I wrote often throughout 2014 about the danger signals flashing from an excessive run up in debt and derivatives. We have a repeat of the scenario we suffered in 2008, only much worse (Watch Junks Bonds For Early Warnings Of New Financial Crisis, Forbes). The budget recently passed by Congress put taxpayers on the hook for a 2008-like derivatives failure. The potential losses could exceed the previous financial meltdown as other world market conditions exacerbate a bad situation.

As a risk manager, I need to acknowledge and plan to mitigate these big, macro risks. At the same time, as a tactical manager, I acknowledge that right now the weight of evidence points to a continued positive trend for this mega bull market.

In a world of excessive debt and unprecedented Central Bank intervention, where is a global investor to go? For now, the best place remains in U.S. equities.

Global debt continues to be the #1 concern going into 2015. A sovereign debt crisis looms on the horizon yet for now the creativity of global central bankers has kicked that can down the road. It is desperation time in Japan and the Eurozone is not far behind. A number of factors favor the U.S. dollar and U.S. equities through mid-2015.

My snapshot 2015 investment outlook:

The Fed & Interest Rates

- Expect rates to be modestly higher in 2015.

- In comparison to a historical average of 3.3 percent annual GDP growth, my expectation of 2.8 percent growth is enough to keep the Fed on track to raise rates for the first time in June 2015.

- North America remains the primary growth engine to the world. Particularly the U.S.

- The wind shifts in the second half of the year as the probability of the second Fed interest rate increase occurs. This could happen in September or October 2015. Bull markets tend to end after the second Fed rate increase.

U.S. Stocks & Bonds

- Ultra low fixed income yields favor equities over fixed income. Despite today’s high valuations, the strong U.S. equity bull market continues through mid-2015.

- The third year of the presidential election cycle is historically bullish for stocks (especially the first half).

- Global capital flows favor U.S. equities and U.S. real estate.

