The price of oil has plummeted this year as a result of increased volatility in most markets and a temporary imbalance of supply and demand. In view of continued long-term world growth, particularly in emerging- and frontier-market countries, we believe oil prices will probably not suffer from a prolonged price slump. As we see it, the demand for raw materials in general, including not only oil but also iron ore, copper, nickel and agricultural products, is still likely to increase over the long term with increased global growth. Much of the velocity of the recent oil price drop, we think, is based on speculation and short-term trading. In our view, the price of oil is likely to rebound in 2015 or 2016.

In the past two months, crude oil has experienced its biggest price slump since the 2007–2009 global financial crisis, with a number of reasons cited, including slowing demand growth from major economies and increased output from the United States in the past few years that hasn’t been met with decreased production among other major oil producers.

Certainly, too much supply, if it continues, will impact prices—that’s just basic economics. However, when we look at long-term demand patterns, we see the overall trend has been up, not down, and we can see how emerging-market economies have been driving this growth.

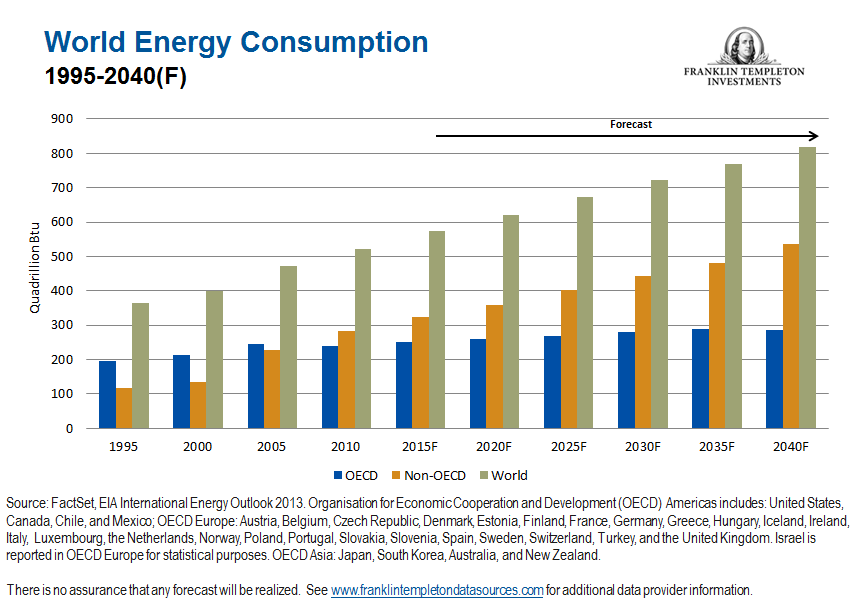

The Organisation for Economic Cooperation and Development (OECD) is a forum that facilitates cooperation among the governments of 34 member-democracies with market economies to promote economic growth, prosperity and sustainable development. Most emerging and frontier markets are non-OECD members, including China and India. The chart below shows how non-OECD countries have already surpassed the OECD countries in terms of crude oil consumption, and the gap is forecast to widen in future years.

China: Growing—or Slowing?

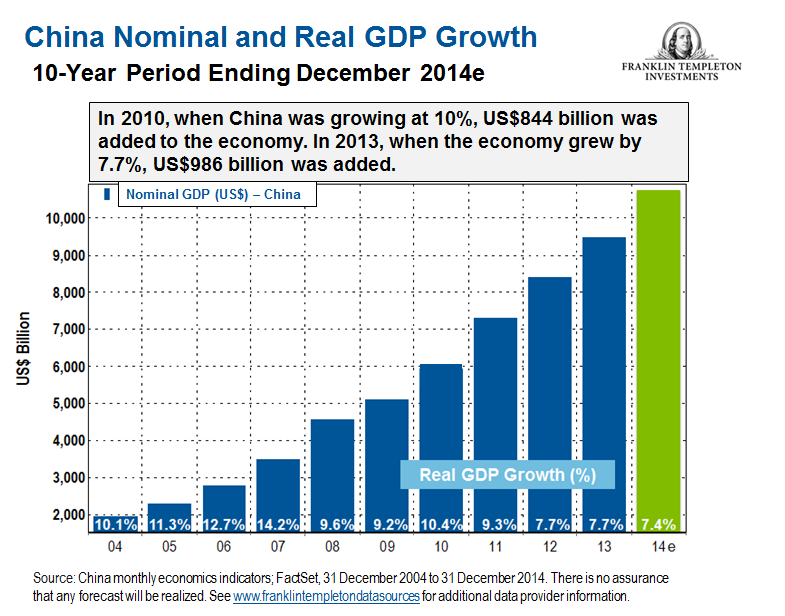

Slowing growth in China has been cited as a reason behind the drop in oil prices, but we look at the situation a little differently than many. Sure, its gross domestic product (GDP) growth is no longer in the double-digits of times past, and that’s to be expected because China’s economy is growing—it now has a higher baseline. I don’t think growth in China is a problem. In 2010, when China was growing at about 10%, US$844 billion was added to the economy. In 2013, growth had slowed to just under 8%, but more than US$900 billion was added to the economy. So, yes, GDP growth has been smaller percentage-wise, but you have to look at the overall economic impact—the US dollar figures.

