Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

Global Carry has gone parabolic. Last such move precipitated the Taper Tantrum, only this time the parabolic move is exaggerated by US dollar appreciation.

As we have recently explained elsewhere[1], it is customary to think of “Risk Parity Asset Allocation” and “Carry Trading Strategy” as the two different things. But the Risk Parity after the Global Financial Crisis is nothing else but a hugely successful Global Carry Trade funded in Japanese Yen, Dollar and Euro. The performance of this trade is fantastic, the allocation is huge (100s of blns of $) and the risk of crash that will precipitate the next financial crisis is growing day by day.

Below we review briefly where we stand.

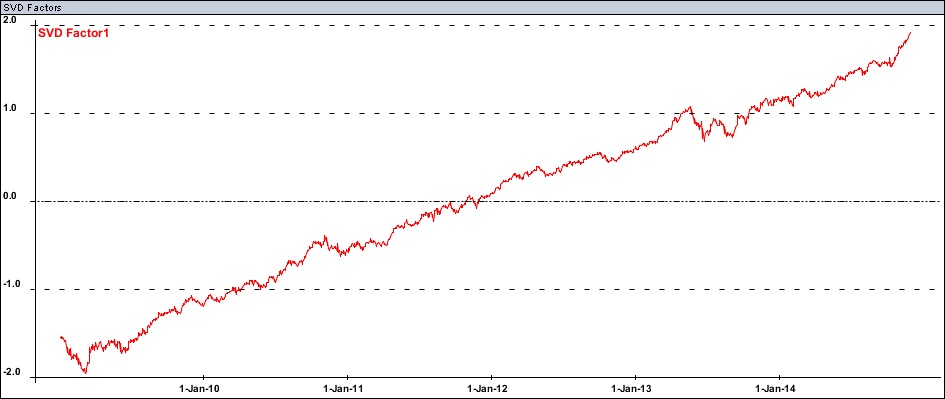

Since 2009 the Global Carry factor performed as follows

You can see that the recent move is somewhat parabolic and we hit top of the range which last time was followed by the Taper Tantrum (it is also true that top of the range was hit in November 2010 with little consequences).

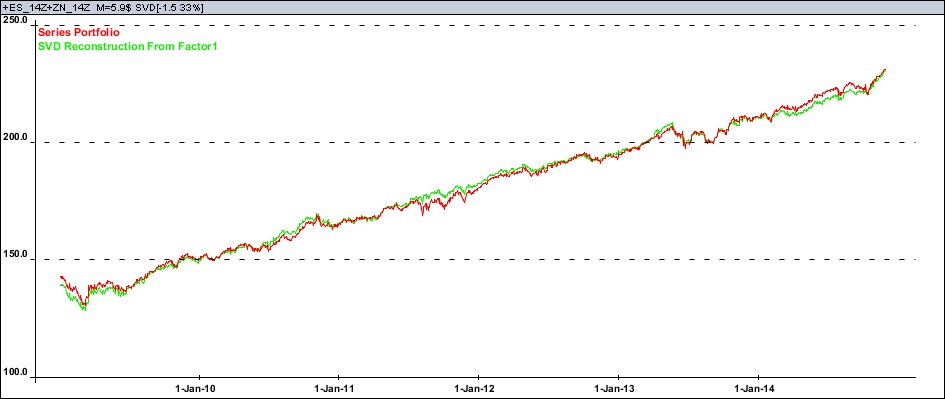

Good proxy for this performance is a simple equal risk (hence Risk Parity) portfolio allocation to US 10y treasuries and SPX index easily replicated by two futures positions - SPX E-mini future plus 10y note future:

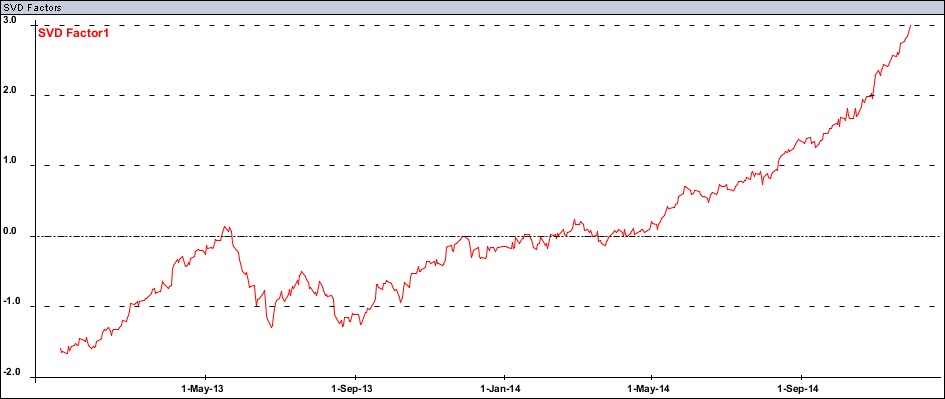

Even more disturbing is the recent incarnation of the Global Carry which includes US dollar appreciation at its core. After the Taper Tantrum related sell-offs of last year it is gone awry with the recent US dollar appreciation:

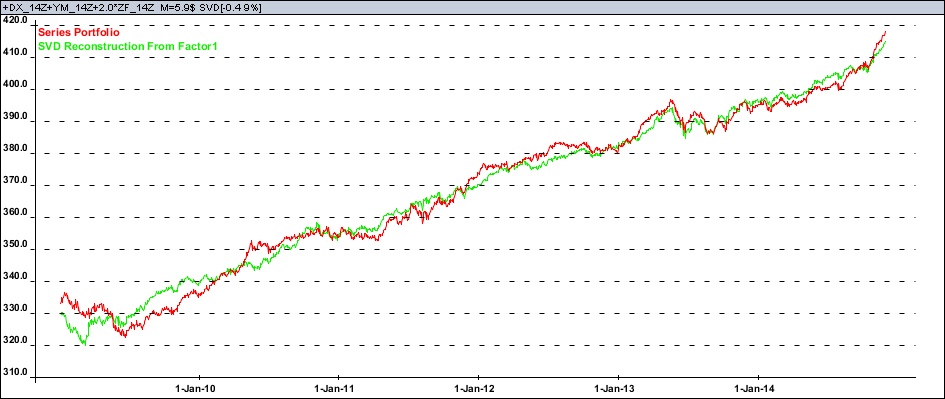

It too can be proxied by a simple futures portfolio of US dollar index (“cleanest dirty sheet”), DJ index future and two shorter duration (Hello again Bill!) 5y note futures:

It appears one should be extremely cautions with this trade at the moment: its recent sweetness is only compared to its ubiquity.

[1] “Global Carry a.k.a. Risk Parity”, Dynamika Commentary, 16-Oct-2014, www.dynamikacapital.com/subscribe