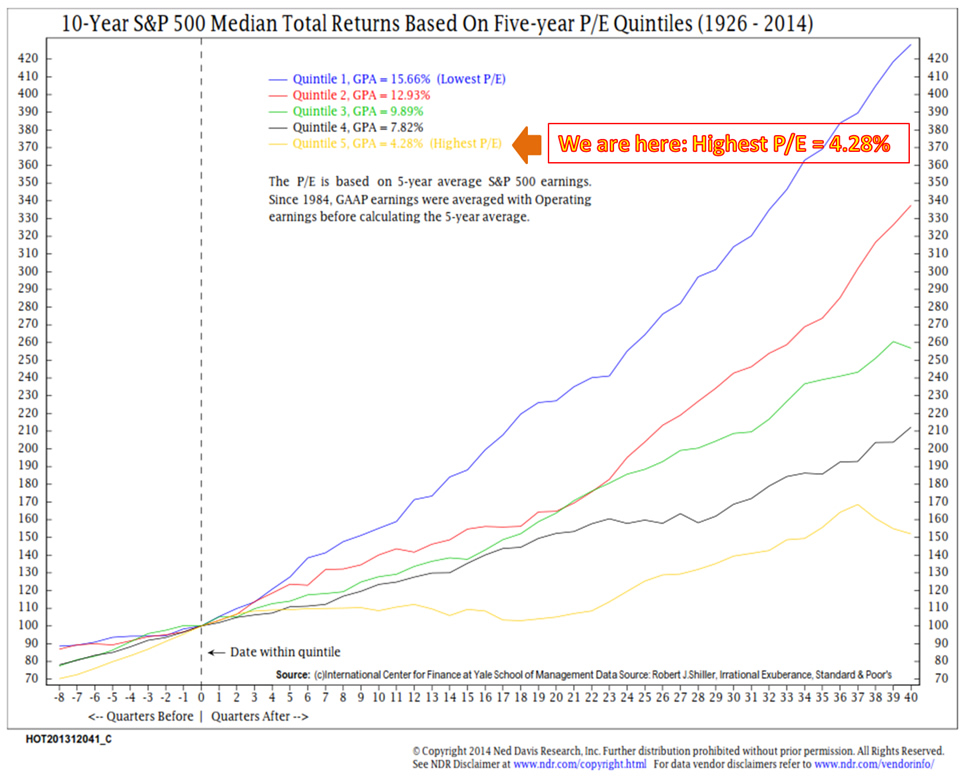

- There are a number of risks: Geopolitical. Crisis in high yield debt. Margin debt is at the highest level in history. U.S. stock valuations are high. At a median PE of 21.2, current valuation puts the probable forward 10-year S&P 500 Index return at just 4.28%. Historically, the lowest performing quintile (yellow line).

- The chase for yield has flooded the high yield market with money to invest. Less credit worthy companies found it easy to borrow and at terms far less favorable to investors. A high yield bond market default wave begins in 2015 and lasts for several years (See Code Red In High Yield, Forbes, 7/25/2014).

- We are 5.75 years into the bull market that began in 2009. Compared with bull markets from 1923 (5.83 years), 1994 (5.75 years) and 2002 (5.0 years), this bull is aged. Couple this with low probable 10-year forward returns and you have a higher risk environment.

- For now, the U.S. economy is holding up the world but the U.S. is not immune to the deflationary pressures that grip much of the global economy. Debt is the problem.

- A sovereign debt crisis likely drives the next financial crisis: a global economic crisis that rivals the 2008 global financial meltdown. My best guess? Beginning in late 2015 or 2016.

There is more than $700 trillion in bank created synthetic derivatives. It exists in an intricate web of entangled global counterparty risk. The concentration of such risk lies in the hands of just a few large banks. One has to wonder to what degree a sovereign debt crisis or other unknowing event might trigger another major financial crisis. It is unnerving that the banks were able to get Congress to pass a bill that puts the U.S. taxpayer on the hook for bank losses related to the banks’ derivatives holdings.

Global Macro Views

- As QE ends in the U.S., interest rates here will rise while rates in Japan (recession and early QE) and the Eurozone (deflation and probable QE) will fall relative to U.S. rates. Additionally, it is widely expected that the Fed will begin to normalize interest rates in June 2015. Both the Yen and Euro offer less favorable interest rates and are early in their QE program. This favors the U.S. dollar over Yen and Euros.

- The Eurozone is in decline economically and is dysfunctional politically. Global investors will continue to see U.S. real estate and equity markets as better investment options. Further, a sovereign debt crisis will cause capital to race into U.S. dollars and U.S. assets. Equities are favored over bonds.

- Japan is now “all in” on QE, which is negative for the Yen but positive for Japanese equities. At 250 percent debt to GDP, Japan has reached a crisis phase. Their plan is to devalue the Yen. This is not viewed favorably by Korea, China or Europe. In 2015, the global trade and currency wars intensify.

- Global pension plans are significantly underfunded and meaningfully exposed to low yielding sovereign debt. A debt reset (default/restructuring) is the probable outcome.

- Underfunded pensions, with exposure to such debts, will be forced to restructure. A pension crisis follows the sovereign debt crisis.

- Global banks are exposed to sovereign debt. EU regulators have made it attractive for banks to own sovereign debt as banks do not have to hold any capital against their holdings of government debt. A banking crisis follows the sovereign debt crisis.

- Japan is center stage and the Eurozone is up next. Trade tensions and currency battles mount. None of this is favorable for global growth. Slow global growth and deflation are likely to continue.

The global central banks have embarked on a grand experiment of unimaginable proportion. But it is wise to remember too that bankers are human. Greenspan shared in his book that his problem as Fed chair was that he just didn’t know about the flood of junk mortgages that fueled the unprecedented risk in housing prices during the bubble years. He offered this reason to explain his lack of action about the risks posed by the bubble.

