Encore Unlikely

- 2014 performance unlikely to be repeated

- 2015 Fed rate hike fears overblown: remain “constructive but cautious”

- Credit concerns on the radar

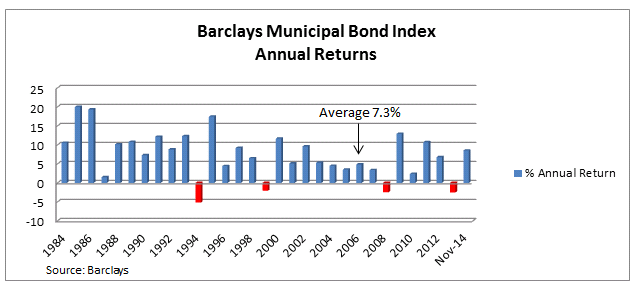

What a difference a year can make. Negative performance returns rendered 2013 a very difficult one for bond investors, only the fourth sub-par occurrence over the past 30 years, as measured by the Barclays Municipal Bond Index. Heading into 2014, the consensus called for a further lift in yields based on the widely held belief the Fed would begin to move away from its near-zero rate policy.

However, this year has once again attested to the adage, “The market will move in the direction that will cause the most pain - for the most investors.” Bearish positioning through the early months of the year left many investment managers lagging their performance bogeys, necessitating performance-chasing capitulation by mid-year when geopolitical tensions began to escalate around the globe and signs of economic weakness materialized in Europe and some emerging markets. The upward march in security prices was orderly and impressive, as evidenced by an uninterrupted succession of monthly price gains; volatility was largely absent except in the high yield arena where credits from various Puerto Rico issuers, Detroit, and tobacco-backed bonds experienced considerable volatility. Comparatively calm conditions in the fixed income markets, led by an investor “flight to safety” into U.S. Treasury securities, contrasted with the heightened volatility in the equity and commodity arenas. The more recent collapse in global oil prices has caused further anxiousness. It appears financial markets are now coming to grips with the reality of a sustained decline in world petroleum prices and the resulting ramifications. Beneficiaries will include U.S. consumers who will have more disposable income for discretionary expenditures. Globally, deflation, not inflation, is now more of a threat globally as commodities cheapen. The negative impact on some currencies will likely lead to further economic weakness, particularly in oil-producing nations such as Russia.

While many economists remain steadfast in the belief that short-term rates will begin moving higher by the middle of next year, we still think the Fed will remain on hold for a considerably longer period of time. The Fed operates under a two-pronged mandate: maximize employment and maintain price stability. The transcript from last week’s final FOMC meeting of the year states that the central bank will remain “patient” in determining when to begin the process of normalizing short-term rates. Based on the stock market’s positive reaction to this announcement there should not be near-term concern. Certainly, the latest readings on CPI inflation should not raise any worries about rising consumer costs. The U.S. jobless rate continues to drop but is still not at a rate signaling full employment.

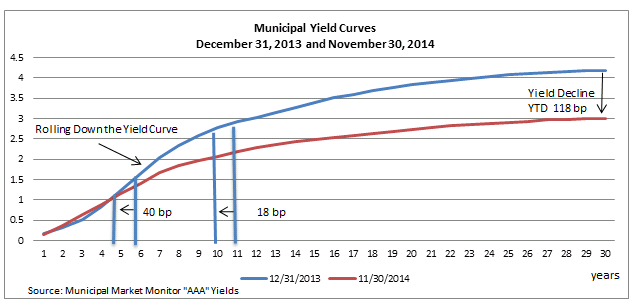

Market performance in 2014 was driven by a variety of factors. Not surprisingly, the biggest move in yields was registered by the longest maturity securities. As depicted in the graph below, ”AAA”-rated bonds maturing in thirty years experienced a decline of 180 basis points (1.80%). Yield declines narrowed for intermediate term securities and the spread was almost negligible for the shortest maturities. An additional source of return in 2014 resulted from bonds increasing in price due to the “roll-down” effect due to the shortening of maturity as bonds age. The impact was approximately 40 basis points for short-term issues and less for longer-dated bonds. Given the low level of rates, income-oriented investors, continue to stretch for additional income through the purchase of lower-rated issues. This activity causes a further compression in quality spreads which has proven to be a significant driver of performance.

We are maintaining a constructive market view, at least through the first several months of the new year. However, investors should be preparing for greater market volatility and less portfolio price appreciation. With bond yields close to generational lows, risk is asymmetrical: odds favor higher yields by the end of 2015. The timing and extent of the rate climb will continue to be extensively debated. Given the anticipated directional bias, we will continue to position accounts more defensively versus the benchmark through a combination of duration, maturity, coupon, and credit structuring.

“Constructive but cautious” is our 2015 mantra. Price appreciation has been a major contributor to portfolio performance as evidenced by the yield curve shift from the beginning of the year. Through November the Barclay Index has returned 8.50%, with almost identical contributions from higher security valuations and coupon income. 2015 market performance should largely be determined by income, with less support from declining yields. Our management strategy will be steered by generating the best combination of income, while maintaining risk exposure (duration) less than the benchmark. In anticipation of a lift in short-term rates, optimal portfolio exposure should be concentrated where maturity roll-down can be optimized. Considering at credit quality, the differential between the highest and lower-rated bonds has narrowed in the rally of 2014; we anticipate a reversal next year.

There should be an ample supply of new bond issuance over the next twelve months. Industry analysts estimate $335 billion of new municipal securities will come to market, slightly above 2014’s supply. Additional issuance could materialize in the form of infrastructure bonds since state and local revenues have regained better financial stability. Underfunded governmental pension plans are a growing problem for many states such as New Jersey, Kansas and Illinois. Newly enacted pension accounting rules, requiring more conservative earnings assumption for public pensions, will magnify the underfunded status that exists in other states. More tax-exempt borrowing could be the solution utilized to shore up underfunded plans.

Tops among the major municipal credit stories in 2014 were Detroit and Puerto Rico. Detroit just emerged from bankruptcy. Uncertainty surrounding the status of various Puerto Rico issuers has quieted down since mid-year and debt prices have stabilized. However, early next year, the Commonwealth will be looking to sell $3 billion of bonds issued by the Industrial Finance Authority (PRIFA) as well as the restructuring of its Electric Power Authority Bonds (PREPA). Anticipate more news and trading volatility when these new issues are marketed.

Add “oil-related” to the mix of possible municipal credit stories. The positive effect of sustained lower energy costs will translate into stronger consumer spending and a resulting lift in state and local sales tax revenues. Long-neglected infrastructure could get a boost if Congress raises the federal gas tax to bolster the Federal Highway Trust Fund. States relying on oil and related services will merit close credit monitoring.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the security transactions listed were or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.