A part of our continuing “What’s that got to do with investing?” series

When I was a kid there were just four year-end college football bowl games. Today there are 39. Perhaps the title of this piece should be “Do we need holiday football bowls at all?” But I guess they wouldn’t produce them unless there was a demand for them – from the cities, hoping to get some travelers, to the sponsors, hoping to get some attention, to the teams, seeking to cap a successful season, and to the fans, who are just looking to have some fun and experience a last hurrah for this year’s heroes.

Despite the fact that the number of bowls has increased by almost eight-fold, the problems that plagued the original four persist. Who should go to the Bowls? Considering that most conference teams go with just a 7-5 record and there are over 75 teams playing in a bowl (there are only 128 Division I football teams in the nation), you would think that the selection would be cut and dry with no room for arguments. Au contraire!

This is the first year of the College Football Playoff Committee (CFPC) selection process, put in place to finally, unequivocally, deliver a national college football champion. From 1998 until now we fans have lived under the rule of the Bowl Championship Series (BCS) process. Based on the various college football polls of experts and computer rankings, the BCS was forever being criticized for both their lack of a true national championship playoff process and its actual selection of the teams to participate in the various bowls.

That criticism led to a four-team playoff (instead of a two-team championship game). Selection by the new CFPC threw out the polls and the rankings and has gone to the NCAA Basketball playoff system where a committee makes the qualifying team decisions. The Committee said that it would rank the teams on strength of schedule, head-to-head and total win/loss records, as well as other stats supplied by ESPN. The rankings appeared weekly this year in the lead up to the final bowl selection Sunday.

Going into this weekend the top four teams in the CFPC’s rankings were Alabama, Oregon, Florida State, and Texas Christian University (TCU). The teams selected Sunday were Alabama, Oregon, Florida State, and … Ohio State!

Immediately there were howls of pain and disbelief from football fans. Today’s headline in the paper is “Big 12 feels cheated by the committee – Co-champs Baylor and TCU left out of four-team playoff.” Each of these teams had but one loss, like all the play-off bound teams save undefeated Florida State, and TCU had been ranked in the top four going into the weekend rankings (although that too was questionable since Baylor had beat TCU in a head-to-head match-up earlier in the season).

There are five major conferences in college football. Incredibly, the rankings and the four-team limit to the playoff seem to take no notice of this. In fact, the rules allow more than one team to represent a conference, despite the fact that four of the five football conferences have a championship playoff. This almost guarantees a dispute.

It has not gone unnoticed that the one conference left out this year was the only one without a league playoff. This has led many to speculate that that was the deciding factor, as those playoffs immediately preceded the final Committee rankings. Perversely, it is also college rules that preclude the Big 12 from having a playoff because they only have 10 teams presently! They are doubly cursed.

The failure of the Committee system to satisfy both football analysts and fans alike actually seems rationale to me. With apologies to Abraham Lincoln – I think the history of human behavior clearly demonstrates that “You can’t satisfy all of the people any of the time.” Someone will be upset no matter what you do.

Of course, this same logic was utilized to justify the sixteen years of BCS disputes, so there must be more. I think the “more” is that a system without objective, quantifiable criteria is doomed to failure.

When I began creating stock market trading systems in the sixties, I was motivated by the fact that everyone had an opinion on the stock market and how to trade it, but few could back that up with any science. Had the applicable past statistics been collected? Had they been quantifiably analyzed for statistical significance? Were they reproducible by others? Back then the answer to all of these questions was “no.”

If one asked these questions of the present CFPC ranking system, the answer would be the same. “No,” one must answer, because the rankings are the result of a committee of “experts.”

I’ve railed about the success record of experts for years. Most major studies show that experts are wrong more times than they are right. Each expert has their own guiding principles, each focuses on their own important statistics. Each is subject to all the behavioral biases that make it difficult for humans to make decisions in complex, emotional contexts.

One solution to the downside to this behavior that has proven to be successful is to quantify the selection criteria and then stick with it in the decision making. While you can always criticize whether you have all of the criteria right and included, you can be sure that you can reproduce the results over a history to verify its “fit” and determine whether the results have statistical significance. You can’t do this with the committee approach, be it an investment committee or the CFPC.

This is precisely the approach we take when developing new stock market strategies. We reduce the strategy to its quantifiable inputs, outline the rules governing the interaction of the inputs, and then apply the rules to past inputs to see whether the rule set generates results that are statistically significant (significantly better than random results).

Unfortunately, this is still not the norm on Wall Street. But they do employ clever marketing to obscure reality. For example, I saw an ad the other day touting that the mutual fund company had X number of strategies (one for each of their mutual funds, coincidentally) all under one roof.

There is no doubt that this ad was an attempt to overcome the increasing popularity of alternative strategies or smart beta products. Unspoken was the fact that the next stop for each of the X number of these funds’ strategy results was the funds’ Investment Committee. There, like at the CFPC, the committee wrestles with the decision of what findings to follow and what actions to actually take.

This is where behavioral bias takes over and the process fails. In a truly quantified decision process, there is no committee decision making. The numbers speak for themselves. And action automatically follows the quantifiably derived results. Human bias and emotion are removed from the process in the interest of better long-term investment results.

The CFPC should take a page from quantified investing. At least the fans, the schools, and the teams would know in advance what was being considered and what weight was being put on it. They might complain about the inputs and their weightings, but not that they were blindsided by the results.

