragraph reproduced above, I had become leery of the stock market and the whole financial environment quite a bit earlier. I can’t remember the exact time, but if I had acted on my suspicions and sold only six months before the date of the paper, for example, the market would have gained at least another 10 percent before beginning its descent. How would my client have felt about that?

Further, professionals who correctly anticipate economic or financial trouble rarely change their minds just as the market bottoms, because that usually happens well in advance of any visible improvement in the economy. In our case, at the time the market hit its low point, in the spring of 2009, the economic and financial situation looked even more dire.

When the only thing that has visibly changed is the significantly lower price of stocks, prudent behavior from both a contrarian and a value perspective is to start accumulating stocks only slowly, rather than dive all in at what might not be the ultimate bottom. Had I previously sold out our portfolios, this is what I would have done.

In this case, just 3 months after its March 2009 bottom, the S&P 500 had already gained 38 percent. According to the National Bureau of Economic Research, this is when the U.S. recession officially ended; but, of course, that was not determined until several months later, when the recovery was obvious but the market was even higher. Casey Stengel (or was it Yogi Berra?) advised never to make predictions, especially about the future. Certainly, market timing only seems feasible in hindsight.

I was reminded that fundamental analysis and contrarian thinking are not very precise investment-timing tools upon re-reading a report I wrote on October 3, 2007: “Two Intriguing Contrarian Viewpoints: Lower Oil and a Lower Euro?”

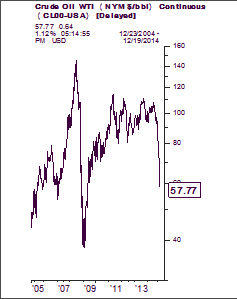

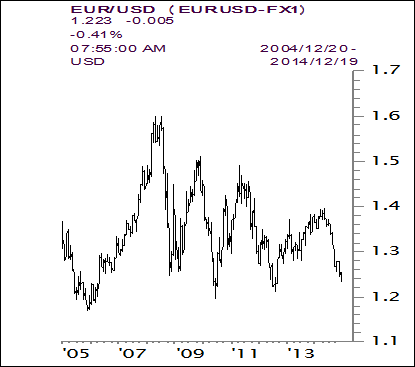

Quoting Mike Rothman of ISI Group and George Friedman of Stratfor, I considered the possibility of oil, then $81/barrel, falling to $45, and the euro, then $1.40, falling to an unspecified level (I think I may have had $1.00 in mind). As can be seen, both continued to rise in earnest for a while.

Oil rose another 80 percent, to $145/barrel, by the spring of 2008, before collapsing toward $40 in early 2009. Although it then recovered with the financial markets and the economies, it has never since returned to its 2008 high. The euro also gained another 13 percent, to $1.59, in the spring of 2008, and has been trending down irregularly since.

WTI oil recently retreated to $56, having lost 30 percent over 7 years. The euro, recently $1.22, lost 13 percent over the same period. Meanwhile, over these same 7 years, the S&P 500, for example, gained 33 percent.

I believe the argument that fundamental analysis and contrarian thinking are not precise timing tools does not need further elaboration. The more interesting question is whether, once you have developed a well-substantiated scenario, it is worthwhile to trade “around it” until it eventually materializes – sometimes after a long wait, as in these two examples.

I don’t believe so. The lack of precision in timing such events and the difficulty, in practice, of sorting out the hiccups from the start of major new trends is bound to cost more in the end than it yields.

Seeking to substantiate credible contrarian scenarios, however, remains a worthwhile pursuit.

Investing is not about magic formulae. It really is about assessing and comparing the odds of making and losing money. If the odds of making money on a contrarian scenario are too meager in comparison to the potential loss should that scenario not materialize, the exact day of reckoning is of little import. The prudent action is to stay away from a danger zone.

And contrary to a true long-term investment strategy, the most dangerous behavior is to change horses in mid-stream: to shift investment posture simply because the hoped-for scenario is unfolding too slowly. The lack of precision in picking the precise entry and exit points in an asset with a fluctuating price adds considerable cost in real life compared to the gains that we believe could have been realized in theory.

My client continues to tease me about our “lost opportunity” in 2007-2009, but I believe she has since become reconciled to the fact that I am not a magician – simply a hard-working professional whose goal is not to be right all the time, but to make fewer mistakes and less costly ones than the investing crowd. As I have said elsewhere, compound interest will take care of the rest.

François Sicart

Disclosure: This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.