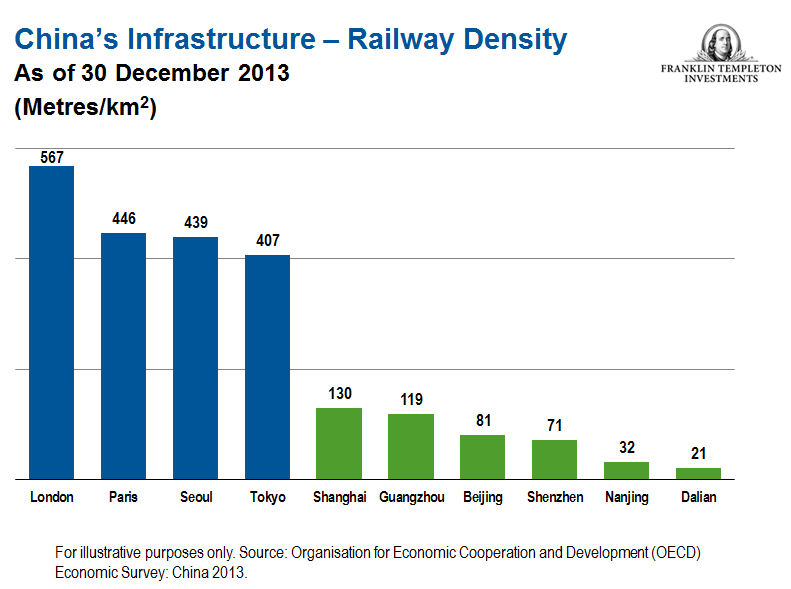

Additionally, many people don’t think China needs more infrastructure, but from my personal experience traveling around the country on packed trains and heavily trafficked roads, it needs it badly! Urbanization is still underway; there is still a lot to be done in China, and it will still need natural resources to do it.

Impact of Lower Oil on Emerging Economies

Most consumers naturally cheer lower energy prices, but looking at overall economic impacts, lower oil prices can be a double-edged sword. In countries that are heavily dependent on oil exports, a prolonged oil price slump could be harmful.

Nigeria’s government, for example, depends on oil for a large part of its budget; the oil and gas sector accounts for about 35% of GDP, and petroleum export revenue represents over 90% of total export revenues.1 If these revenues drop, Nigeria’s leaders would either have to suffer through a lower oil price spell, or do something to revive the economy through diversification and reforms. Among the world’s top exporters, Russia’s GDP fell 8% in 2009 as the price of oil plunged below US$40 a barrel amid the global financial crisis. Russia remains heavily dependent on energy revenues today, and the country seems likely to be impacted greatly if prices don’t rebound quickly enough. Combined with Ukraine-related sanctions, Russian government officials have predicted a possible recession in 2015. Also highly dependent on oil revenues, Venezuela also seems particularly vulnerable, in our view. Saudi Arabia seems likely in a better position to weather the price downturn, as Saudi Arabia has enormous foreign reserves and investments that we believe should enable it to continue spending and growing even with low oil prices. On the flip side, China and India, as net importers, are likely to benefit from lower oil prices.

Part of the increased supply of oil has come from increased US shale production. At levels under US$60 a barrel, extracting oil becomes less profitable to shale producers. As it becomes unprofitable, some production will likely shut down, although it may take a number of months for fields to be abandoned. Meanwhile, the demand for oil in the two most populous countries in the world (China and India) is increasing as a result of more cars, buses and trucks on the roads. In addition, plastics and many other widely used products are derived from oil. The cost of finding and producing oil has not generally been declining. Therefore, over the longer term, we think oil prices will recover.

We see another side to the lower oil price story that is potentially positive for some emerging economies that had been subsidizing energy. These subsidies were a drag on government budgets, and lower market prices make removing such subsidies less painful for consumers residing in those countries. Indonesia has removed some subsidies, and we see signs that India and China are moving in that direction as well. An environment of lower energy prices has helped some emerging countries embark on much-needed reforms with less painful effects.

Right now, we think perhaps the biggest concern from an investment standpoint is volatility, not only in the price of oil but in related stocks in the sector—and in equity markets generally. We’ve seen some incredible swings. We look to use the downturns to find potential bargains for our portfolios, but many investors get spooked and lose out on opportunities. We, of course, will be looking at those countries, sectors and companies that we think could benefit from lower oil prices. We are not avoiding oil companies completely right now, however. Since many such companies are diversified, they may suffer in terms of their exploration and production activities, but could potentially benefit from their retail activities.

Mark Mobius’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Investments in the energy sector involve special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector.

© Franklin Templeton Investments