Completing the Alternative Investments Puzzle: Putting the Pieces Together

In my previous blog, I discussed why I believe advisors and investors should approach alternative investments much like a jigsaw puzzle and offered an organizing framework that can help. When putting together a puzzle, the first step is to sort and organize all the pieces. For alternatives, the first step is to organize and align the various alternative strategies with specific investment objectives. This step is critical because it helps investors decide whether alternatives can help them meet their needs, and, therefore, whether they should invest in them.

Organizing the pieces and deciding whether to invest is just the beginning, of course. The next step is to start clicking the pieces into place within a broader portfolio. In this step, the question becomes how to fund the allocation — in other words, where do you take money from in order to put it into alternatives? This is where puzzle-makers have the advantage — there’s only one spot for each jigsaw piece. In a portfolio, choices must be made. But how?

It’s a complicated subject, and one that investors should always discuss with their advisors. As a general rule, I believe investors should base this decision on the return and risk characteristics of the alternative they want to add. By that I mean, I would first consider allocating away from fixed income to fund an alternative investment that had fixed income-like return and risk characteristics. The same would be true for equities.

Let’s look at different ways to allocate to alternatives using the framework as our guide:

• Objective – Inflation mitigation

Real estate investment trusts (REITs), commodities, master limited partnerships (MLPs) and infrastructure have historically performed well in inflationary environments. Given that these alternative assets typically have had equity-like return and risk characteristics, investors, who meet certain risk criteria, could first consider allocating away from equities in order to fund an allocation to these assets.

• Objective - Principal preservation

As discussed in my first blog, relative value strategies such as market neutral seek positive returns in different market environments. Given that these strategies typically have had bond-like return and risk characteristics, investors, who meet certain risk criteria, might consider allocating away from bonds to fund this allocation.

• Objective -Portfolio diversification

Global investing and trading strategies such as global macro, risk balanced and multi-alternative may potentially help buffer a portfolio if stocks and bonds fall in tandem. Given that these strategies typically have generated stock-like returns with significantly lower levels of risk than stocks, investors, who meet certain risk criteria, could consider allocating away from equities to fund the allocation.

• Objective – Equity diversification

Alternative equities strategies such as equity long/short or unconstrained equity may help investors diversify their stock exposure. Given that these strategies have tended to generate equity-like returns with lower risk than traditional stocks, investors might consider allocating away from equities to fund the allocation. Furthermore, given the potential high correlations between equities and alternative equity strategies, some investors, who meet certain risk criteria, may view alternative equity as a core part of their equity allocation.

• Objective – Fixed income diversification

Bank loans, unconstrained fixed income and long/short credit can help diversify a traditional bond allocation. Given that these strategies have return and risk characteristics similar to that of bonds, investors may consider allocating away from fixed income to fund the allocation. Similar to investor attitudes about alternative equity, some investors, who meet certain risk criteria, may view alternative fixed income as a core part of their fixed income allocation.

Of course, the above discussions are pretty straightforward if an investor holds just one of the five major investment objectives. Life isn’t always that straightforward, and investors often have goals that necessitate a combined approach. Two common investor goals are below:

• Goal – Generate increased current income

To pursue this goal, investors, who meet certain risk criteria, may consider allocating to 1) alternative assets that generate current income (i.e. REITs, MLPs, and infrastructure), and 2) alternative fixed income strategies that generate current income. In order to fund the allocation, the alternative assets portion could be funded from the portfolio’s equity allocation and the alternative fixed income portion could be funded from traditional bonds.

• Goal – All-weather allocation to alternatives

A potentially “all-weather” allocation to alternatives is one that allocates across the five different buckets shown in the framework, either on an equal-weight basis, or emphasizing certain categories over others. In order to fund the allocation, investors, who meet certain risk criteria, could consider funding the alternative asset, global investing and trading, and alternative equity allocations by investing away from equities. The relative value and alternative fixed income allocations could be funded by allocating away from fixed income.

