Both our operating and investment experience cause us to conclude that “turnarounds” seldom turn, and that the same energies and talent are much better employed in a good business purchased at a fair price than in a poor business purchased at a bargain price.

- Warren Buffett, Berkshire Hathaway Annual Report 1979

Like all good students, we try to learn from the experience of experts, and amongst value investors there is no more esteemed expert than Warren Buffett. We have followed Buffett closely, sending dozens of employees to Berkshire Hathaway annual meetings and scouring past letters to shareholders in search of value investing knowledge. Thus, we pay heed when Buffett warns that the temptation to predict a “turnaround” is often misguided. However, when interpreting historical information, such as the quote that starts this paper, it is important to focus on the overarching message and not let the specific words obscure the lesson. In the current investment environment, dominated by twenty-four hour financial news and an obsessive focus on the short-term, the phrase “turnaround” has come to be used casually as a description for any company that isn’t reporting record earnings. We believe the more important distinction is between a good business – defined by prospects for growth over the long-term, above average returns on capital, and an attractive industry structure – and a poor business. A good business does eventually turn; it recovers from mismanagement, short-term fluctuations in the business cycle, and competitive challenges.

Over the past year, we have been building our ownership stake in insurance broker Willis Group Holdings PLC (WSH), which according to numerous financial commentators is a “turnaround” with significant “execution risk” associated with its long-term operational improvement initiative. Indeed, the very phrase “operational improvement initiative” seems to self-identify Willis as a company in need of fixing, and a string of quarterly earnings shortfalls versus consensus expectations has encouraged more bearish analysts. We have a different perspective, however, believing that Willis is not a turnaround but rather a firm that is achieving a measure of success in an attractive industry and one that has the opportunity to dramatically improve its shareholder returns through actions largely under its own control.

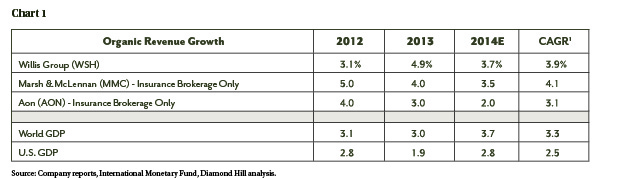

By any reasonable definition (i.e., not focused on one quarter or one year of results), Willis is not a poor business. In fact, it is a very good business. Over the past three years, Willis has posted organic growth in excess of World GDP, and we expect this pattern to continue as insurance penetration increases in developing economies and the large insurance brokers maintain market share in developed markets. (See Chart 1 below.)

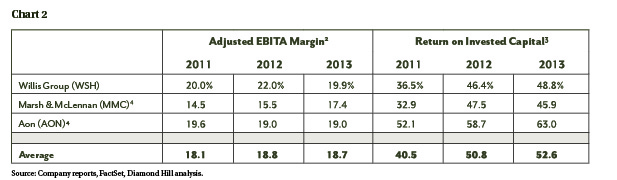

Importantly, Willis achieved above GDP organic revenue growth while still producing attractive operating margins and returns on capital. Over the past three years, Willis’ return on invested capital averaged nearly 45%, in-line with its large competitors. Critics will point out that through the first three quarters of 2014, Willis reported modest margin compression, as investments in personnel during 2013 led to expense growth in excess of revenues. However, expenses have stabilized in recent quarters, and we expect the operating margin to expand significantly as investments made in 2013 are lapped and the impact of the company’s “operational improvement initiative” is realized. This cost savings plan aims to reduce expenses by $300 million, or approximately 10% of the 2014 operating expense base, by 2018. The expense savings will come from two primary areas: 1) relocation of support functions to low cost locations and 2) reduction in real estate footprint. While some skepticism about the company’s ability to realize these savings is warranted, given prior management’s inability to yield sustainable gains from smaller cost saving initiatives, we believe the changes contemplated under the current program are more structural in nature and have successful precedents at both Marsh & McLennan Cos., Inc. (MMC) and Aon PLC (AON). Both Marsh & McLennan and Aon have made structural changes to their cost bases over the past ten years, increasingly employing outsourcing for support functions and reducing fixed costs such as real estate. The changes at Marsh & McLennan and Aon have been successful by any measure, leading to more predictable expense growth and consistent operating margin expansion. We see no reason that such changes will not be successful at Willis as well. (See Chart 2 below.)

1 Compound Annual Growth Rate

2 (EBITA + restructuring costs + non-servicing component of pension costs) / revenue

3 NOPAT / beginning of period total assets - cash - pension assets - intangibles - accounts payable - other current liabilities

4 MMC and AON results include both Insurance Brokerage and Consulting segments. Brokerage is higher margin.

The large insurance brokers’ track record of stable organic growth and superior returns on capital suggests they have historically possessed competitive advantages that provided buffers against competition. While this historical evidence supports our contention that Willis is a very good business, our returns will reflect what happens in the future not the past. We believe high switching costs combined with significant investments in intellectual capital will prevent competitors from eroding Willis’ high returns in the future.

For corporations, their insurance broker provides the most tangible benefit derived from their insurance expenditure, with the broker delivering analysis of the company’s risk exposures and providing options for addressing those exposures that are not easily accessed by the company on its own. However, the broker’s cost is largely invisible to the client and represents a small fraction of the ultimate premium paid. For complex organizations with large amounts of data to be analyzed, the risk of switching insurance brokers is far higher than the risk of switching carriers. Moreover, there are only three firms in the brokerage industry – Marsh & McLennan, Aon, and Willis – that have invested heavily in the analytical skills and breadth of market access required to service the largest corporations, and competition between them has been rational. As a result of these factors, the large insurance brokers do not compete on price, have client retention rates above 90%, and face minimal threats from new entrants, who would have to invest heavily to offer the levels of service required and would have limited means of acquiring business.

In our view, Willis is a very good company, one that can weather the short-term headwinds it faces and significantly improve its results over the next few years. Solid organic growth and superior returns on capital are already characteristic of a very good company, and we believe the success of Willis’ operational improvement initiative will lead to more sustainable earnings growth and confirm those other indicators. Finally, we believe an attractive industry structure, with competitive advantages for incumbents, supports our view that Willis will continue to be a very good company for many years into the future. Willis’ current valuation reflects little of the positive change that we expect over the next several years, providing an attractive expected return for long-term investors.

The views expressed are those of the research analyst as of December 2014, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2014 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management