Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

The day after Thanksgiving we noted that Global Carry has gone parabolic and needs to be watched carefully. It has been mildly correcting since and we encourage investors to stay cautious. We also review where we stand in terms of Risk On/Risk Off factor.

As we have recently explained elsewhere[1] Global Carry is of paramount importance in current financial marketplace of zero or near zero interest rate policies.

Since the Taper Tantrum the Global Carry factor has performed as follows

You can see that the recent move was somewhat parabolic[2] and we hit top on the day after Thanksgiving which was subsequently followed by disturbing ongoing correction.

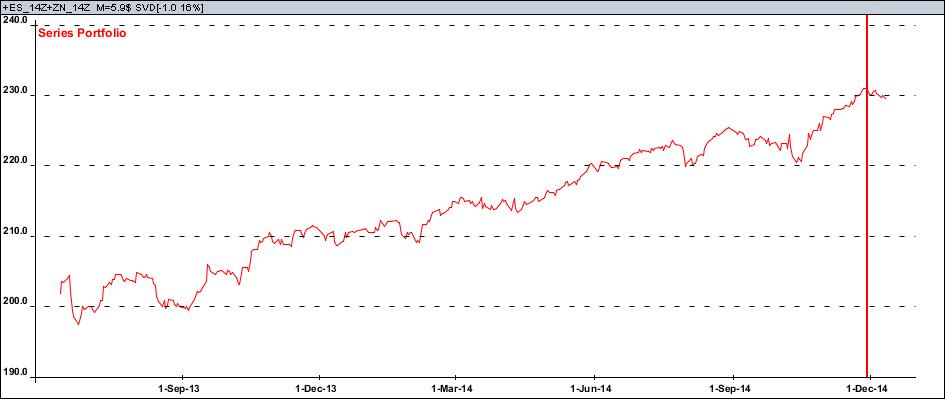

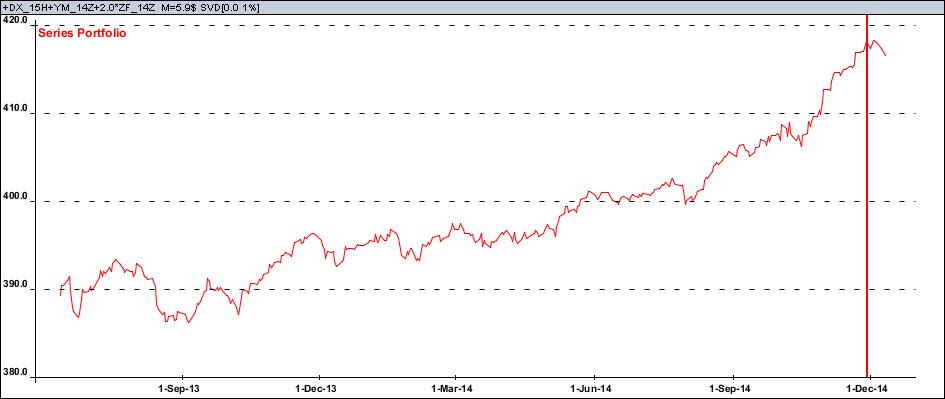

Below we refresh our Global Carry proxy portfolios

- SPX E-mini future plus 10y note future:

- US dollar index (“cleanest dirty sheet”) plus DJ index future plus two (shorter duration) 5y note futures:

It is worth to be very careful with the Global Carry at the moment.

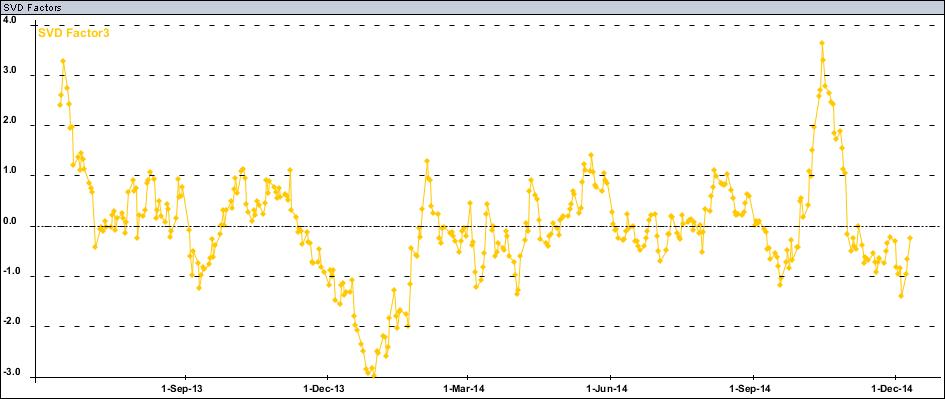

Another source of ongoing concern is the Risk On/Risk Off factor which it seems might be intended to come back off the recent Risk Off lows where it stayed for a while after its 15th of October peak:

While nothing dramatic here yet and holiday season is supposed to be Risk Off environment it is worth to be watched carefully too (it can be easily traced in equities, especially Nikkei, and Japanese yen).

[1] “Global Carry a.k.a. Risk Parity”, Dynamika Commentary, 16-Oct-2014

[2] “Global Carry gone parabolic?”, Dynamika Commentary, 29-Nov-2014