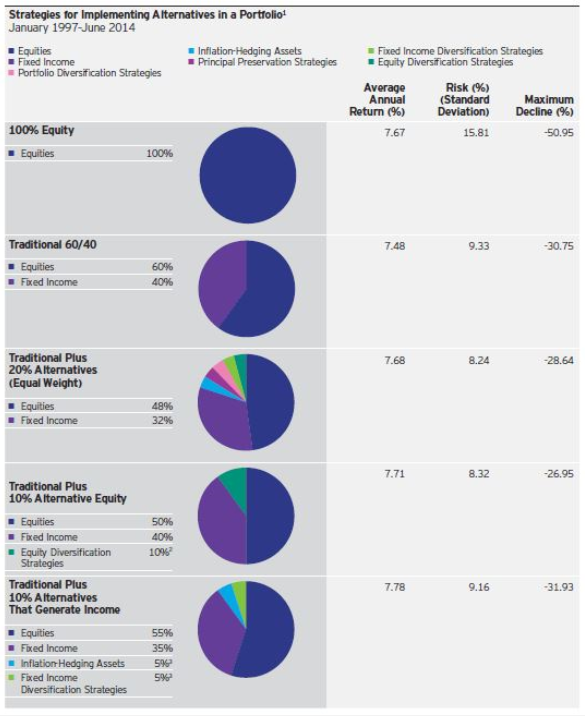

There are a variety of ways advisors and investors can allocate to alternatives, several of which are highlighted above. In addition, the charts below compare a 100% equity portfolio and a 60% stock/40% bond portfolio with:

• The impact of the all-weather approach, shown by the “traditional plus 20% alternatives” pie.

• The equity diversification approach, illustrated by the “traditional plus 10% alternative equity” pie.

• The current income approach, shown by the “traditional plus 10% alternatives that generate income” pie.

To me, the key when allocating to alternatives is to align the different types of alternatives with specific client objectives in order to best achieve those objectives. Please keep in mind that the chart below is for illustrative purposes only and that it is not representative of any particular investment or strategy. There is no guarantee that the strategies described will meet income, performance or volatility objectives described. Past performance is not a guarantee of future results.

1 Inflation-Hedging Assets represented by FTSE NAREIT All Equity REIT Index, Dow Jones UBS Commodity Index and Alerian MLP Index. Principal Preservation Strategies represented by BarclayHedge Equity Market Neutral Index; Portfolio Diversification Strategies represented by BarclayHedge Global Macro Index, BarclayHedge Multi-Strategy Index and BarclayHedge Currency Traders Index; Equity Diversification Strategies represented by BarclayHedge Long/Short Index; and Fixed Income Diversification Strategies represented by Credit Suisse Leveraged Loan Index, HFN Fixed Income Arbitrage Index and BarclayHedge Fixed Income Arbitrage Index. Equities represented by S&P 500 Index. Fixed income represented by Barclays U.S. Aggregate Bond Index. An investment cannot be made directly in an index. Past performance is not a guarantee of future results. Risk is measured by standard deviation.

2 Equity Diversification Strategies represented by 10% BarclayHedge Long/Short Index.

3 5% Inflation-Hedging Assets represented by 2.5% FTSE NAREIT All Equity REIT Index and 2.5% Alerian MLP Index; does not include commodities. 5% Fixed Income Diversification represented by 1.66% Credit Suisse Leveraged Loan Index, 1.66% HFN Fixed Income Arbitrage Index and 1.67% BarclayHedge Fixed Income Arbitrage Index.

Important information

Alternative products typically hold more non-traditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Investing in infrastructure involves risk, including possible loss of principal. Portfolios concentrated in infrastructure securities and MLPs may experience price volatility and other risks associated with non-diversification. Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.in which those investments are traded.

There is a risk that the value of the collateral required on investments in senior secured floating rate loans and debt securities may not be sufficient to cover the amount owed, may be found invalid, may be used to pay other outstanding obligations of the borrower or may be difficult to liquidate.

The dollar value of foreign investments will be affected by changes in the exchange rates between the dollar and the currencies in which those investments are traded.

Diversification does not guarantee profit or eliminate the risk of loss.

Volatility is the annualized standard deviation of returns.

Downside risk is the maximum decline based on the month end value of the index or portfolio.

Correlation indicates the degree to which two investment have historically moved in the same direction and magnitude.