The Guardian explains, “Greenspan’s ‘I didn’t know’ excuse is so absurd as to be painful. The explosion of exotic mortgages in the bubble years was hardly a secret. It was frequently talked about in the media and showed up in a wide variety of data sources, including those produced by the Fed. In fact, there were widespread jokes at the time about ‘liar loans’ or ‘Ninja loans.’ The latter being an acronym for the phrase, ‘no income, no job, no assets’.”1

Japan is in desperation mode. Europe is following quickly behind. The Fed has printed trillions of dollars and has meaningfully participated in our markets. It has kept interest rates at near zero percent for six years. QE has become the global medicine of choice. There will be unintended consequences.

Here are some things you can do to participate in the market’s upside while protecting yourself from the next market crisis.

- Overweight equities but put a stop loss process in place to protect yourself from a -40 percent or more decline. Placing a stop loss just below an ETF’s 200-day simple moving average can help.

- The following graph looks at a 13-week over a 34-week exponential moving average. If you are invested in an S&P 500 index ETF such as “IVV”, “VOO” or “SPY”, when the 13-week (blue) line declines below the 34-week (red) line, sell NYSE “SPY” or “IVV”, switch to a lower volatile S&P 500 index like “HSPX” (it uses covered calls) or move more defensively to iShares 1-3 year Treasury ETF symbol “SHY”.

- Favor large caps over small caps. I like the following sectors: Technology via iShares, U.S. Technology ETF “IYW”, Healthcare “IYH” and Consumer Staples “KXI”.

- Look to include tactical all asset, tactical equity and tactical fixed income strategies in your portfolio. These strategies offer disciplined buy and sell processes that can help you further mitigate portfolio risk. Remember that broad diversification coupled with sound risk management remains the best path over time.

In summary, capital continues to flow into dollars, supporting a favorable view of U.S. equities. Trend evidence remains positive. A reasonable guess puts the S&P 500 index at 2350 by mid-2015 (a gain of approximately 15 percent). But it is really just a guess – much is dependent on capital flows and the timing of developing sovereign debt default worries. Markets move on supply and demand. I see more demand than supply for now.

Overweight U.S. equities, but keep in mind that valuations are high and the bull market is aged as is favorable Fed policy. Risk remains high. Corrections happen quickly and absent a plan, recall that a 50 percent decline can wipe out all the gains made over the last few years. Further, it will then take another 100 percent gain to get back to even and that takes time. As we well know, meaningful declines can happen.

As with all predictions, it is smart to remain balanced. I remember the 35 Wall Street analysts who, this time last year, on average predicted the yield on the 10-year Treasury would rise from then 2.99% to 3.25% by the end of 2015. Here we stand at 2.12%. Not one analyst thought the yield would be below 2.90%. They all missed.

One of the best performing assets of the year, the iShares 20+ Year Treasury Bond ETF “TLT” is up 24% through December 16. I too believed rates would rise; however, despite my fundamental view, our bond positioning process kept us invested in bonds. Keep this in mind when you look at expert opinions. They are probability based and come with no guarantees. It is best to broadly diversify your risks, overweight to areas that look most promising and incorporate a disciplined process that limits your downside and can keep you participating in the upside just in case your view or mine is wrong.

I see a strong first half for 2015 with a potential tipping point in late 2015. The trigger could be a sovereign debt crisis, successive Fed rate increases, an unexpected shock in oil prices or something we just don’t yet know. The point is that systemic risk is high and a 2008 crisis-like event is probable in the near future. If valuations were in quintiles 1 or 2 (as presented in the chart above) the story today would be entirely different. I believe we’ll see those quintiles within the next few years.

The good news is that market crisis creates outstanding opportunity. With a risk management plan in place, you will have the liquidity that will enable you to take advantage of the opportunity that the next crisis creates and it may just help you sleep more peacefully at night.

Here’s to a great 2015. Stay tactical!

© CMG Capital Management Group

© CMG Capital Management Group