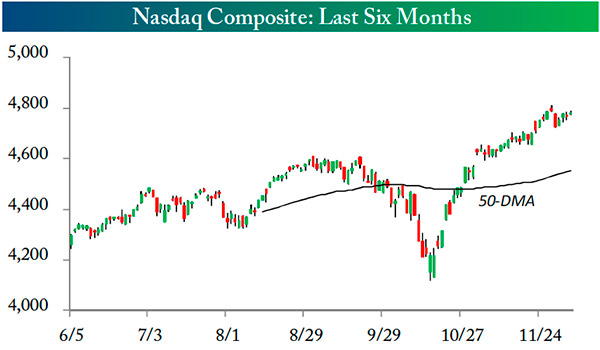

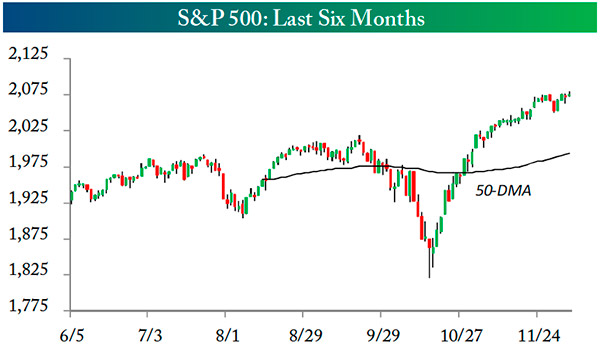

Many do continue to be blindsided by the results on Wall Street. Stock markets in this country continued to rack up gains last week. We have been in one heck of a rally since the market bottomed on October 15, as the charts of the S&P 500 and NASDAQ show.

Source: Bespoke Investment Group

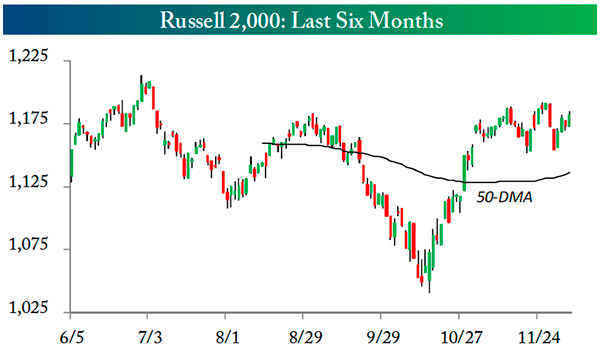

Yet it has been a strange rally. A majority of stocks are down more than 10% since they registered new highs earlier this year. In addition, the broader-based Russell 2000 small-cap index has failed to move higher for most of the year. Note how flat the price trend has been in the accompanying chart.

Source: Bespoke Investment Group

Another indicator of the hidden personality lying behind the large-cap market indexes often cited by the media is the large number of investor favorites that have been languishing this year. Take a look at the list provided.

Source: Bespoke Investment Group

While the S&P 500 is up over 12% this year, many actively traded, widely known stocks are actually down for the year. As the Bespoke Investment Group reported:

“Names like Amazon.com (AMZN), First Solar (FSLR), Google (GOOGL), IBM, Netflix (NFLX), Priceline (PCLN), Qualcomm (QCOM), TripAdvisor (TRIP), Whole Foods (WFM) and Wynn Resorts (WYNN) are all a who’s who of the stocks that individual investors like to invest in, and none have delivered any gains this year.”

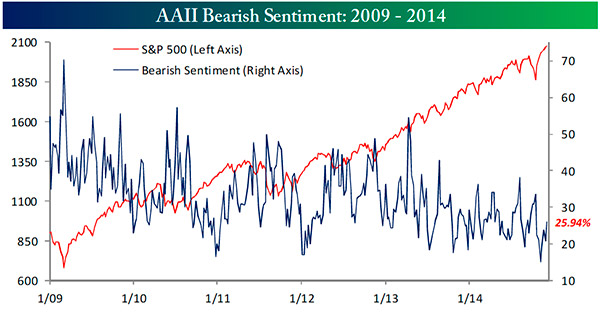

Furthermore, investors continue to scorn stocks in general. Despite new highs on the major indexes, most investors (as measured by the AAII Investment Sentiment survey) are actually becoming more bearish. Anecdotally we hear that many of these investors have not been in stocks for the entire rally that started in March of 2009!

Source: Bespoke Investment Group

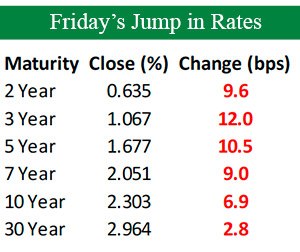

There are reasons for some caution at the present time. We seem to be in an equilibrium period where positive economic surprises are balancing out against negative ones. As the table shows, interest rates have been rising. Friday’s positive jobs report was finally recognized as “good” news, but the positivity was restricted to stocks. Since interest rates rose substantially, bonds (where many investors fled) tumbled in price. Earnings are at high levels, but so are price/earnings ratios, frightening many of the more fundamentally-oriented investors.

While we are in the seasonal period where we normally have a pause in the Santa Claus rally that typically ends each year, the continuing overriding fact is that we remain in rally mode.

The trend is up. Until the major trend breaks, stocks continue to be the place to be.

The CFFP based its new “bracket selection” system on the popular March Madness, NCAA Men’s College Basketball Championship. Back in 1939, the championship started with eight teams being invited. For eleven years the NCAA heard the criticism, as worthy contenders were omitted. In 1950, they responded to the griping and expanded the tournament to 16 teams. Still the harping continued, and in the intervening 60 years the NCAA expanded the number of teams nine more times!

Today, 68 teams are invited to the National Championship tournament, with the last change coming in 2011 when four teams were added through new “play-in games.” Immediately after last year’s selections were announced…

As I said, “You can’t satisfy all of the people any of the time.”

All the best,

Jerry

P.S. I’ve written about the famous Marshmallow Experiment in the past. Now with a recent follow up study, it has become even more relevant. This story takes a slightly different take on the results as they relate to investing. Enjoy.

http://cms/market-hotline/disclosures