Relative value strategies seek to provide positive returns above cash in all market environments, typically with lower volatility than the broad market. They generally employ arbitrage techniques to capture pricing anomalies by purchasing undervalued assets and shorting overvalued assets. The success of these strategies is driven by the managers’ security selection and strategy execution, as they seek to profit from the relative value created by the price differentials in the related securities.

Long positions make money when an investment rises in price.

Short positions make money when an investment falls in price.

Market neutral strategies use offsetting long and short stock positions in an attempt to limit non-stock-specific risk.

Macro strategies base their investment decisions on macro views of various markets around the world. They may take long and short positions within and across such asset classes as equities, fixed income and currencies.

Also known as risk parity strategies, risk-balanced portfolios are constructed so that each asset contributes a relatively equal amount of risk to the strategic allocation of the portfolio. These portfolios may also include a tactical overlay that allows managers to opportunistically adjust the strategic allocation.

Multi-alternative strategies invest in a number of different types of nontraditional asset classes and strategies.

Long/short strategies (equity or credit) typically take both long and short positions to benefit from rising prices on the long side and declining prices on the short side.

Unconstrained strategies (equity or fixed income) may seek returns in a variety of ways, including the creation of long/short exposures or the implementation of an unconstrained approach that allows the managers to pursue their best ideas across the equity or fixed income markets.

The FTSE NAREIT All Equity REITs Index is an unmanaged index considered representative of US REITs. The Dow Jones UBS Commodity Index is designed to be a liquid and diversified benchmark for the commodity futures market. It is a rolling index composed of futures contracts on 19 physical commodities traded on US exchanges. The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology. The BarclayHedge Equity Market Neutral Index includes funds that attempt to exploit equity market inefficiencies and usually involves being simultaneously long and short matched equity portfolios of the same size within a country. Market neutral portfolios are designed to be either beta or currency neutral, or both. Well-designed portfolios typically control for industry, sector, market capitalization, and other exposures. Leverage is often applied to enhance returns. Only funds that provide net returns are included in the index calculation. The BarclayHedge Global Macro Index includes funds that carry long and short positions in any of the world’s major capital or derivative markets. These positions reflect their views on overall market direction as influenced by major economic trends and or events. The portfolios of these funds can include stocks, bonds, currencies, and commodities in the form of cash or derivatives instruments. Most funds invest globally in both developed and emerging markets. Only funds that provide net returns are included in the index calculation. The BarclayHedge Multi Strategy Index includes funds that are characterized by their ability to dynamically allocate capital among strategies falling within several traditional hedge fund disciplines. The use of many strategies, and the ability to reallocate capital between them in response to market opportunities, means that such funds are not easily assigned to any traditional category. Only funds that provide net returns are included in the index calculation. The BarclayHedge Currency Traders Index is an equal weighted composite of managed programs that trade currency futures and/or cash forwards in the inter-bank market. The BarclayHedge Long/Short Index includes funds employ a directional strategy involving equity-oriented investing on both the long and short sides of the market. The objective is not to be market neutral. Managers have the ability to shift from value to growth, from small to medium to large capitalization stocks, and from a net long position to a net short position. Managers may use futures and options to hedge. The focus may be regional or sector specific. Only funds that provide net returns are included in the index calculation. The BarclayHedge Fixed Income Arbitrage Index includes funds that aim to profit from price anomalies between related interest rate securities. Most managers trade globally with a goal of generating steady returns with low volatility. This category includes interest rate swap arbitrage, US and non-US government bond arbitrage and forward yield curve arbitrage. Only funds that provide net returns are included in the index calculation. The BarclayHedge indexes are recalculated and updated as soon as the monthly returns for the underlying funds are recorded. Only funds that provide BarclayHedge with net returns are included in the index calculation. The number of funds that are currently included in the calculations for the most recent months can be found at www.barlcayhedge.com. Please note that the calculation for the number of funds is time-stamped and that the number of funds will continue to increase until all funds categorized within the sector have reported monthly returns. The Credit Suisse Leveraged Loan Index represents tradable, senior-secured, US-dollar-denominated, noninvestment-grade loans. The HFN Fixed Income Arbitrage Index includes funds that attempt to exploit pricing inefficiencies between credit sensitive instruments which may include government or corporate debt, structured securities and their related derivatives.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and consider the investment objectives, risks, charges and expenses.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2014 Invesco Ltd. All rights reserved.