Disruptive Technologies are the gold vein every entrepreneur seeks, but rarely find. Clayton M. Christensen, the patriarch of observing disruptive technologies, noted in his seminal book “The Innovators Dilemma” in 1997 that each breakthrough can be categorized as either disruptive or sustaining. We are often late in recognizing the importance of many technologies since a large percentage fall into the sustaining category. Incremental steps are much easier to quantify and therefore allow us to erroneously project a linear adoption and efficiency gains that may arise from such technology advances. When disruptive technologies occur in modern times, the combination of underestimation of the technology advance, the modern day singular distribution and resulting viral contagion as well as the basic nature of herd migration often results in profound transformation in short order.

We have witnessed some of these recently:

· Apple’s new pay system appears to be a technology advance that is similar to the iPod but with far bigger economic gains. By utilizing its reach along with grabbing the potential gains of each financial transaction, one gets the sense that by the time competitors catch up, they will be battling for a small group of those who didn’t utilize this advance.

· Lockheed Martin has now “claimed” to have had significant advances in cold fusion technology that appear to promise free perpetual energy for eternity. Though they were heavy on headlines and short on details (and doubters are right to be skeptical), it too would fall into the category of a disruptive technology.

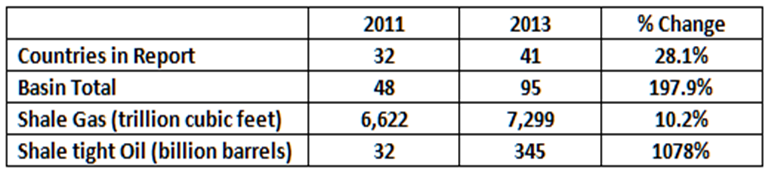

· In oil, one need only to look at the difference in the EIA (Energy Information Administration) report from 2011 to 2013. In just two years, a significant increase in potential resources was found as well as new basins.

When a disruptive technology hits an archaic industry, prices and promises often have a volatile reaction. We have seen a near 50% correction in oil prices although the supply glut is a fraction of this. The technology improvements in finding and extracting oil has been known for some time, however when it hit the markets, the prognostications of energy’s demise have picked up. This is a natural reaction of human nature and has its converse when the perma-bull crowd yells “it’s different this time”.

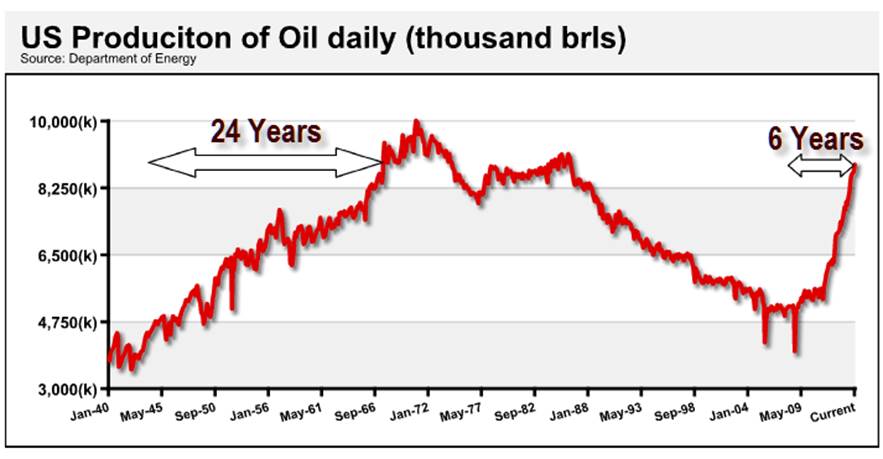

Consider what has happened here recently in the United States from a production of barrels per oil daily over the last 75 years. The recent shift in production took only 6 years to achieve in what initially took 24 years to accomplish (1943 to 1967). When an economy and market has time to acclimate itself, it can be described as a sustaining technology. I believe what we have seen here recently is a disruptive advance.

The easy answer is to firmly state that this changes everything and oil is in the grip of a paradigm shift of lower prices for a longer period of time. Occam’s razor (if multiple theses exist, choose the one with least complications or most simple) would tell you that this easy choice of projecting current trends would be reasonable, however one underlying principle of oil combats this. High oil prices typically reduce high oil prices as consumers shift their pain at the pump to less painful public transit or carpooling behaviors. Thus the slight reduction in gas or oil causes the finding of a level. (In other words, when oil prices begin to drop, a significant stimulus is passed through to its consumers and demand picks up.)

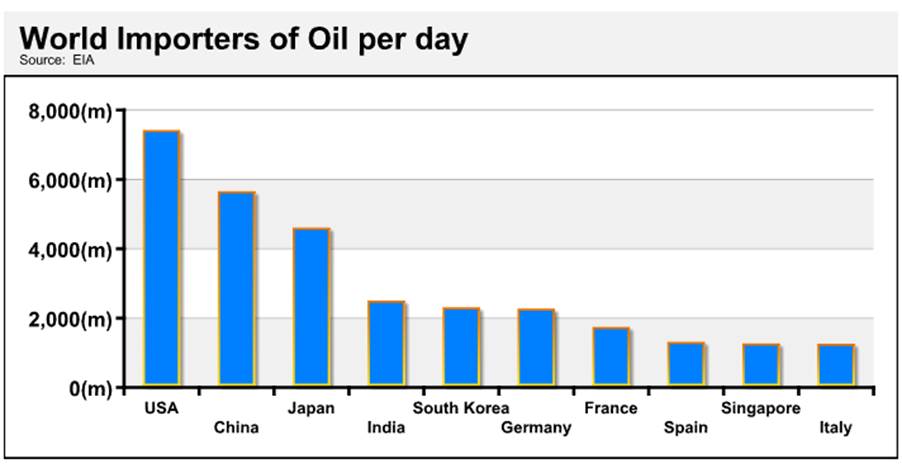

One condition that is being underestimated is the potential for an accelerated pick-up in growth in Europe as the Euro drops and they possibly move from a hushed breath of growth to a larger increase in the coming year. The top 10 importers all look to have a substantial stimulus passed through to consumers and businesses. Even though the US (as of 2012) was the largest importer, our increased production creates a positive energy gap and has a continued positive growth impact as efficiency in energy transfers domestically creates both stimulus and production profits simultaneously.

Excluding the US on the list below, nine countries comprise over $27 trillion of global GDP, or 37%. Though it will be disruptive to certain parts of the globe, namely the Middle East, Russia and Venezuela to name a few, the stimulus to other parts of the world looks to be substantially underestimated.

2014-1208-4552 R

© AAM